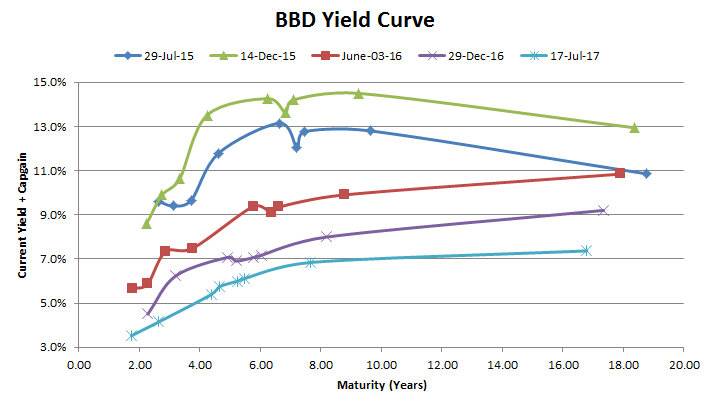

The yield curve of Bombardier continues to compress:

Despite all of the negative press concerning their trade war with Boeing for the C-Series jets, it appears that the credit market is thinking that the credit side of Bombardier is quite secure – offering less than 7% for 8-year money. The company can easily raise capital with its current yield curve.

The preferred shares have had some interesting action lately, and this is because of the repricing of the BBD.PR.D dividend – because of (from the company’s perspective) an ill-timed rapid increase of the 5-year Government of Canada yield curve, their BBD.PR.D series will be giving out 3.983% on a $25 par value of dividends. Around July 10th when the market was blissfully unaware of the dividend adjustment (as they apparently didn’t read press releases), this would have translated into a 10.8% eligible dividend yield.

It is because of this that the BBD.PR.C series has traded down – there is obvious arbitrage between the C-yields and the D-yields. They were originally trading a full 200 basis points away from each other but this has now converged to about 50 basis points which is more reasonable (BBD.PR.C is worth more if you plan on interest rates to decrease, while the D’s are better if you expect them to rise in 4.9 years).

In relation to Bombardier’s bond yield curve, the preferred shares looked extremely cheap (especially the BBD.PR.D series at 10.8% yield!). Now it is around 9.3%.

Disclosure: I own some BBD.PR.C and BBD.PR.D.

If you had owned BBD.PR.B, would you have exchanged them for BBD.PR.D? I was surprised that Mr. Hymas was indifferent on the choice but I am curious how many others exchanged their B’s for D’s or vice versa. I thought it was a very attractive option (I requested conversion of my B’s to D’s) and I’m honestly not sure if the Ds reacted right away to the higher dividend or if the Bs pulled them up with the hawkish BOC statement that day!

@Safety: It really is a call on what you expect future rate projections are. If you had to hold onto the thing for 5 years? I’d probably pick the B’s. If you can engage in rampant trading? Exchange for the D’s. Of course I say this with complete 20/20 hindsight so my comment is sadly not too useful.

As an interesting note I am speculating if Birchcliff Preferred A’s (September 30 is their 5-year rate reset date) will get called. They are 5yr+683bps so at a 1.5% GOC5yr, they’ll be paying more in dividends if they don’t exercise the call at the end of August. If it happens I won’t be too thrilled as it is so obviously a safe high payer.

Thanks for the BIR idea.

I guess my comment was in the past with any fixed reset conversion opportunity, Mr. Hymas, has always compared floaters to their strong pair and noted the floaters generally trade cheap so choose the fixed and trade into the floaters if the discount gets big. That’s been my strategy here as well. There are some other pref names of low credit quality (eg. AZP.PR.B; DC.PR.D) where the floater trades at a big discount to its strong pair and may offer an increasing dividend (if the 90-day t-bill rate resumes its ascent) and capital gains, all else being equal.

@Safety: This appears to be materializing with BBD preferreds right this very second. The yield diff between floating and fixed is huge (about 180bps with existing rates).

@Sacha Peter: You might be right. I have to think the BBD.PR.D yield downside is the BBD.PR.C yield in the short term but the yield spreads for AZP.PR.C/B and DC.PR.D/B are 30 and 50bps respectively. If we get down there, then downside for the BBD.PR.B is very big (at least on a relative basis). Does it make sense for BBD.PR.B owners to be way more optimistic on rate increases than AZP.PR.C or DC.PR.D holders?

@Safety: The B/D spread makes no sense to me, unless if there was a liquidity concern. I’m going to guess that most B’s converted to D’s, so there will just be one series trading at this point.

@Sacha Peter: Spread is too narrow or too wide? If you are right that most B’s converted to D’s then we might see a lot of selling of D’s after August 1 as those shares show up in accounts and people are able to sell. I’m not sure what people did but I wouldn’t be surprised if it’s less than half that converted.

Spread seems to be wayyyyyyyyyyy too wide at 163bps (which is what it is today at close). If there’s less than a million B’s outstanding then it all becomes a moot point.

“As an interesting note I am speculating if Birchcliff Preferred A’s (September 30 is their 5-year rate reset date) will get called. They are 5yr+683bps so at a 1.5% GOC5yr, they’ll be paying more in dividends if they don’t exercise the call at the end of August. If it happens I won’t be too thrilled as it is so obviously a safe high payer.”

I thought you mentioned the Pref C’s were the safer bet……I take it you must own both.

The C’s are redeemable by the holder on June 30, 2020. BIR retains the option to pay in common stock (95% of the 20-day VWAP or $2 floor). If you can get shares at par, it is a likely 7% return. At 102 cents on the dollar the return is about 6.2% which is not terrible considering the risk but I don’t think a portfolio manager would be getting financial accolades for the investment.

One of my semi-blunders in February 2016 was getting a bit too fancy (cheap!) on my accumulation scheme for the C’s – I got less than half of what I wanted before the bid started moving up on me.

thanks for the comment Sacha

@Sacha Peter It looks like there are now 6.2m BBD.PR.D and 5.8m BBD.PR.B outstanding following the exchange offer. The spread is between them is tightening which maybe should have been expected given the flows but I’m not sure how long it will last.

On a separate note, any thoughts on DC.PR.E? The YTM looks pretty interesting as one of few retractables out there. Perhaps, they will try to negotiate another extension but that discussion is still over a year away.

@Safety: The BBD B’s have baked in two 0.25% rate hikes to assume neutrality between the D’s.

I’m not interested in DC prefs. Although their asset base is likely to support preferred share dividends for some time, their underlying business is a shamble of cash negative entities. That said, they did raise another $105 million by dumping all their DRM and there’s a better chance than not that the E’s will be made whole in June 2019, but will the common shares be less than $2? The market’s discount vs. book value is an appropriate assessment of management’s past efforts…

http://birchcliffenergy.com/media/uploads/documents/pdfs/PressReleases/2017/1713-press-release-re-conversion-of-series-a-preferred-shares-final-170814.pdf

@Marc: I’m pleased that there’s no unwanted capital gain here. The market shot it up 50 cents for good reason – the call risk was keeping it capped. Now it will likely trade in the upper 26’s. Not sure if I’d want to do fixed or floating, but it’s a decision I can make after August 31st when they announce the final rates. Of course shareholders will have the luxury of waiting until the Bank of Canada announces short term rates on September 7th…