This post should not be news for anybody in finance, but it is worth refreshing fundamental principles of compounding and equity.

The most attractive feature of equities vs. debt is the effect of compounding. Stocks can rise infinitely while bonds have an effective price cap at the risk-free rate of interest.

To get on the equity gravy train and make outstanding returns, you need to have capital invested in a business with great prospects for reinvestment.

We will use an example of a debt-free company earning a perpetual $10 per year on a $100 investment, but the investment is of a style that does not scale upwards with further reinvestment. The long-term risk-free rate of interest is 2%. Our dream world also does not have income taxes or management expenses.

In this instance, the company can choose the following policies (or a blend thereof):

1) Give the money back to shareholders.

2) Bank its cash and receive 2% on that capital,

3) Speculate on other (preemptively higher-yielding) ventures.

If the policy option is (1) then in theory the valuation of this firm will be $500 (the risk-free rate of interest). The company will still generate $10/year for its shareholders whether the valuation is $100 or $500. An investor would be indifferent to sell the business for $500 and invest in the risk-free bond or just keep holding onto the business – you have magically created $400 of capital profit and you can clip dividends or bond coupons. With your $10/year you can do what you please, or put it in a risk-free 2% yourself.

This example is a constraint of reinvestment – after the re-valuation, your equity has effectively turned into a bond with no chance of compounding beyond the risk-free rate of interest.

If the policy option is (2) then you will see your returns in the appreciation of equity value. After the first year, your firm will generate $0.20 more in income and this will translate into $10 extra equity value, and this will compound at the rate of 2%.

Policy option (3) introduces the concept of risk – can management pull off the reinvestment? If there was an attractive investment at 5%, they would be able to generate $0.50 extra and this would translate into $50 of extra equity value for its holders, again, capitalized at the 2% risk-free rate.

So far we have made the assumption that the equity value follows lock-step with the risk-free rate of return. Of course in the real world, it never works that way and there are wildly divergent capitalization percentages used.

What is interesting is in this fictional example, the results you get if the initial equity investment does not trade at the risk-free return rate, but rather it trades at a higher rate, say 5%.

In this instance, the company would trade at an equity value of $200.

We will then consider a fourth policy option with the generated cash returns:

4) Buy back your own stock

This option requires a willing seller to the company (something that isn’t available to a 100% wholly owned firm!). Passing that assumption, an incremental deployment of $10 into the company’s own stock (a 5% reduction in shares) would result in continuing shareholders receiving 5.3% more returns in the future. Shareholders as an aggregate will still receive $10/share in returns, but the return per share will be 5.3% higher than before due to the reduced shares outstanding. This is a far better outcome than policy option (2).

The principle is the following: If a company is earning sustainable, long-lasting cash flows, it is to the benefit of shareholders that either the inherent business of the company has a capital outlay that offers higher returns on capital OR failing that, that the market value of the company’s equity is low to offer another conduit for reinvestment. Barring these two circumstances, returns should be given out as dividends.

This is unintuitive in that sometimes companies engage in really destructive practices with share buybacks. They are not universally good, especially if the future cash generation of the business is spotty. Likewise there are circumstances where buybacks work to massive benefit (a good historical example was Teledyne). However, in all of these cases, investors must possess a crystal ball and be able to forecast that the cash generation of the existing business (in addition to any other potential future capital expenditures) will be sufficiently positive over the required rate of return.

