On paper, the valuations of various international oil/gas producers look quite cheap.

One example is the state-owned enterprise of Petrobas (NYSE: PBR).

For the past 12 months, they generated about USD$37 billion in cash. Their current market cap is about USD$69 billion, and net debt is US$48 billion (total EV US$117 billion), so an EV/FCF of about 3.2x. Really cheap-looking!

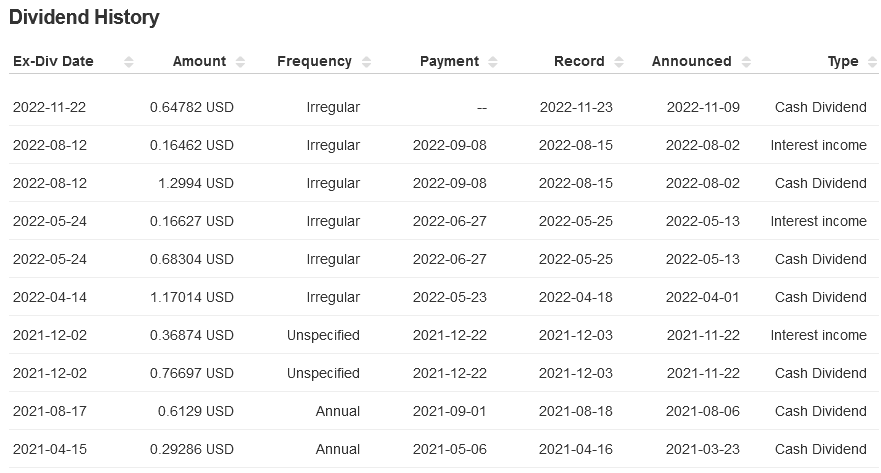

Also, there is no denying that shareholders have received some capital back in the form of dividends:

For 2022 alone, this has totaled USD$4.13/share in dividends.

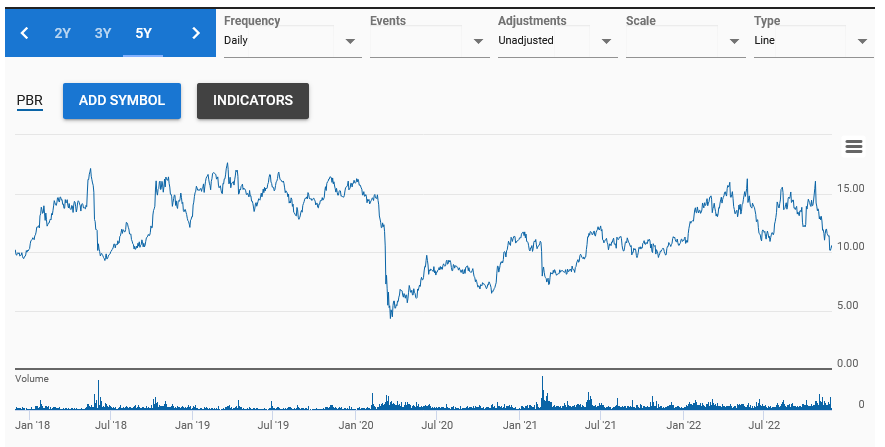

When dividends are this high in relation to the existing share price (US$10.54/share), it is instructive to look at the stock price unadjusted for dividends:

So let’s say you lucked out during the Covid low (March 2020) and bought your shares of PBR at US$5/share.

Today you would be sitting on a cumulative dividend of US$6.27/share.

Needless to say, this is a very healthy cash return on investment.

The question is – is this cash stream going to continue in the future?

Political considerations would have one believe otherwise. Jurisdictions all over the world, ranging from the United Kingdom, the EU, Colombia and the alike have either implemented or are calling for “windfall profit taxes” to be levied on hydrocarbon companies.

The history of Brazil and Petrobras I will not explore in this post, but needless to say, it is quite the story about how very profitable state-owned resource enterprises are, not shockingly, not optimized for shareholder returns.

The history of Mexico and Pemex is another one.

Venezuela and PDVSA.

Saudi Arabia and Aramco.

I can go on and on.

Finance and politics go hand in hand. When dealing with politically sensitive sectors such as hydrocarbons, political considerations must be in the investing toolbox.

In the case of Petrobras, “too difficult” is all I can come up with. I have no idea about the legislative framework and the relationships between the government and its state-owned agencies, nor do I have a way of assessing whether the new presidency will be able to substantively enact hostile actions to minority (let alone foreign) shareholders. In general, not even knowing the language of the land is enough of a disadvantage, let alone all of these other prevailing considerations.

Just like when investing in a company with a controlling stake, you always have to have a precise assumption of the intentions of the controlling stakeholder before diving in.

We fast forward to Parex Resources (TSX: PXT), which, just like Petrobras, on paper looks extremely cheap.

Its market cap is US$1.5 billion, and it has net cash of US$350 million, leaving it with an EV of about US$1.17 billion.

It generated free cash flow of US$275 million for the first 3 quarters of this year. Annualized, that is about US$370 million (not an appropriate extrapolation since Brent is down in Q4 from Q1-Q3 but we are doing a paper napkin valuation).

That is an EV/FCF ratio of about 3.2x. Just like Petrobras.

Looks cheap on paper, but going forward things are going to get much more expensive for the company. Colombia’s newly elected president has successfully put forward and passed a piece of legislation that is financially punitive. In addition to the general corporate tax rate increasing, there will be a 15% surcharge levied if Brent is above a certain threshold, and also royalties on oil and gas are no longer tax deductible.

This will do wonders for capital investment, let alone talks about banning further drilling.

Also not helping is the domestic situation allowing for blockades and the like against existing producing facilities (run this through Google Translator).

Parex will likely be best valued as a run-off facility. The question becomes whether it is worth it for them to propose a significant amount of capital expenditures to keep their facilities pumping at current levels or not, even if this can be achieved in a regulatory environment that makes Justin Trudeau look like oil and gas’ best friend.

I don’t know.

Parex has traditionally given a huge amount of shareholder returns via the share buyback route – they have maxed out their 10% NCIB in the past few years. Their new NCIB will renew around Christmas time, and that will likely give a bid to their stock. Trading-wise you might even be able to skim 10-20% riding the NCIB capital infusion. However, just because you take out 10% of your float every year for a few years doesn’t mean that your stock price will respond if your home government is taxing the majority of your future profits away. As most people know, when the government enacts a tax, it is a very rare day when they will take back the tax. Inevitably there will be a day where the commodity price environment reverses and we will never see a reverse “windfall recovery grant” given to such companies.

So despite it looking incredibly cheap on paper, I’m staying away. We’ve seen many cases in the past where the golden goose gets strangled. This might be the case and hence why these companies trade at 3.2x EV/FCF ratios.