Lots of headlines are being made about Turkey and its currency, the Turkish Lira:

(The chart with the Turkish Lira to US dollar is very similar).

(Wikipedia Article on the matter)

Turkey’s GDP is about half of Canada’s (i.e. not an insignificant economy).

A lot of the cause of the currency depreciation appears to be the leveraged borrowings in foreign currency by domestic companies coupled with the domestic government wanting to keep interest rates lower than the prevailing market rate.

As a result, the purchasing power of the domestic currency has declined significantly. Even the basic math of accounting changes when dealing with a rapidly inflating currency. Just imagine marking up all of that foreign debt on each quarterly financial statement – normally the foreign currency translation adjustment component of equity on the balance sheet is some small fraction of the overall picture, but in this case, comprehensive earnings becomes a very important figure to watch – your business might be making 500 units of profit, but if foreign currency liabilities increase by 5,000 units of domestic currency, you’re toast!

Since Turkish inflationary headlines have reached the mainstream, chances are there is some actionable ideas, but I am not enough of a macroeconomic professional to truly figure out where things are headed.

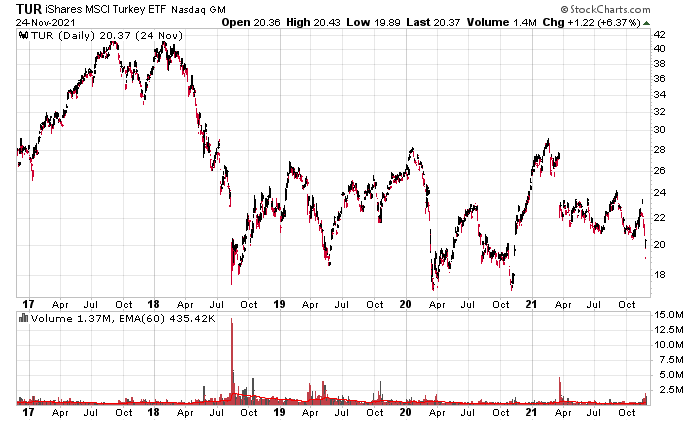

On the domestic side of things, Turkish stocks have been a better store of value than pure Lira:

The preceding chart is the iShares MSCI Turkey ETF, the only broad-based Turkey ETF I could find. It is denominated in US Dollars.

Despite the Lira depreciating 75% over the past five years to the US Dollar, the ETF has “only” lost about 25% of its value denominated in US Currency.

Obviously, when the companies that constitute the index have heavy amounts of foreign currency debt, the equity will be taking a considerable hit as companies try to service these debts with domestic cash flows. However, with the currency depreciating at the rate it does, it amounts to an effective interest rate on foreign debt that is very high. One possible conclusion is that there will be a foreign debt default with a subsequent recapitalization and/or nationalization of various strategic entities as I very much doubt the Turkish government wants its major companies to be foreign controlled.

The stock market is thus not a very good retreat if you are forced to live with a currency in a very inflationary environment. This has also shown to be true in other jurisdictions – initially the stock market makes huge gains (everybody is looking for a shelter for depreciating currency), but later the economic damages caused by high inflation rates eventually kills returns on the whole spectrum of the capital structure.

Indeed, there is a huge incentive to leverage at low interest rates (these debts would be repaid in much less real value) and purchase different assets, ideally liquid ones.

Holding USD itself (or Euro) would be a liquid store of value. A physical gold investor over the past 5 years not only would have made a 50% return in nominal US dollars, but the gains would be much, much higher in Turkish Lira. Having a mechanism of storing crude oil would also be a liquid store of value. There are plenty of options, some feasible, some not.

Here in Canada, if companies issue debt in non-Canadian dollar currency, it is most likely to be in US Dollars. Since most of our trade is linked to the USA (we are functionally joined at the hip with them) it is unlikely that we will face the same mechanism of currency decline as Turkey. If our export market starts to evaporate (e.g. we shut down our fossil fuel and automobile industries in the name of climate change) we will be in serious trouble.

Where should we put our money? In an unhedged US index fund? Gold? Certainly appears that our export market is under attack internally.