Tag: TOO

Dividend suspensions – Aimia, and soon-to-be Teekay Offshore

Aimia (TSX: AIM) suspended their common and preferred share dividends today. While this decision could have been entirely anticipated, the market still took the shares down another 20-25%. If you read between the lines from my previous post on them, this should not have been surprising. Nimble traders that were awake around 9:40am Eastern Time could have capitalized on an intraday bounce, but the current state of the union is likely to be short-lived since the company still has to figure out how to work its way out of a negative $3 billion tangible equity situation and pay the deluge of rewards liabilities. This will probably not end up well.

And in a “tomorrow’s news today” feature, it is more probable than not you will see Teekay management finally tuck in their tails and suspend dividends entirely on Teekay (NYSE: TK) and distributions from common and preferred units of Teekay Offshore (NYSE: TOO). When the announcement will be made is entirely up to management but it will likely be before the end of the month. What is funny is that I called it a couple weeks in advance (post is here), while it took a Morgan Stanley analyst a few days ago to actually cause a significant market reaction in the share price while everybody rushes for the exit. Teekay Offshore unsecured debt is now trading at 17% and with their preferred units still at 12%, it doesn’t take a rocket scientist to figure out what’s going to happen next – they desperately need a few hundred million in an equity infusion and they will be paying for it dearly.

As a bondholder in Teekay’s unsecured debt, I’m curious to see how management will bail themselves out this time. Since I do not believe they are interested in losing control, I still believe the parent company’s unsecured debt looks fairly good since there isn’t much ahead of it on the pecking order in the event of an unlikely liquidation event.

Thoughts on Teekay Offshore have not changed

Teekay Offshore (NYSE: TOO) reported their Q1-2017 results last night and they were lacklustre. In particular, the introduction of a litigation dispute with their largest customer, Petrobras, in respect of the operation of an offshore rig is not helping matters for them.

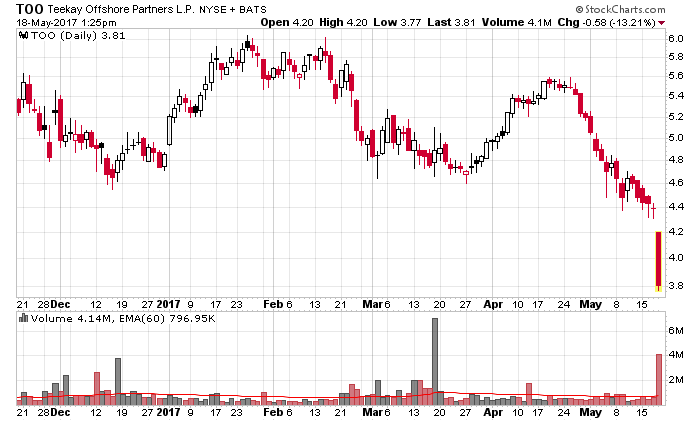

Last quarter I wrote about how Teekay Offshore units are “not going anywhere“, and that was an understatement considering this stock graph in the interm:

The next pillar to fall is their common unit dividend. Teekay traditionally declares dividends at the beginning of the calendar quarter and pays them out mid-quarter. I would expect there would be a 50/50 chance that they will suspend common dividends at the end of June or early July, and this would probably have a negative impact on their unit price. There is also an outside chance that they would decide to suspend their preferred unit dividends at the same time until they have shored up their financial resources.

The reason for this would be that they have not stabilized their financial position. With approximately 149.7 million units outstanding, the cash outflow of $16.5 million/quarter is something they really need to be putting into their outstanding debt. Preferred units receive around $11 million/quarter in cash in distributions and in a couple years, another series of preferred shares will switch from payment-in-units to payment-in-cash distributions (another $10.5 million/year).

Saving $27 million a quarter in distributions has to be attractive for a management that needs to repay $589 million in 2017 (this information is from their 20-F filing for their 2016 annual report). Cash flows through vessel operations will bridge some of this, but they are still missing some capital to make it through. They are also uncomfortably close to a debt covenant that they maintain total liquidity of at least 5% of their total debt (which is about $150 million in liquidity).

If you remember this chart from an earlier presentation when they got investors to chip in another $200 million in equity (April 2016):

CFVO (Cash flows through vessel operations) in Q1-2017 was $141.3 million, while net debt is ($3.12 billion gross minus $0.29 billion cash = $2.83 billion) – doing the math, we have ($2,830 / 4*$141.3) = 5.00 Net Debt/CFVO ratio!

This is way off the original 4.5x target as projected by management and this is getting into very dangerous territory where management has to take other measures to get the balance sheet back into a reasonable condition.

The only silver lining I can think of is that net debt has dropped $13 million for the quarter, but this is such a minor fraction of the overall net debt that it is relatively inconsequential.

Thus, I will predict that short of another form of recapitalization (or extremely dilutive equity offering), management will likely cut distributions from Teekay Offshore.

On a side note, I have gotten used to the “personality” of their quarterly reports and presentations as they release them and they are quite skillful at illuminating the information that they want you to be seeing and not paying any attention to the worms and termites that are crawling under the rocks. These nuggets of information are usually buried in the subsequent (weeks later) 6-K filings they report to the SEC. Also they are quite good at not reconciling their current situation with past expectations as you can see in the above post of their CFVO/Debt chart.

Teekay Offshore’s common units are not going anywhere

Reviewing Teekay Offshore’s financial results (NYSE: TOO), it strikes me as rather obvious that they have missed their initial early 2016 targets when they proposed a partial equitization (issuing common units, preferred units, and some refinancing) of their debt problems. They also borrowed $200 million from the Teekay parent entity (NYSE: TK).

