A mixed post.

Where I was mistaken

I made a claim earlier that I thought employment around January or February of this year would be shown to decline, presumably due to a slowdown in demand and companies cutting costs. Unless if you were one of the victims of a big tech company’s layoff, wow, was I ever wrong with this! Gross employment trends continue to exhibit strength, consistent with anecdotal reports of employers finding it difficult to source labour.

So where was I wrong here? Is there a demographic issue? Are companies out there finding additional vectors of demand to necessitate employment? Or am I just premature with my prognostication? I’m not sure.

There are some hints on the Fiscal Monitor – income tax collections and GST collections are up over comparative periods last year, and especially corporate income taxes. The government is likely to report an improved fiscal balance as well. This leads me to the second issue, which is…

The progression of QT

Members of Payments Canada (a.k.a. financial institutions parking reserves at the Bank of Canada and earning the short-term rate) continues to hover at the $190 billion level. The recent slab of government debt maturing off of the Bank of Canada’s balance sheet got directly subtracted from the Government of Canada’s bank account at the Bank of Canada, but the GoC is still sitting with $65 billion cash as of February 15, 2023.

What does this mean? The presumed pressure on liquidity is not happening – yet. Banks can still lend out capital, but you have to have an awfully good proposition since they’re not going to give it to you for cheap interest rates. Why should they lend it out to you at 6% when they can keep it perfectly safe at the Bank of Canada and skim their 4.5%?

While there’s liquidity, it’s definitely a lot more expensive. When you combine what I wrote about employment above, coupled with real estate finding its two legs again (helps that there is zero supply in the market), makes me think that the Bank of Canada was incredibly premature to call a pause on rates – March 8th they’ll be guaranteed to stand pat, but perhaps we might continue to see rate increases if CPI doesn’t drop quickly enough in the next couple months. Also, the US-Canada currency differential is also going to widen as the US Fed will be raising rates for longer.

A public market investor at this point is facing a crisis of sorts. Asset prices (unless if you owned garbage technology companies) haven’t deflated that much, so what is trading out there is really not the greatest competition for the risk-free rate. You have cash.to giving off a net 4.89%, and when you look at some average 20 P/E company, one has to ask yourself why you should be bothering to take the comparative risk. Just look at the debenture spreadsheet and the spreads over risk-free rates is minimal.

Commodities

In the middle of 2020, the trade was a no-brainer. Ever since then, it has become less and lesser so, to the point today where it is no longer about throwing capital into random companies and winning no matter what – discretion has been critical from about June of last year. The meltdown in the natural gas market is one example of where an investor could have turned into roadkill, especially with leverage. In general, you can lose less money by investing in low cost structure companies, ideally with as low debt as possible. The problem is if you have a whole bunch of industry participants in a good balance sheet situation – the race for the bottom becomes brutal since they can mostly survive low commodity price environments until some finally do get eliminated due to high cost structures and/or high debt service ratios.

