Higher prices means lower returns going forward. Overall prices are quite high right now. Therefore, expect lower returns.

The few times that I have been able to identify something of value over the past year, my primary issue has been to not add enough into it. Perhaps I am just over-cautious, or perhaps I am just getting old and do not feel the need to swing for the fences anymore. The most poignant example of this was my tepid entry into Premium Brands (TSX: PBH) early in 2025 in the $75-80 range, which should have been a 10% position but unfortunately was much less. Rationally, it is better to get a small position of something that appreciates rather than nothing, but emotionally it just feels like another lost opportunity plagued with regret!

Here are some thoughts in no particular order:

1. (no surprises here) Precious metals have gone wild over the past few months, but especially silver and platinum:

Silver is most frequently mined as a byproduct of gold production and is a relatively ‘common’ element in comparison. However, platinum is a much more rarer metal (rarer than gold). It would suggest that platinum should be more expensive than gold, but currently due to historical factors and the fact that gold is used in higher quantities, especially in jewellery, it is not.

The pricing for precious metals is making me think about several questions –

a. High commodity prices will spur capital expenditures and more production. For physical mining projects, this will take half a decade and there will be a huge lag effect between the investment and when the supply will eventually hit the market – but it will eventually. The AI machine guesses that a ‘greenfield’ gold mine project will have an AISC of US$1,600-$2,200 per ounce and other projects will be less, so there is a gigantic margin to be made on this over the next couple years. When I look at the majors (e.g. Barrick Gold, etc.), it looks like that this story has already played out in the stock market.

b. In the late 1970s after many years of soul-crushing inflation, and short-term interest rates in the double digits, gold became a very popular way to escape. There were accounts of people lining up to buy gold and silver and of course this was the best time to be selling the precious metals and investing in US Treasury bonds. While I don’t see signs of that happening quite yet, there does seem to be some element of precious metal fever reflecting sentiment on the current state of our monetary system.

c. Is physical (or financial) ownership of precious metals displacing cryptocurrency? Is there going to be a “retro” trade? I was particularly intrigued when brokerage platforms (e.g. Wealthsimple) were advertising one-tap purchases of gold, and you can have it transformed into physical metal for a nominal fee. However, what will you do with it? Just put it in a display case and have it stolen like the crown jewels at the Louvre? At least, unlikely cryptocurrency, you can melt it and turn it into a piece of artwork or create some very conductive wire or something.

I am not a fan of holding physical metal. It is a huge security risk. I have one 2 ounce silver coin which I bought many years ago and it acts as a great paperweight on my desk. It doesn’t yield anything other than looking nice.

2. Telus’ “Look! Insiders bought back stock and we did a buyback of 1.5 million shares!” announcement.

Telus came up on my year-end stock screens. I am absolutely sure retail investors will pick them because they have an absurdly high dividend rate, yield is currently 9.3%. I guess when your dividend rate is so high a stock buyback makes sense on paper, but an issue is that the free cash flow going out the window for the past 12 months is higher than the regression to the mean – plus they are still spending billions in capex with no end in sight. While I have no doubt that over time there will be an element to an oligopoly price power to keep them afloat, I would view this public advertising of managing the stock to be a negative signal.

Telus has a ton of debt (about $30 billion net) which also puts them into a dangerous area where their free cash generation to gross debt levels is quite high. While their industry is very stable, it does make them vulnerable to an external shock that would involve withdrawing of credit – these are the times that one waits for to pounce, albeit it happens so infrequently that people get impatient and want to collect a 9% yield instead of waiting for the moment they can purchase shares for 50% cheaper.

The nearest comparable is Bell Canada (TSX: BCE), which is in slightly better financial position than Telus and they already cut their dividend to finance questionable acquisitions and shore up their heavily indebted balance sheet.

A general rule, however, is that if yield is the only thing you are seeking in an investment, you might get dissapointed. Telus sticks out like a sore thumb in this department and it makes me very, very suspicious, especially when seeing this press release from them.

