Alpha Pro Tech (APT on the NYSE), my proxy for the CoronaPanic, is up 3%, while the S&P 500 is up 3.5% compared to yesterday’s slaughter.

My guess is that this is, with respect to the markets, 80%-90% over, but noting the actual spread counts in the USA/Canada are probably 20% done. Please note I’ve been badly wrong on my timing during this whole panic so take any predictions with a grain of salt, and they change with incoming information. There will be serious damage in terms of supply chains, and GDP to tourism and public-crowd related events (the cruise ship industry is toast, and anything relying on a shopping mall or foot traffic for discretionary consumer sales, e.g. clothing retailers, is in big, big trouble – thinking about TLRD here). On the flip side, Dollarama (TSX: DOL) is a great place to buy cheap panic supplies!

Companies that are close to debt covenants will likely tip over and when the banks come calling, it will not be pretty, but just for them and the financials. Certain corporate debt issuers look very interesting, spreads are hugely wide.

The infected accumulation curve will increase quite rapidly in the USA, and Canada. That said, the new phraseology of “social distancing” will stick and people will discover new-found time at home.

China, Hong Kong, Taiwan, Japan, South Korea, and even places that you don’t ordinarily associate with public cleanliness (Thailand, Malaysia) have it under control. Even if you don’t believe the stats coming out of China (which you shouldn’t, ever), the other countries do have reporting mechanisms that are relatively more trustable. In particular, SARS taught anybody coming out of Hong Kong about how to react and behave. This culture will come to North America and in the longer run, will improve our society.

Nobody seems to be talking about climate change anymore. I wonder why!

The media will hype this up to the point of being one of those “outbreak” movies, with the reality being somewhat more muted, which is:

* around 80% of the people that catch Covid-19 don’t get any symptoms at all

* those that are seriously affected or die from it are older (65+) people prone to other conditions (heart, lung)

The governments are in a ‘stuck’ position, mainly if they panic too much, they look stupid, while if they don’t panic enough, they will be accused of not panicking enough. They’re stuck in a rock and a hard place, but the Government of British Columbia has struck a very nice balance between these two.

There might even be a cultural change where telecommuting may be even more acceptable than it is at present. This has been going on at a snail’s pace, but Coronavirus will accelerate it. Will office REITs be killed?

Netflix, Amazon Prime Video, Hulu will receive record subscriptions; internet providers are going to deliver record amount of bandwidth.

There will be a considerable element of demand destruction in North America over the next month, but after that, things should normalize. Fundamentally, life continues, and pension funds need to make their returns. The character of the returns, however, will be somewhat different because interest rates are once again at the zero boundary. There will be a drive to TINA – There is No Alternative, which means that the drive for yield will be very alluring. You can’t invest in bonds (zero return, or you’ll probably get a 2-3% spread on BBB-A type issuers), so equity will be the only game in town (once again).

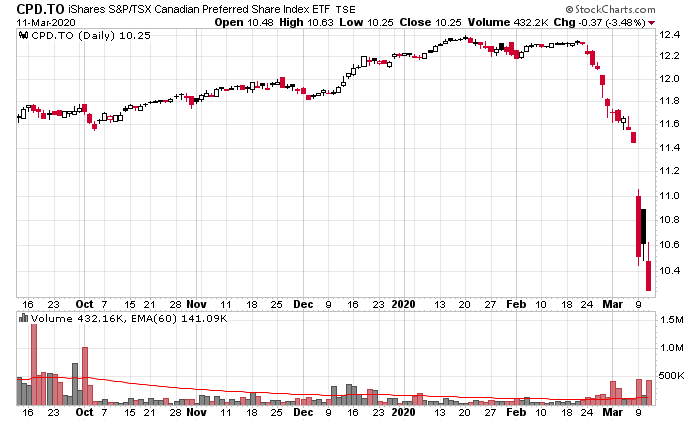

Gold, the last safe haven, people are still discovering like preferred shares and bonds, that it is not immune – right now gold is being sold to raise cash to buy other “risk-on” assets, but once the Federal Reserve and other central banks polish off their 2008 game plans and re-execute it, the currency depreciation should flow into commodities in a dramatic fashion – this will include gold to a degree.

Another question is what happens with inflation. Right now with the demand destruction and possible collapse of debts by companies that were already teetering on the brink – this will likely cause a drop in CPI. But I’m wondering about the rebound effect – once that has all been dealt with over the next 12 months, will there be a shortage of goods/services available relative to the money supply? Will we be seeing a huge rebound in consumer costs circa 2021-2022? Just a thought.

Finally, the US and Canadian governments are going to blow deficits like you’ve never seen before. I’m expecting Canada to announce a $60 billion dollar deficit for the upcoming fiscal year. The US will probably blow a couple trillion dollars. They can do so, and have the financial capacity (interest rates are at zero, after all).

Where does all of this fiscal stimulus go? In an idea world, public infrastructure – stuff that will be actually useful and consume domestic goods and services. The question is whether it actually does so or not. But the underlying point here is that companies that have relatively large amounts of revenues from government sources – they will likely do well. Engineering firms, defense, etc.

In particular I’ll disclose a holding in BWX Technologies (BWXT on the NYSE) which specializes in nuclear engineering in defence and civilian fields. This position was acquired within the last week. While it has not been taken down nearly as much as most of the rest of the stock market, I am pretty sure this company will be higher in a year.

I have also taken a long position on the S&P 500 futures at the close of March 12, 2020, which was at 2475. Equity liquidity will reign, and nothing will be receiving liquidity more than the Apples, Microsofts, Amazons, etc., of the US universe. My price target is 3100. This is in absence of having conviction on anything other than a few select names of reasonably credible companies (e.g. BWXT) that I’ve done a ton of due diligence on prior to this crash.

Companies that can collect cash and nowhere close to any credit covenants/maturities are critical variables at this point.