Pier 1 Imports (NYSE: PIR) is a retailer of home furnishings. It’s a stock I check up on once in awhile but never considered buying it.

In a classic case of “do not confuse consumer markets preferences with your own”, almost every time I walk into the place (which is usually once a year to see what sort of junk I do not want in my living room) I walk out thinking to myself how this place exists as an entity. This thought of mine has been for nearly a decade. The company has defied my expectations for quite a long time.

From the 10-K: “During fiscal 2019, the Company sold merchandise imported from many different countries, with approximately 60% of its sales derived from merchandise produced in China, 16% in India and 17% collectively in Vietnam, the United States and Indonesia.”

60% of its sales derived from China? Uh-oh, watch out for those cost of goods sold rising!

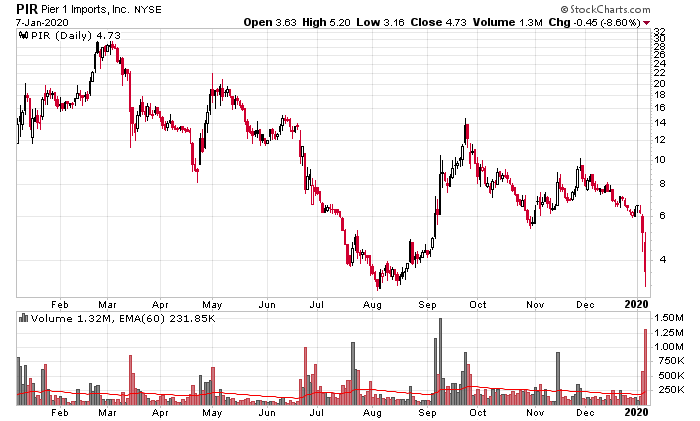

It looks like it finally might be happening – their last quarterly result for the November 30, 2019 quarter was very lacklustre. Gross profits were 31% of revenues, but SG&A expenses were 42%, which translated into a $59 million dollar hole for the quarter when factoring in depreciation and interest expenses.

They then came to the realization they need to close down half their stores to cut costs.

On November 4, they also appointed their CFO to replace the old interim CEO. I’m sure the executive suite is having a lot of fun right now.

A year ago, PIR had just over $600 million in the “retained earnings” line item on their balance sheet. That is down to $295 million. Current assets are less than current liabilities, and the company is drawing down its revolving line of credit – currently $96 million is borrowed, and they can take out another $158 million – until April 30, 2021 when a separate term debt facility matures.

So this is clearly a race against time – about 15 months – they need to shut down unprofitable stores, and get to the point where they can start building credit again to extend their credit facilities.

In terms of raw valuation, PIR only has 4.1 million shares outstanding, so when doing the math on their $5 stock price, you’re betting on them simply not Chapter 11-ing themselves out of their situation, which is a very high probability outcome at their current trajectory. Leases and debt commitments have to be honoured, and Chapter 11 must look awfully alluring for management.

Back in the glory days, the year ended February 2016, they generated over a hundred million in free cash flow. In February 2017, it was $72 million. In February 2018 that went down to $13 million. When fashion goes against you, watch out!

I would then make a contrast with the company that used to be known as Restoration Hardware (NYSE: RH) that somehow managed to become a $200 stock because they successfully realized that retail is either about the upper-upper end (just click on their “RH New York” video and contrast with PIR), or the lower end (think Dollarama and Walmart!) and anybody inbetween will get killed, like Pier 1.

Or, you might get lucky with Pier 1 just because the valuation is so cheap at present – sort of like a Francesca’s (Nasdaq: FRAN) when the stock quadrupled after an unexpectedly profitable quarterly report.