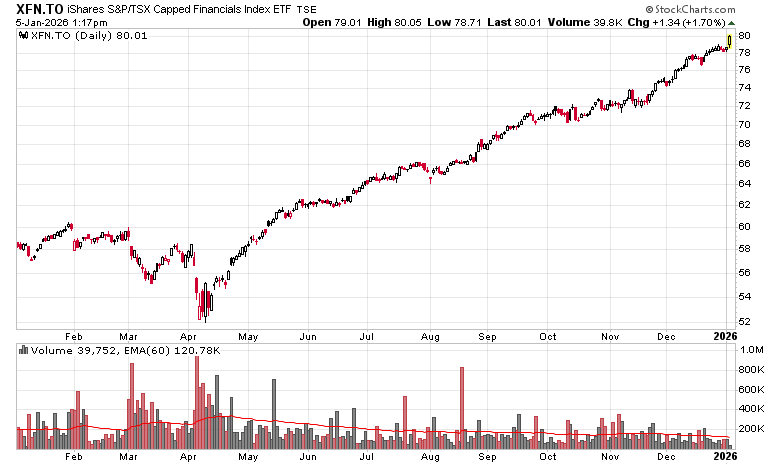

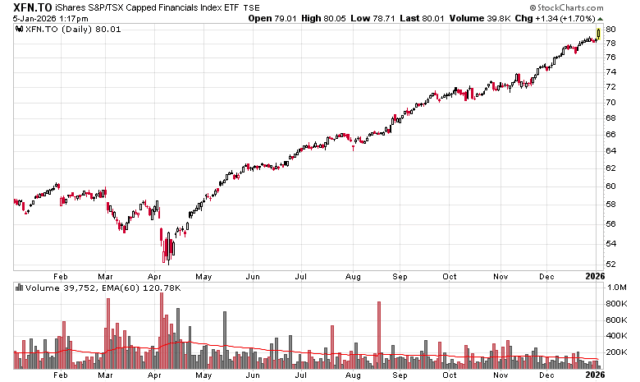

3. Money supply keeps on growing – Bank of Canada – $4.993 trillion in June 2025, $5.090 trillion in October 2025… where does that cash liquidity end up? Some of it in gold, platinum and silver of course, but also the TSX, which was up 32% (total return) in 2025.

Money is reflected by a journal entry – somebody’s credit is somebody else’s debit and the total sum of liabilities plus equity is equal to assets – the larger this number, the larger the nominal returns will be sought after, and the larger the inflation. Hence, we have the Canadian financial sector doing very well in 2025:

The Bank of Canada reducing interest rates from 4.5% to 2.25% just might have something to do with this chart!

4. The compression in real estate, especially in the residential condominium markets in Vancouver and Toronto, is starting to have an effect on rental prices and this is reflected in the price of CAPREIT (TSX: CAR.UN), albeit not today when I am making this post!

There is so much levered finance on real estate that governments and central banks have huge incentives to not letting things get too bad. I suspect things will meander on this front for many years.

5. Lower interest rates create abundant credit conditions, causing a huge chase for yield – preferred shares are now a wasteland (lots of issues trading at/above par), corporate credit spreads are narrow, and Canadian debentures are mostly at par – things in fixed-income land are just terrible if you want to make a high return.

On the Canadian debenture front, I do note that George Aryoman’s adventures into Slate Office REIT (now Ravelin, RPR.UN) doesn’t look like it is going too well – his entity, G2S2, is lending a good chunk of credit and this has been extended out and is now being paid 10%. RPR.DB is a $29M debenture that is outstanding on January 31, 2026 and the debenture series have not been paid interest for quite some time. My comments I made nearly three years ago about this train wreck have aged fairly well, “I quickly came to the realization there is no way for a financial flea such as myself to “win”.”.

6. Software has not done well in 2025. The market starling, Constellation Software (TSX: CSU) has fallen from grace, from $5000/share to $3,200 presently. Its twin cousin, Topicus (TSXV: TOI), also has exhibited a similar price curve. Both of them have been a valuation mystery to me.

However, more common-name companies are also feeling the crunch. Adobe (Nasdaq: ADBE) is trading at 3 year lows, presumably a brand and suite of software that has a following nearly as strong as people’s familiarity with the Windows operating system. As far as large-cap companies go, Adobe seems to be relatively cheap for what it is.

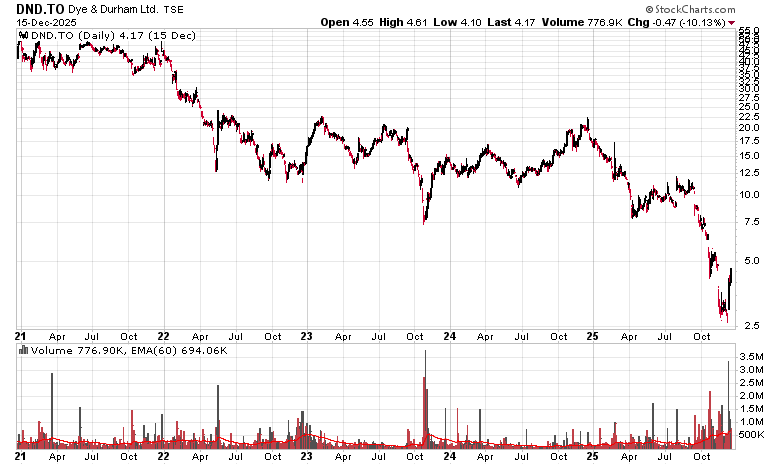

Finally, the drama at Dye and Durham (TSX: DND) or should I say, Dead and Durham? has not resolved itself. We also have companies that have not gone anywhere for seemingly centuries, including Calian Group (TSX: CGY), and OpenText (TSX: OPEN).

7. Energy and lumber are two commodities that have not done well. Despite energy, Canadian oil and gas has picked up a bid – sentiment has made a notable turn there. Lumber, on the other hand, looks to be depressed as the state of the real estate market is suppressing consumption. However, when this turns, there will be a massive spike up in lumber prices as supply constrictions have been significant. Thus, I would pay attention to lumber as a potential “sleeper hit” for 2026. Surely it can’t get worse for them?