Aimia (TSX: AIM) suspended their common and preferred share dividends today. While this decision could have been entirely anticipated, the market still took the shares down another 20-25%. If you read between the lines from my previous post on them, this should not have been surprising. Nimble traders that were awake around 9:40am Eastern Time could have capitalized on an intraday bounce, but the current state of the union is likely to be short-lived since the company still has to figure out how to work its way out of a negative $3 billion tangible equity situation and pay the deluge of rewards liabilities. This will probably not end up well.

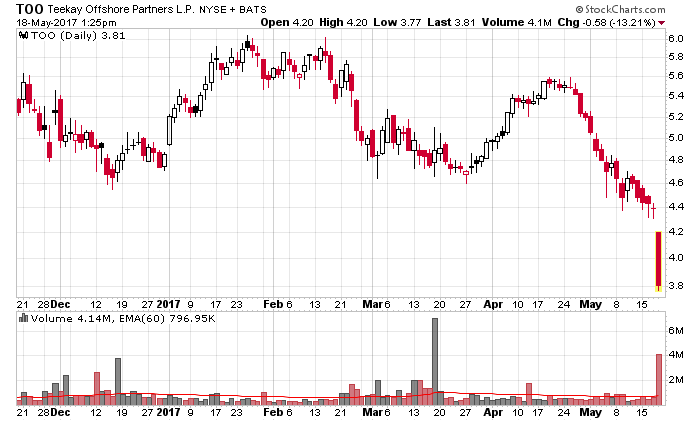

And in a “tomorrow’s news today” feature, it is more probable than not you will see Teekay management finally tuck in their tails and suspend dividends entirely on Teekay (NYSE: TK) and distributions from common and preferred units of Teekay Offshore (NYSE: TOO). When the announcement will be made is entirely up to management but it will likely be before the end of the month. What is funny is that I called it a couple weeks in advance (post is here), while it took a Morgan Stanley analyst a few days ago to actually cause a significant market reaction in the share price while everybody rushes for the exit. Teekay Offshore unsecured debt is now trading at 17% and with their preferred units still at 12%, it doesn’t take a rocket scientist to figure out what’s going to happen next – they desperately need a few hundred million in an equity infusion and they will be paying for it dearly.

As a bondholder in Teekay’s unsecured debt, I’m curious to see how management will bail themselves out this time. Since I do not believe they are interested in losing control, I still believe the parent company’s unsecured debt looks fairly good since there isn’t much ahead of it on the pecking order in the event of an unlikely liquidation event.