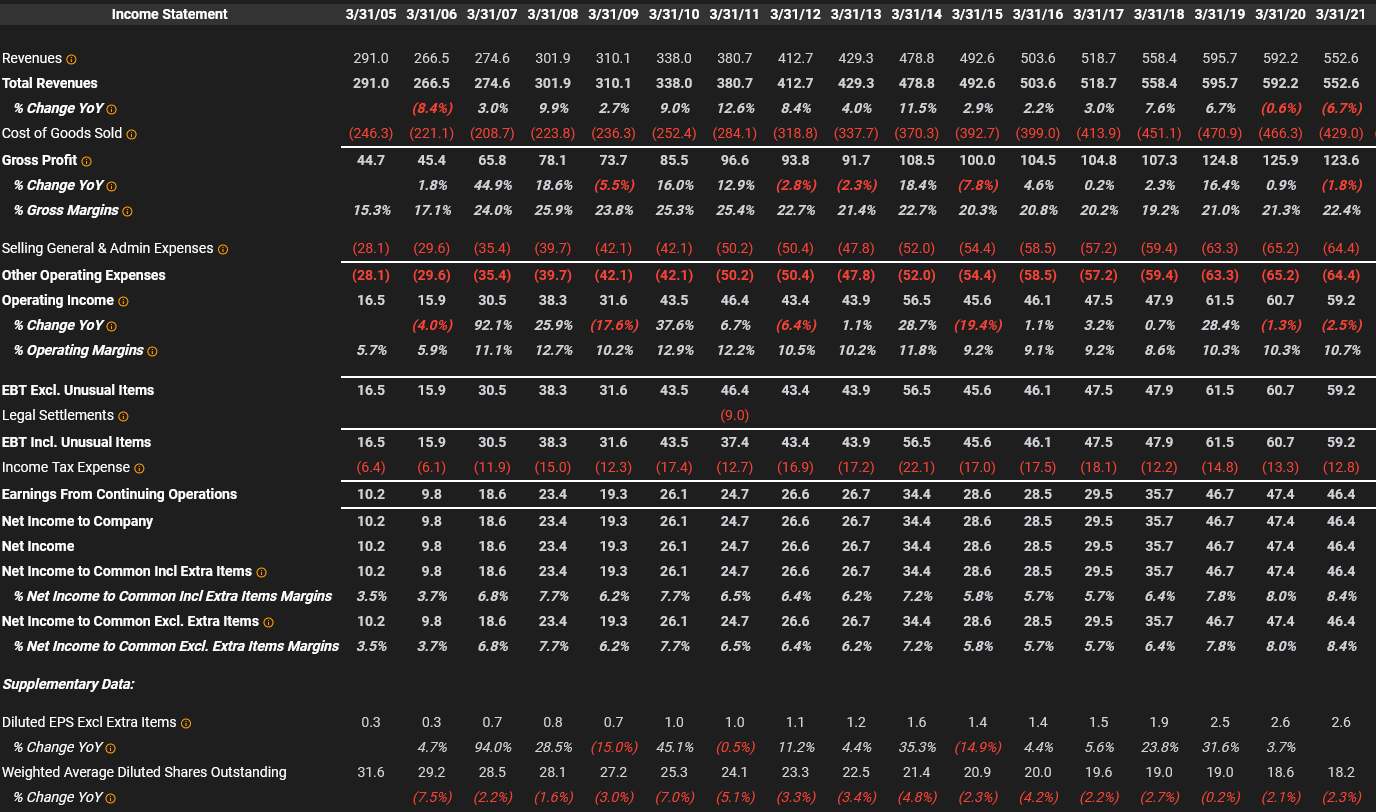

For example, Corvel (Nasdaq: CRVL) has a very extensive history of share buybacks:

The Company’s Board of Directors approved the commencement of a stock repurchase program in the fall of 1996. In May 2021, the Company’s Board of Directors approved a 1,000,000 share expansion to the Company’s existing stock repurchase program, increasing the total number of shares of the Company’s common stock approved for repurchase over the life of the program to 38,000,000 shares. Since the commencement of the stock repurchase program, the Company has spent $604 million on the repurchase of 36,937,900 shares of its common stock, equal to 68% of the outstanding common stock had there been no repurchases. The average price of these repurchases was $16.36 per share. These repurchases were funded primarily by the net earnings of the Company, along with proceeds from the exercise of common stock options. During the three and six months ended September 30, 2021, the Company repurchased 165,455 shares of its common stock for $25.6 million at an average price of $154.48 per share and 284,348 shares of its common stock for $39.8 million at an average price of $139.81, respectively. The Company had 17,763,576 shares of common stock outstanding as of September 30, 2021, net of the 36,937,900 shares in treasury. During the period subsequent to the quarter ended September 30, 2021, the Company repurchased 49,663 shares of its common stock for $8.7 million at an average price of $176.02 per share under the Company’s stock repurchase program.

We look at the financial history of the company over the past 15 years:

This is a textbook example that financial writers should be writing case studies about up there with Teledyne (NYSE: TDY) as this has generated immensely superior returns than if they had not engaged in such a buyback campaign. Share repurchases made over a decade ago are giving off gigantic benefits to present-day shareholders and will continue to do so each and every year as long as the business continues to make money.

The question today is whether this policy is still prudent. The business made $60 million in net income and there stands little reason to believe it will not continue, but should the company continue to buy back stock at what is functionally a present return of 2%? The business itself cannot be scaled that much higher (they primarily rely on internally developed research and development expenses and do not make acquisitions).

It only makes sense if management believes that net income will continue to grow from present levels. One has to make some business judgements at this point whether the company will continue to exhibit pricing power and maintain its competitive advantages (in this respect it looks very good).

Another example we are seeing in real-time is Berkshire (NYSE: BRK.a) using its considerable cash holdings to buy back its own stock. In the first 9 months of this year, they have repurchased just over 3% of the company. There’s more value right now in Berkshire buying its own massively cash-generating options than there would be on the external market – the last major purchase Berkshire made was a huge slab of Apple stock in 2017/2018 which was a wildly profitable trade.

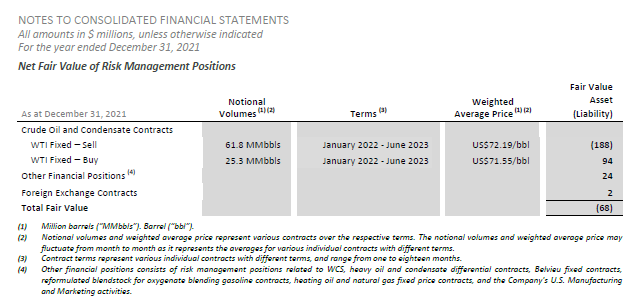

In the Canadian oil and gas industry, right now we are seeing the major Canadian companies deal with the first world problem of excess cash generation. They are all in the process of de-leveraging their balance sheets and paying down (what is already low interest rate) debt, but they are also funneling massive amounts of money into share buybacks.

For example, Suncor (TSE: SU) and Canadian Natural (TSE: CNQ) are buying back stock from the open market at a rate of approximately 0.5% of their shares outstanding each month. Cenovus started their buyback program on November 9th and intends to retire 7% of shares outstanding over the next 12 months. The financial metrics of these companies are quite similar in that with oil at existing prices, an investment in their own stock yields a far greater return than what you can get through the uncertainty of opening up a major project (good luck getting through the environmental assessment!). My estimate at present is around 15% return on equity for these buybacks and needless to say, this will be great for shareholders.

It is why an investor should want low equity market values as long as these buybacks continue and the pricing power of the companies remain high. In the oil patch, this of course requires a commodity price that by all accounts should remain in a profitable range for companies that have had their cost structures streamlined and capital spending requirements that have been curtailed due to a hostile regulatory regime. The returns from these share buybacks are likely to be immense, barring a collapse in the oil price.