It is very important to remember that all of the trading that happens on the financial markets do not create or destroy anything – money and the asset is simply transferred, and the only change is the price that the asset is transferred. There are minor slippages (e.g. commissions and SEC fees) but for the most part, on a daily basis, it is a closed loop system.

The options market is completely zero-sum over the long run – every dollar a participant makes has to come out of the pocket of another participant. When option contracts expire, this is when the ultimately reconciliation occurs to zero the sum of transactions.

The stock market differs somewhat in that, as an aggregate, companies accumulate profits at the end of the day, and shareholders are recipients of these profits. It is a positive-sum game. Unlike option markets, however, equities are perpetual instruments (until bankruptcy or takeover/dissolution) and thus over time, the asset values of market participants should increase at the rate of company profitability, plus or minus the speculative forces we see each day when the market opens.

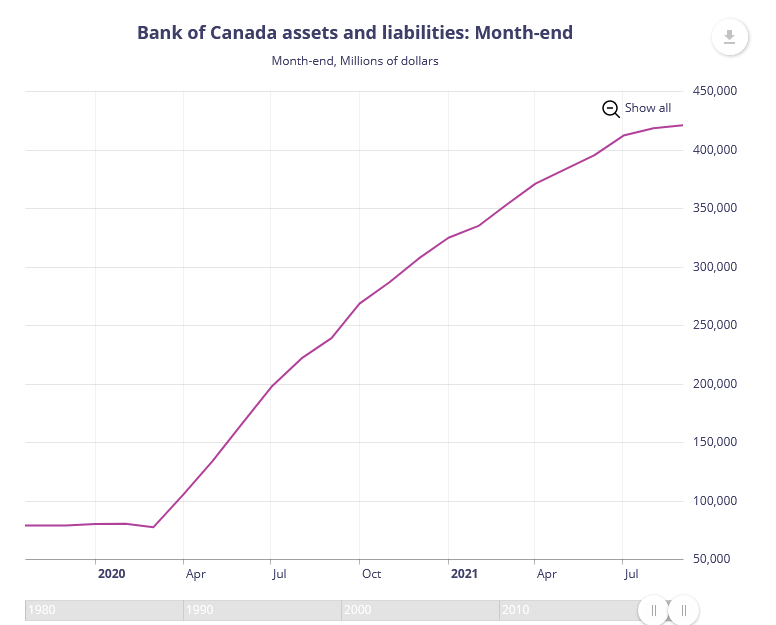

The lubricant that makes this occur is cash, and this is provided in the form of credit extended by financial institutions and ultimately backstopped by the central banks.

When there is more cash out in the system, it increases the demand for productive assets seeking a return. Likewise, when participants feel insecure or not as risk-taking, the demand for cash depresses demand for assets and will result in a drop in asset prices.

A simple numerical example suffices. If your ideal portfolio fraction is 80% equities and 20% cash and you have a total of $100 in your system, you want to own $80 of equities and $20 cash. If your shares rise in value, you sell a little of it to maintain your 20% cash fraction, while if your shares drop, you buy a little bit of stock to get back to 20%. If monetary policy suddenly infuses you with another $100 of cash, suddenly you will want to buy $80 more in equities to balance your portfolio. The residual cash goes towards an increase in asset value – and you see this everywhere with the stock market and real estate. Increasingly, this cash is starting to diffuse in other outlets, such as cryptocurrencies, NFTs, collectables, used vehicles, and so on.

One of my predictions for 2022 is that liquidity in the form of drenching the economy with cash is not going to solve real world economic problems. It will instead worsen them. Indeed, what we are seeing today is exactly a result of this – it is a world where (thankfully not literally, I am using some hyperbole here) everybody becomes a day trader. Every minute spent tapping a buy or sell on Wealthsimple (or perhaps Crypto dot com) was a minute that may have been spent producing good or service in the economy.

Perhaps day trading is too dramatic an example – and perhaps slightly exaggerated – but we also see this in the real estate market – many are jumping into the real estate agent game – how many times can a land title be flipped in a year?

The phenomena of “no supply at any price” is going to occur with higher frequency in 2022 in the real world. Unlike the financial analogy (e.g. the Volkswagen short squeeze of 2008), this is increasingly going to happen in the real world where only extreme amounts of money can bring supply of specific real-world products. A trivial example currently going on is purchasing a vanilla-styled iPad – they’re not available until the end of February.

This issue of “no supply at any price” will especially occur in price inelastic markets. Energy is one obvious example of a product that will be in very high demand and supply provisions are increasingly becoming expensive (whether politically or geologically) to procure. Another example will be specialized services (e.g. nuclear engineering or other ultra-specialized trades).

Just imagine being involved in a business that involves the assembly of many disparate elements involving multiple suppliers. If one or two of your key suppliers develops 2-3 month lead times, how the heck can you plan on your end the labour component for assembly? It means that you must start stockpiling. This will have a ripple effect return on equity for many businesses, but it will also translate into higher prices. This will go on until there is a demand collapse and only then we will see lower prices.