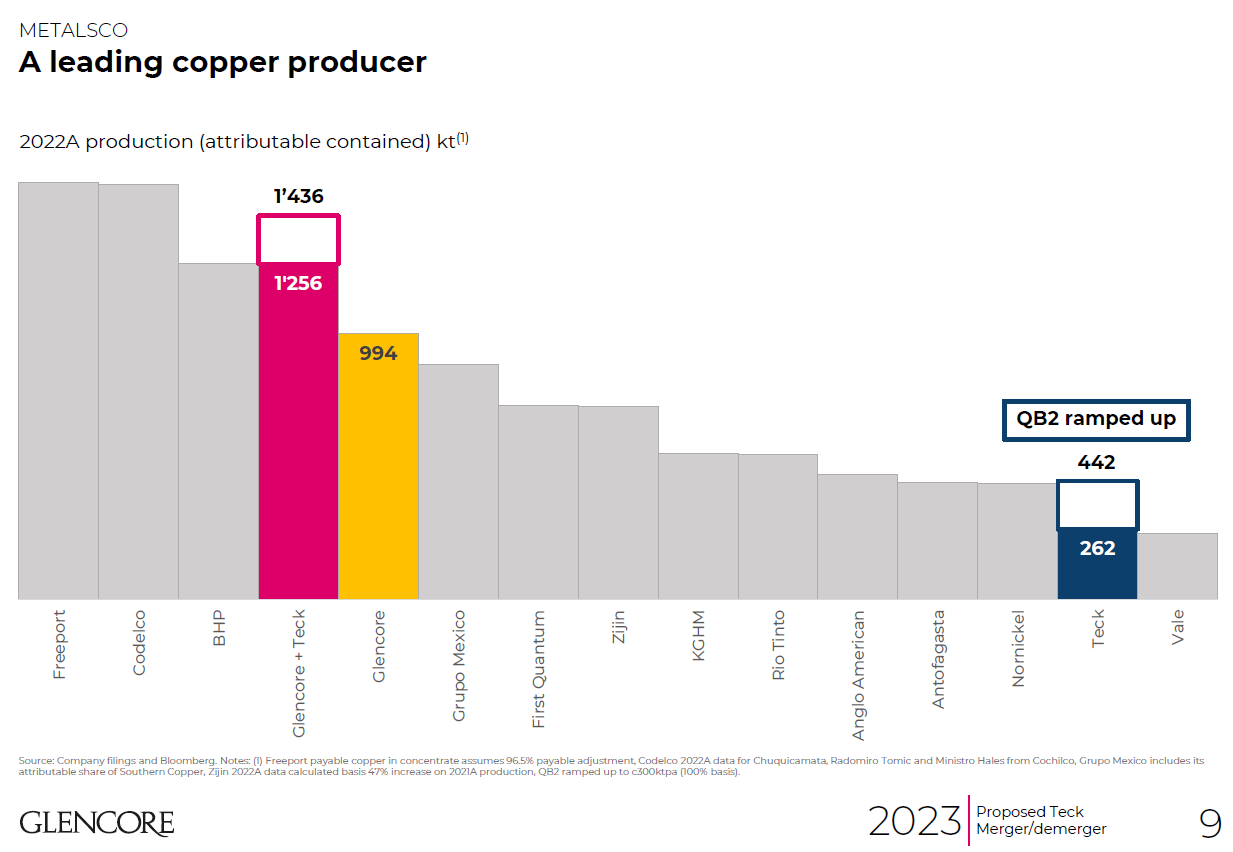

Teck

They explicitly had to disclose they’re looking into strategic options for their met coal unit, which would be a cash machine of a spinoff if they went down that route. Seaborne met coal has rebounded as of late and it would be really interesting to see the price to cash flow ratio assigned to a pure met coal unit. A comparable would be Arch Resources, and they are trading at 4x 2023 earnings. Teck does have considerable competitive advantages, however – better access to the Pacific and a lower cost structure, in addition to being able to pump out more coal. Stripping out the coal business would leave the copper and zinc business in core Teck, and the residual copper business might get a 20x valuation (looking at Freeport McMoran as the comparable here). When you do the math on both sides of the business (especially as Teck’s QB2 project is ramping up this year and will produce gushing cash flows at US$4 copper), the combined entity would be worth well more than $30 billion today. So with a little bit of financial engineering, Teck can generate market value from nothing.

Let’s look at the first 9 months of the year (which is abnormally high for met coal, but just to play along).

I have (for met coal) their gross profit minus capital expenditures, minus taxes, at around $4.5 billion annualized. Give that a 4x multiple and you have $18 billion. On copper, with QB2 at full swing, it should be (very) roughly $1.5 billion total for their consolidated copper operations and at 20x you get $30 billion. Add that together and it’s well over the existing market cap.

What you also do to complete the financial wizardry is that you load the coal operation with debt, say around $10 billion. Give it to the parent company as a dividend, or perhaps give it to shareholders as a dividend in addition to the spun-off equity and the projected return on equity will skyrocket (until the met coal commodity price goes into the tank, just like what happened two seconds after Teck closed on the Fording Coal acquisition before the economic crisis).

Despite the above calculation, I’ve been taking a few chips off the table. My overall position has continued to be of increasing caution, one reason being that I don’t have a very firm footing on what is going on.