I recently took a position on warrants that trade on Mirion Technologies (NYSE: MIR, warrants trading as MIR.WS). My average entry was under a dollar per warrant.

Nuclear Insurance

There are a small number of companies out there that specifically deal with the nuclear industry and even less that are pure plays. You can invest in generalized engineering companies like Fluor (NYSE: FLR) or GE (NYSE: GE), but they have a lot of non-nuclear operations which dilutes the sector interest to an insignificant level. You can also invest in power generation (e.g. Tokyo Electric, 9501.JP), but power itself is a commodity and you are investing in commodity-like characteristics. Likewise the same can be said for Uranium producers like Cameco (TSX: CCO). There are a handful of firms that can be considered pure plays.

One of the historical pure plays in this sector was a radiation detection company called Landauer (formerly NYSE: LDR), but in 2017 they were taken off the public market via acquisition by Fortive (NYSE: FTV), a very large diversified instrumentation company. Another one that I have written about in the past is BWX Technologies (NYSE: BWXT), which its primary moneymaker is producing nuclear reactors for US Navy vessels, but for various reasons I divested myself of this investment earlier this year.

Mirion is a pure play. It is an aggregation of various products relating to radiation biophysics, including medical imaging and also industrial imaging and the like as it relates to the radiological side of things.

I want to clarify the term nuclear insurance. It is specifically looking for a company that will rise in price dramatically whenever there are threats of nuclear catastrophes, likely due to geopolitical concerns or improper operations of nuclear reactors. To be clear, this is assuming that financial markets will still be functional after such an event – if this is of the scale where you have thousands of nukes thrown across the planet, there will be bigger problems to deal with!

The general theme of this trade is thinking of the biological analogy of what happened with Alpha Pro Tech (TSX: APT), a personal protective equipment manufacturer, during the onset of Covid-19:

This company rose by a factor of about 10x from early January to March 2020 when things got really hot and heavy. I would suspect in a nuclear scenario, Mirion would exhibit a similar price curve and hence the ‘insurance’ as probably every other component in the stock market would evaporate at about the same speed as something at ground zero.

Mirion, the company

This trade would be so much more attractive had the corporate entity had better characteristics, but sadly it does not.

Mirion can be described as a broken SPAC offering, going public in October of 2021. The predecessor name was “GS ACQUISITION HOLDINGS CORP II” and merged into what is Mirion today. It was the typical arrangement, going ‘public’ at $10/share with some warrants. Any investors in the SPAC post-closing (who are these people??) have lost money. As of April 2022, about 40% of the company economically is owned by Goldman Sachs entities. 20% are owned by two other hedge funds. The long-time founder and CEO owns about 2% of the stock. The Goldman entities are actively divesting stock – indeed, the principal officers have a listed occupation as “Goldman Sachs” which is amusing in itself. I’m sure the follow question gets asked at cocktail parties: “What do you do for work?” Answer: “Oh, I’m a Goldman Sachs”.

The corporation has a dual class structure, but the second class of stock does not convey any disproportionate privileges.

I’ve discussed above what the company actually does, and it is not a fly-by-night operation. They have about 2,600 employees, and 75 US patents (which you can search for and contain headlines that are in the relevant domain area).

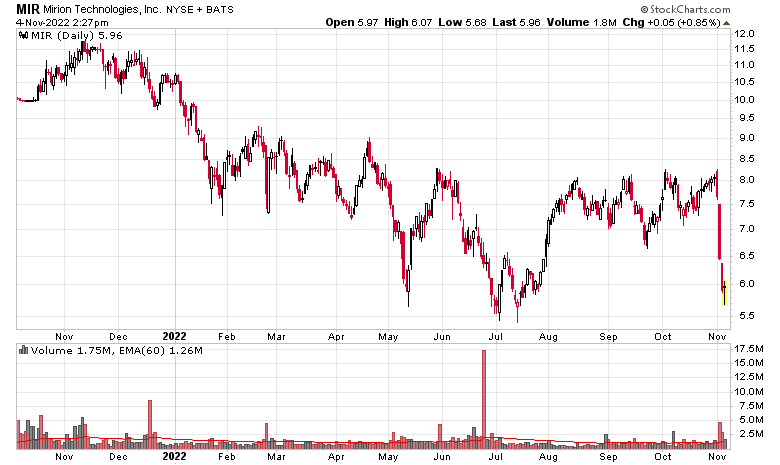

The big problem is financial. The company has a balance sheet issue, and even worse, they don’t make that much money. Note the market cap of the company at a $6 stock price is about $1.25 billion. They got rightfully slammed after their third quarter report. It was awful.

Looking at their Q3-2022 report, the balance sheet has $58 million in cash and $808 million in debt. The only silver lining on the balance sheet is that the debt is in the form of a floating rate (LIBOR plus 275bps) secured loan that does not mature until October 2028, which is a huge time runway for them to figure things out.