In Q1-2016, they delivered a presentation with this chart:

In subsequent quarters, the company has generally not referred to progressing tracking to this projection, mainly because their debt to cash flow through vessel operations ratio has not met these targets. While the underlying entity is still making money, revenues are eroding through the expiration and renegotiation of various contracts, couple with some operational hiccups (Brazil) that is not helping matters any.

Putting a lot of the analysis away from this article, while in 2017 the future capital expenditure profile is going to be reduced (which would greatly assist with the distributable cash flows), the company doesn’t have a lot of leftover room for matters such as debt repayment and working on improving their leverage ratios in relation to cash generation ability. This leaves them with the option of continuing to dilute or depend on the parent entity for bridge financing. Indeed, one reason why I believe management thinks the company is still open for dilution is due to them employing a continuous equity offering program – they sold nearly 1.9 million units in the quarter at an average of US$5.17/unit. If they don’t think the company is worth US$5.17/unit, why should one pay more than that?

I don’t believe that they are a CCAA-equivalent risk in the current credit market (this is a key condition: “current” credit market), and I also believe that their preferred units will continue to pay distributions for the indefinite future, I don’t believe their common units will be outperforming absent a significant and sustained run-up in the oil commodity price. Note that there is a US$275 million issue of unsecured debt outstanding, maturing on July 30, 2019, which will present an interesting refinancing challenge. Right now those bonds are trading at around a 10% yield to maturity.

I have no positions in TOO (equity or debt), but do hold a position in the Teekay Parent’s debt (thesis here).

Teekay Corporation – Debt

Over the past couple months I have accumulated a substantial position in Teekay Corporation’s (NYSE: TK) unsecured debt, maturing January 15, 2020. The coupon is 8.5% and is paid semi-annually. I am expecting this debt to be paid out at or above par value well before the maturity date. The yield to maturity at my cost I will be receiving for this investment will be north of 20% (and obviously this number goes up if there is an earlier redemption).

I was really looking into the common shares and was asleep at the switch for these, especially around the US$7-8 level a month ago. Everything told me to pull the trigger on the commons as well, and this mistake of non-performance cost me a few percentage points of portfolio performance considering that the common shares are 50% above where I was considering to purchase them. This would have not been a trivial purchase – my weight at cost would have been between 5-10%.

However, offsetting this inaction was that I also bought common shares (technically, they are limited partnership units) of Teekay Offshore (NYSE: TOO) in mid-February. There is a very good case that these units will be selling at US$15-20 by the end of 2017, in addition to giving out generous distributions that will most likely increase in 2018 and beyond.

The short story with Teekay Corporation debt is that they control three daughter entities (Teekay Offshore, Tankers, and LNG). They own minority stakes in all three (roughly 30% for eachUpdate on April 26, 2016: I will be more specific. They have a 26% economic interest and 54% voting right in Teekay Tankers, a 35% limited partner interest in Teekay Offshore, and 31% limited partnership interest in Teekay LNG), but own controlling interests via general partner rights and in the case of Tankers, a dual-class share structure. There are also incentive distribution rights for Offshore and LNG (both of which are nowhere close to being achieved by virtue of distributions being completely slashed and burned at the end of 2015). If there was a liquidation, Teekay would be able to cover the debt with a (painful) sale of their daughter entities.

Teekay Corporation itself is controlled – with a 39% equity stake by Resolute Investments, Ltd. (Latest SC 13D filing here shows they accumulated more shares in December 2015, timed a little early.) They have a gigantic incentive to see this debt get paid off as now do I!

The mis-pricing of the common shares and debt of the issuers in question revolve around a classic financing trap (similar to Kinder Morgan’s crisis a few months ago). The material difference that the market appears to have forgotten about is that Teekay Offshore (and thus Teekay Corporation’s) business is less reliant on the price of crude oil than most other oil and gas entities. The material financial item is that Teekay Offshore faces a significant cash bridge in 2016 and 2017, but it is very probable they will be able to plug the gap and after this they will be “home-free” with a gigantic amount of free cash flow in 2018 and beyond – some of this will go to reduce leverage, but the rest of it is going to be sent into unitholder distributions assuming the capital markets will allow for an easy refinancing of Teekay Offshore’s 2019 unsecured debt.

At US$3/share, Teekay Offshore was an easy speculative purchase. Even at present prices of US$7/share, they are still a very good value even though they do have large amounts of debt (still trading at 16% yield to maturity, but this will not last long).

The absolute debt of Teekay Corporation is not too burdensome in relation to their assets, and one can make an easy guess that given a bit of cash flow through their daughter entities, they will be in a much better position in a couple years to refinance than they are at present. They did manage to get another US$200 million of this 2020 debt off at a mild discount in mid-November 2015, which was crucial to bridging some cash requirements in 2016 and 2017. The US$593 million face value of unsecured debt maturing January 2020 is the majority of the corporation’s debt (noting the last US$200 million sold is not fungible with the present $393 million until a bureaucratic process to exchange them with original notes) – I’d expect sometime in 2017 to 2018 this debt will be trading above par value.

The debt can be redeemed anytime at the price of the sum of the present values of the remaining scheduled payments of principal and interest, discounted to the redemption date on a semi-annual basis, at the treasury yield plus 50 basis points, plus accrued and unpaid interest to the redemption date.

This is a very complex entity to analyze as there is a parent and three daughter units to go through (and realizing that Teekay Corporation’s consolidated statements are useless to read without dissecting the daughter entities – this took a lot of time to perform properly). I believe I’ve cherry-picked the best of it and have found a happy place to park some US currency. I still think it is trading at a very good value if you care to tag along.