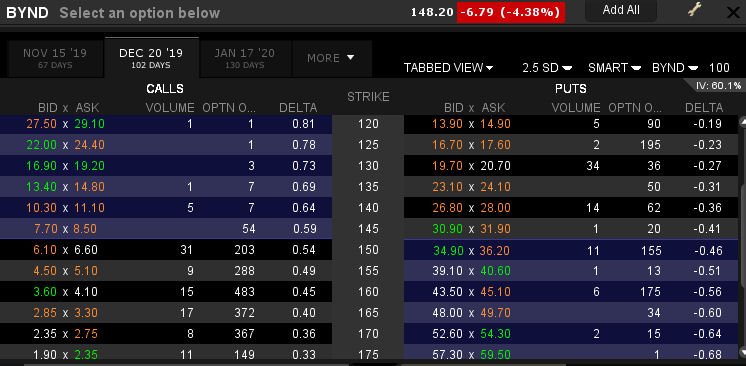

I just take a look at this chart from Beyond Meat (Nasdaq: BYND):

What is the first thing I think of when I see this chart?

“Follow-on offering”. BYND did their IPO in early May, and insiders are restricted from selling shares (not distributed during the IPO) for 180 days, but the company can raise capital in the meantime! I would not be shocked at all to see them raise another $750 million or so this month.

They haven’t even filed Form 10-Q yet, but when skimming their Q1 earnings press release, net revenues of $40 million for the quarter, and management estimates $210 million for the year. They raised a net of $252 million on their IPO (which was in early May, at a price of $25/share).

Needless to say, the $10 billion market capitalization is frothy. Investors in this stock better heed the following entry in the prospectus (I’ve highlighted the relevant section below, with a link for those so interested):

We may not be able to protect our proprietary technology adequately, which may impact our commercial success.

Our commercial success depends in part on our ability to protect our intellectual property and proprietary technologies. We rely on a combination of patent protection, where appropriate and available, copyrights, trade secrets and trademarks laws, as well as confidentiality and other contractual restrictions to protect our proprietary technology. However, these legal means afford only limited protection and may not adequately protect our proprietary technology or permit us to gain or keep any competitive advantage. As of March 30, 2019, we had one issued U.S. patent and 21 pending patent applications, including eight in the United States and 13 international patent applications.

We cannot offer any assurances about which, if any, patents will issue from these applications, the breadth of any such patents, or whether any issued patents will be found invalid and unenforceable or will be threatened by third parties. Any successful opposition to these patents or any other patents owned by or, if applicable in the future, licensed to us could deprive us of rights necessary for the successful commercialization of products that we may develop. Since patent applications in the United States and most other countries are confidential for a period of time after filing (in most cases 18 months after the filing of the priority application), we cannot be certain that we were the first to file on the technologies covered in several of the patent applications related to our technologies or products. Furthermore, a derivation proceeding can be provoked by a third party, or instituted by the U.S. Patent and Trademark Office, or USPTO, to determine who was the first to invent any of the subject matter covered by the patent claims of our applications.

Patent law can be highly uncertain and involve complex legal and factual questions for which important principles remain unresolved. In the United States and in many international jurisdictions, policy regarding the breadth of claims allowed in patents can be inconsistent and/or unclear. The U.S. Supreme Court and the Court of Appeals for the Federal Circuit have made, and will likely continue to make, changes in how the patent laws of the United States are interpreted. Similarly, international courts and governments have made, and will continue to make, changes in how the patent laws in their respective countries are interpreted. We cannot predict future changes in the interpretation of patent laws by U.S. and international judicial bodies or changes to patent laws that might be enacted into law by U.S. and international legislative bodies.

Moreover, in the United States, the Leahy-Smith America Invents Act, or the Leahy-Smith Act, enacted in September 2011, brought significant changes to the U.S. patent system, including a change from a “first to invent” system to a “first to file” system. Other changes in the Leahy-Smith Act affect the way patent applications are prosecuted, redefine prior art and may affect patent litigation. The USPTO developed new regulations and procedures to govern administration of the Leahy-Smith Act, and many of the substantive changes to patent law associated with the Leahy-Smith Act became effective on March 16, 2013. The Leahy-Smith Act and its implementation could increase the uncertainties and costs surrounding the prosecution of our patent applications and the enforcement or defense of our issued patents, which could have a material adverse effect on our business and financial condition.