In a decision that surprised nobody, the Bank of Canada kept the interest rates steady at 5% and gave the usual cautionary language that they’re watching the situation carefully.

However, my post is about the press conference the Bank of Canada held a day later, titled “What population growth means for the economy and inflation“.

In the Bank of Canada’s page describing this December 7 press conference, they highlighted the following quote (bold emphasis my own):

===============

“Strong immigration since the start of 2022 has helped increase Canada’s workforce…. And the larger workforce has boosted the level of our potential output by 2% to 3% without adding to inflation. This is a significant improvement, especially considering Canada’s otherwise rapidly aging population.”

===============

Then just a little bit lower down, we have the following (again, bold emphasis my own):

===============

The impact on inflation

When newcomers move to Canada, they need to buy many necessities to help them get settled. This increases demand for goods and services, which can have an impact on inflation.

Not all newcomers affect the economy in the same way. For instance, because of their high tuition fees, international students typically add to consumption more than many other newcomers. Overall, though, the initial boost to spending from the recent rise in newcomers has had very little impact on inflation.

But newcomers also need housing, and that’s a different story. Canada has long had housing supply challenges for many reasons, including:

* zoning restrictions

* lengthy permitting processes

* a shortage of construction workers

The result is that new housing construction has not kept up with population growth for many years.

With these housing supply challenges, the recent increase in newcomers has added to the pressure on rent and housing prices. And this has affected inflation.

Ultimately, Canada needs more housing, and the recent focus by all levels of government to increase construction is a welcome development.

===============

I take amusement in the phrases “without adding to inflation”, “which can have an impact on inflation”, “has had very little impact on inflation”, “this has affected inflation” all bundled together – talk about covering your bases!

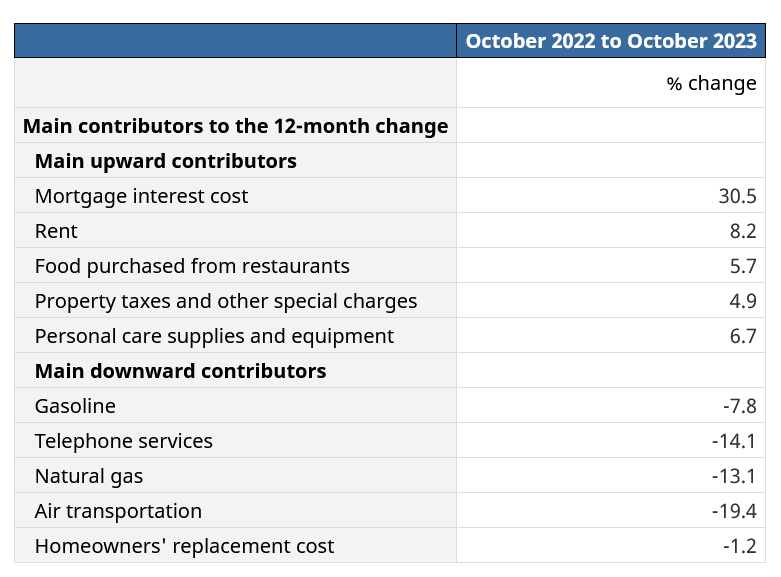

The Bank of Canada is just as much a political beast as our members of parliament are in Ottawa, but the way they express it is different in flavour. They are trying to telegraph something fairly obvious, in that the component of CPI that is contributing the most to inflation is related to real estate:

It does not take a Ph.D. in economics to determine that if you admit a million people into the country a year, and the increase in housing stock is well less than a million homes, that prices are going to rise.

That said, the year-over-year comps for mortgage rates (looking at 5-year and variable) is about to level off in 2024 and this component of CPI will abate. The Bank of Canada raised to 4.5% on January 25, 2023 before taking a pause and then raised to 4.75% on June 7, 2023 and 5.00% on July 12, 2023. Energy prices have dropped considerably year-to-year and this will also provide a tailwind to the economy.

It reminds me of a fictional economic scenario where a loaf of bread costs $1.00 and next year it goes to $2.00. Inflation is 100%, people panic, and then some action is taken. Next year, the load of bread costs $2.04 and then everybody cries victory that they have conquered inflation. This will likely be the result of some disastrous economic decisions made during the Covid crisis.