The bad news is that the company is cash flow negative. Management talks about positive “adjusted EBITDA” this and that, but in reality, they are bleeding cash. They need to raise their prices and get their cost structure in line, especially now that LIBOR is rising like a piece of Styrofoam rising from the middle of the ocean.

I will spare the quantitative analysis other than to say that while the TTM price-to-sales is very roughly 2x (with companies such as TDY or FTV at 5x and 4x, respectively), the cash generation situation is just awful. This is not an attractive company using trailing financial metrics.

That said, it is in an industry which is relatively inelastic in terms of consumption preferences – companies that need the product are not going to suddenly defer their purchases. As a result, a general economic recession is not as likely to affect Mirion as it would for some other industrial suppliers.

The warrants

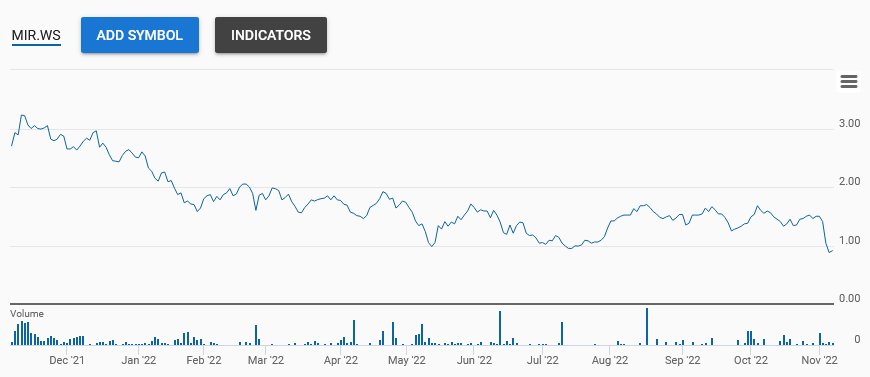

The warrants have a headline expiration date of October 20, 2026 and a strike price of $11.50. This is about 4 years to expiry. They are trading around 95 cents at the moment. I will humble-brag that my last purchased tranche to finish my trade was at 80 cents.

It might appear to be a bad deal considering the common stock is trading at half the price of the warrant strike price.

However, when it comes to warrants, they are not always traded like standardized options.

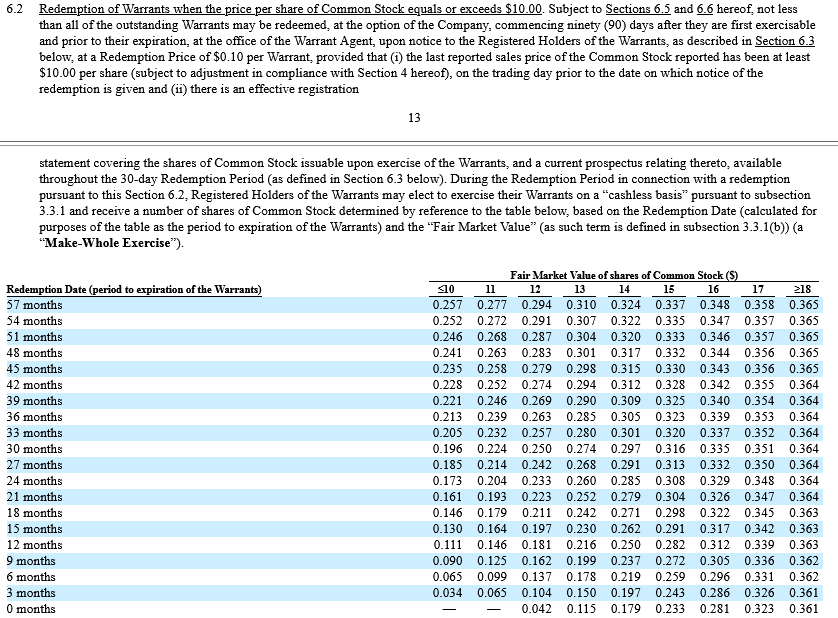

When reading the fine print of the Mirion Warrants, the most relevant non-standard clause governs the option of the company to exercise the warrants if the common stock trades above US$18/share, which will enable the holder to receive 0.361 shares of MIR at a 10 cent exercise price at expiration:

Mirion also has the right to exercise the warrants above US$10/share and the holders have a month to decide if they want the number of shares in the table or whether to take the warrants the ‘conventional’ way. I do not know any scenario where Mirion would want to force the conversion of warrants, but perhaps one of my readers can enlighten me.

Back to nuclear insurance

If there is a relevant nuclear event, I would anticipate the warrants would appreciate significantly beyond their current trading price. As there is time value remaining on these financial products, I would suspect in the worst case scenario in a couple years that I would be able to get out for moderate losses. Again, this is insurance more than anything else. And heaven forbid, if the company gets its cash flow situation in line and actually starts to learn to how to make profits, the stock will appreciate on its own.

This is a small position, I do not intend to make it larger, and the chance of making a loss is relatively high. I share this research for you.