I’ve been following the PG&E (NYSE: PCG) story rather closely.

I don’t know anybody that would actually want to operate a utility in California with the state’s liability regime (you are completely liable for damages as a result of wildfires) and this is a pretty clear example of avoiding an investment that will have a good blow-up disaster potential.

Most publicly traded utility companies trade as if they are stable and boring, but in reality, there are quite a few that have embedded hidden risks – beyond their insurance regimes.

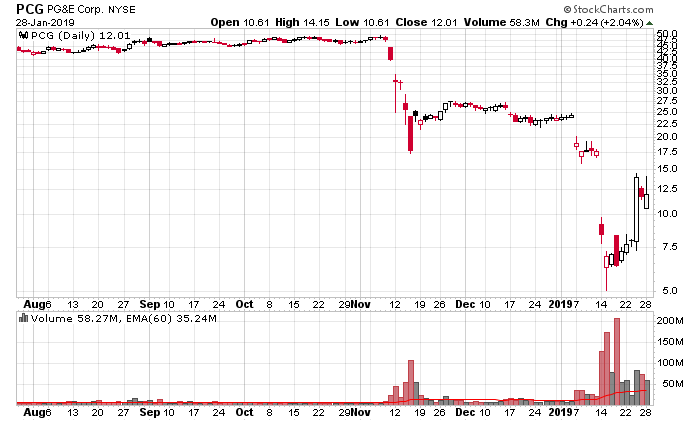

The more interesting part of this story is that even after the initial wildfires to cause the slide in the stock, an investor still had plenty of time to bail out before PCG was finished.

But now they’re into Chapter 11, primarily to shed liabilities associated with the California wildfires.

Financially, PCG has US$20 billion in equity on the balance sheet, which works out to about $38/share. They accrued $2.8 billion in wildfire-related claims in liabilities, but estimates are that there will be about $22 billion coming in, which would nearly wipe out the equity in the company.

The unsecured debt is trading at around 80 cents on the dollar presently, but one could make quite a bit of money on the equity if your loss projections on claims were less than what the market is projecting at the moment.

I’m not the type of person to be playing such types of financial games as there are typically far more smarter people than I am (to determine the residual value of PG&E after claims), but I still find it interesting to see how it will resolve nonetheless.

One thing is for certain – people still need to be supplied electricity, and electricity is a very inelastic commodity. When you have so much state regulation in place, especially when hearing about multi-billion dollar capital and maintenance expenditure proposals to prevent future wildfires across huge amounts of power lines, it all serves to have one effect – raising the cost of electricity for captive customers. California residents (e.g. Los Angeles) already pay very high rates for power – and after this debacle on PG&E, they’ll be paying more after these claims are settled. The money has to come from somewhere.

Think a moment about your investments in well-known utility companies such as Emera (TSX: EMA) or Fortis (TSX: FTS) or Hydro One (TSX: H) for a moment. Is there more risk than you originally anticipated?