There is no way to explain Bombardier selling out a 50.01% stake of its C-series jet (leaving it with a minority 31% stake, with the Government of Quebec with a 19% interest) to Airbus for zero other than the simple fact that they ran out of money. They couldn’t keep things going for a few more years while all of the trade dispute issues played out.

With airbus fully incentivized to starting marketing the C-Series (and acquiring most of any industrial secrets contained within the aircraft design), they will be better positioned than Bombardier was with respect to the upcoming Boeing trade dispute (which will be a multi-year bloody battle, especially since Boeing has the full support of the US Government). One question internally for Airbus is how they will reconcile selling Airbus 319’s instead of CS300’s with this arrangement. Or are they just doing this to shut down the aircraft entirely?

The key paragraph is:

At closing, there will be no cash contribution by any of the partners, nor will CSALP assume any financial debt. It also contemplates that Bombardier will continue with its current funding plan of CSALP and will fund, if required, the cash shortfalls of CSALP during the first year following the closing up to a maximum amount of US$350 million, and during the second and third years following the closing up to a maximum aggregate amount of US$350 million over both years, in consideration for non-voting participating shares of CSALP with cumulative annual dividends of 2%, with any excess shortfall during such periods to be shared proportionately amongst Class A shareholders.

So Bombardier’s downside is US$700 million over the next couple years.

Long term, assuming this isn’t an agreement by Airbus to effectively shut down the C-series program, this should bode well for the C-Series program, which should remain in Canada and will have a more powerful marketing partner, but this is a negative for any upside to Bombardier – the promise of a wildly profitable commercial jet program will have now shrunk down to a 31% stake.

If I was going to use an analogy here, it is “Would you like 31% of something, or 100% of nothing?”. Bombardier seems to have taken the first option.

Bombardier has plenty of other cash-positive business units (Transportation and smaller-scale aircraft) that will be bringing in cash flows, but most of the upside in the business (via the promise of significant C-Series jet revenues) is gone.

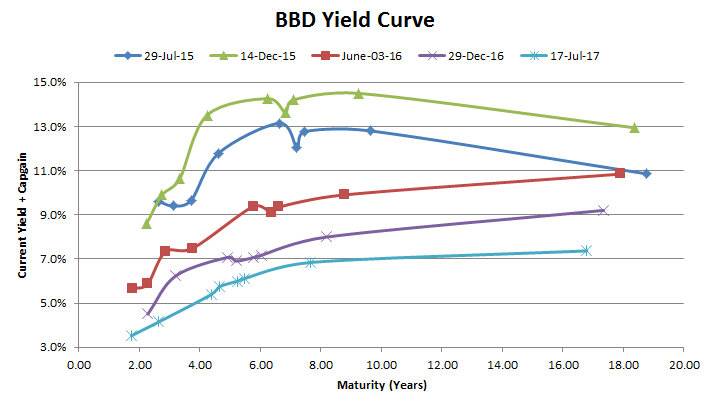

I continue to hold a much-diminished stake of BBD.PR.C and BBD.PR.D shares, of which I am tepid on valuation and still do not see any imminent (I added in this word a couple hours after making this post!) dividend risk despite this deal.