The rest of the stock market is getting killed by the Coronavirus as well, but Canadian preferred shares are not much of an escape valve.

James Hymas reported today that:

It is noteworthy that the Total Return version of TXPR closed at 1,304.43 today. I will note that the value of this index on September 30, 2010 was 1320.92, so total return has been negative over the past NINE YEARS AND FIVE MONTHS and a little bit. That’s before fees and expenses. Remember those charts I published in the post MAPF Performance : August 2019 illustrating the downturn to date, comparing it to the Credit Crunch and remarking that there had been zero total return for seven years and four months? Well, those charts are now out of date.

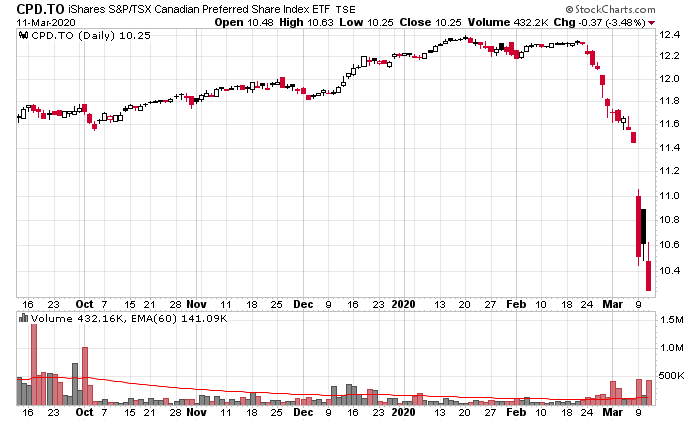

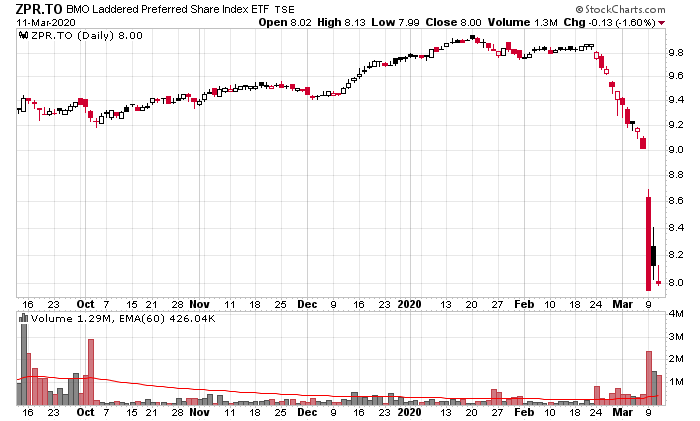

The two major ETFs which trade in Canadian preferred shares are ZPR and CPD, and they both have been murdered in the past two weeks, roughly 17%:

A negative total return of 9 years and 5 months can be contrasted against the TSX total return of about +4.5% (compounded annually) in the same period. In theory, preferred shares are safer investment vehicles than common shares, but clearly as the 5-year rate reset preferred share came to dominate the market, as 5-year interest rates have declined, they have also taken down the capital return of the preferred shares, resulting in very lacklustre long term performance.

This can only be considered to be a total washout that is going on.

One reason is perhaps that leveraged players are being forced to cash out. A retail example is in this reddit post, where the poster very thoughtfully constructed a diversified portfolio of preferred shares, and who is certainly underwater on this trade.

The math was pretty simple: Choose a “stable” preferred share (e.g. BAM.PR.Z) (4.7% and a rate reset of 5yr+2.96%, which presumably would be ‘stable’ since obviously the five year government bond will hover near 1.7% and you won’t get ripped off on the rate reset!). You borrow money at 3.3% from a proper brokerage firm, and leverage $100k of equity to buy $200k of stock, and voila. At the beginning of 2020, the shares would yield 5.9%, and your net would be 2.6%, minting a cool tax-preferred $2,600 in the process per $100k equity.

The problem is today, those BAM.PR.Z shares are worth $160,000, your net equity is down to $59,175 (had to pay the interest expense) and the only thing you will be receiving in this procedure is a first dividend payment of $2,928 tomorrow (which will correspond with a drop in the price of the preferred shares, so this is a push). Your margin level has gone from 50% to 37%, and this is precariously close to the 30% level which is allowed by the IIROC list of securities eligible for reduced margin and the brokerage firm.

Surely these preferred shares couldn’t go down further, to the point where you’re going to be forced to clear out your account? Can you take the risk being so close to the brink of a margin call?

This is part of what is going on. The other aspect is that the market is pricing in the reduced dividend rate that will inevitably occur with the rate reset. At a 5 year government of Canada bond rate of 0.55%, that BAM.PR.Z yield, after the reset, will go from 5.9% to 4.4% on original cost, which cuts heavily into the original intention of the trade, which was to skim a leveraged return off the dividend. The only solace is that the short term interest rate (that you would pay for margin) also decreases, but then your capital is impaired – you can realize the capital loss today, or wait patiently and hope for better times and hope things don’t get worse to where you will face that margin call.

These two factors I suspect are driving the push down in preferred shares. What will be even more fascinating is if we enter into a negative yield environment – preferred shares will look even uglier then.

Even the preferred shares with minimum rate guarantees (e.g. TRP.PR.J – 5.5%, reset at 4.69% with a minimum of 550bps) have not been immune to selling – although you are guaranteed a 5.5% coupon payment (and traded at a 4% premium to par for this minimum rate privilege to yield 5.3%), this series has been sold down in the past few weeks to 91.5 cents of par, or a minimum yield of 6.01%. Fascinating times.

Fortunately a couple weeks ago I sold all of my preferred shares short of a 2% position in something which I’m still not happy at myself for not unloading when I saw the proper bid for it.

Finally, the only solace for the rate reset preferred shares that are resetting at the end of March is that five years ago, the five-year government bond rate was 0.93%. I bet the people receiving that rate never thought they’d be getting a lower rate at the end of this month.

If the price of oil stay low, if we enter a recession, there is scenario well the gouvernement of Canada get in trouble with their debt, pushing the rate on the on the 5 year bond higher, then pref shares will outperform.

No idea if that plays out, but it’s something to keep in mind.

In my hypothetical scenario above with BAM.PR.Z, somebody using margin to invest would have been cashed out – they are down about 18% from when I did the post on March 11th. Loan to value would have been about 23%, so they would have force-sold the position well before then.