(See previous article: November 4, 2022)

Unfortunately, due to my complete inability to properly read the warrant indenture for Mirion’s public warrants (NYSE: MIR.wt), they have called out their warrants because their common stock satisfied a particular call criteria. Unfortunately I was mislead to believe that they could only call out the warrants when the stock was trading above US$18/share when there was a provision that allowed for a call above US$10/share! Oops!

The announcement has the salient paragraph:

Warrant holders may continue to exercise their warrants to purchase shares of Common Stock until immediately before 5:00 p.m. New York City time on the Redemption Date. Holders may exercise their warrants and receive Common Stock (i) in exchange for a payment in cash of the $11.50 per warrant exercise price, or (ii) on a “cashless” basis in which case the exercising holder will receive a number of shares of Common Stock determined under the Warrant Agreement based on the redemption date and the redemption fair market value, as determined in accordance with the Warrant Agreement. The “fair market value” is based on the average last price per share of Common Stock for the 10 trading days ending on the third trading day prior to the date on which the Notice of Redemption is sent. In accordance with the Warrant Agreement, exercising holders will receive 0.220 of a share of Common Stock for each Warrant surrendered for exercise. If a holder of warrants would, after taking into account all of such holders’ warrants exercised at one time, be entitled to receive a fractional interest in a share of Common Stock, the number of shares of Common Stock the holder is entitled to receive will be rounded down to the nearest whole number of shares.

Given that the stock is trading at about US$10.90/share, there is no way that people would rationally choose to exercise for US$11.50/share. At 0.22 shares per warrant, the break-even price for the $11.50 strike provision would be about $14.70/share. So the warrants, for a month, are effectively trading at 0.22 MIR shares per warrant. They will get delisted on May 17 and if people did not exercise or sell them on the open market by then, they will get cashed out for 10 cents a piece for those too sleepy to take action.

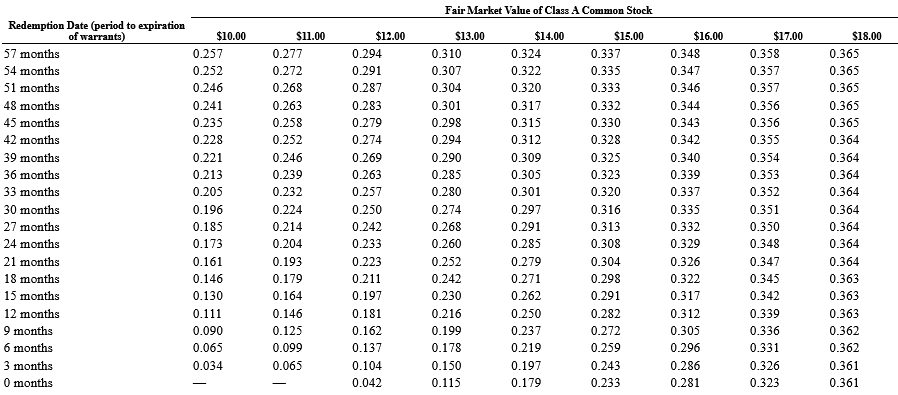

The 0.22 share conversion number came from a result of this table, which applies a premium to an early redemption when the stock is above US$10/share:

The warrants were to expire on October 20, 2026 and hence there are about 30 months remaining.

Anyhow, sadly I had to close off this trade – while my gross incompetence did not result in a loss, I do consider it a completely failed trade for my financial illiteracy.

The reason why this trade is so good for “nuclear insurance” is because of the embedded leverage of the warrants – especially the leverage that would occur if there was a nuclear event of prominence. The stock price would skyrocket and the percentage gain on the warrants would be astronomical. While the common stock is an acceptable way of achieving an “insurance payout”, the cost of capital is a lot higher than going down the warrant route. Essentially you just want to purchase as much out of the money as possible (just like how a life insurance policy is effectively selling a call option on the low probability expiration of your life!). The publicly listed equity options do not sufficiently go out in time and are illiquid so you will have to pay the market maker spread – the November 15, 2024 call options with a strike of 12.5 are trading at bid/ask 0.75/0.85, which is a terrible value compared to the October 2026, 11.5 strike for the warrants that were trading at $1.80-ish just a few days before this announcement. Too bad! This really hurt me.