Teekay Offshore (NYSE: TOO) reported their Q1-2017 results last night and they were lacklustre. In particular, the introduction of a litigation dispute with their largest customer, Petrobras, in respect of the operation of an offshore rig is not helping matters for them.

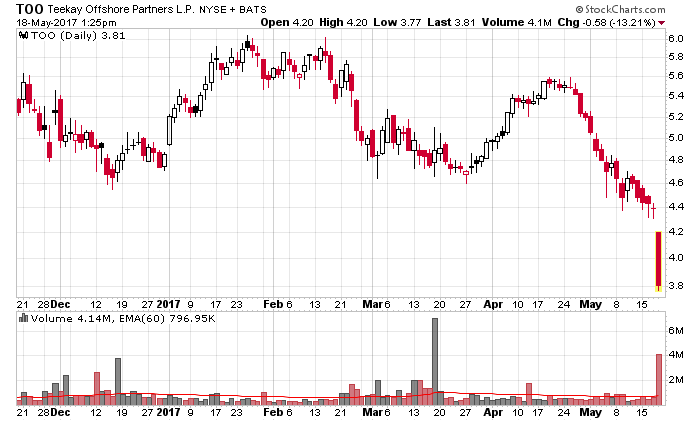

Last quarter I wrote about how Teekay Offshore units are “not going anywhere“, and that was an understatement considering this stock graph in the interm:

The next pillar to fall is their common unit dividend. Teekay traditionally declares dividends at the beginning of the calendar quarter and pays them out mid-quarter. I would expect there would be a 50/50 chance that they will suspend common dividends at the end of June or early July, and this would probably have a negative impact on their unit price. There is also an outside chance that they would decide to suspend their preferred unit dividends at the same time until they have shored up their financial resources.

The reason for this would be that they have not stabilized their financial position. With approximately 149.7 million units outstanding, the cash outflow of $16.5 million/quarter is something they really need to be putting into their outstanding debt. Preferred units receive around $11 million/quarter in cash in distributions and in a couple years, another series of preferred shares will switch from payment-in-units to payment-in-cash distributions (another $10.5 million/year).

Saving $27 million a quarter in distributions has to be attractive for a management that needs to repay $589 million in 2017 (this information is from their 20-F filing for their 2016 annual report). Cash flows through vessel operations will bridge some of this, but they are still missing some capital to make it through. They are also uncomfortably close to a debt covenant that they maintain total liquidity of at least 5% of their total debt (which is about $150 million in liquidity).

If you remember this chart from an earlier presentation when they got investors to chip in another $200 million in equity (April 2016):

CFVO (Cash flows through vessel operations) in Q1-2017 was $141.3 million, while net debt is ($3.12 billion gross minus $0.29 billion cash = $2.83 billion) – doing the math, we have ($2,830 / 4*$141.3) = 5.00 Net Debt/CFVO ratio!

This is way off the original 4.5x target as projected by management and this is getting into very dangerous territory where management has to take other measures to get the balance sheet back into a reasonable condition.

The only silver lining I can think of is that net debt has dropped $13 million for the quarter, but this is such a minor fraction of the overall net debt that it is relatively inconsequential.

Thus, I will predict that short of another form of recapitalization (or extremely dilutive equity offering), management will likely cut distributions from Teekay Offshore.

On a side note, I have gotten used to the “personality” of their quarterly reports and presentations as they release them and they are quite skillful at illuminating the information that they want you to be seeing and not paying any attention to the worms and termites that are crawling under the rocks. These nuggets of information are usually buried in the subsequent (weeks later) 6-K filings they report to the SEC. Also they are quite good at not reconciling their current situation with past expectations as you can see in the above post of their CFVO/Debt chart.

Already before I read your comments on presentation style, I immediately noticed the y-axes in the chart being conveniently chopped of to visually (subliminally) suggest net debt is significantly projected to decline.. Also notice that the y-axes are cut off at different points (they scale differently).

Managements that try to delude their bosses (owners), that’s a big no-no for me.

TOO is no doubt the trouble kid. But is the TK parent thesis still intact?

TNK was the trouble kid, while TOO is the troubled teen, and fortunately for TK, the responsible adult in the house is TGP.