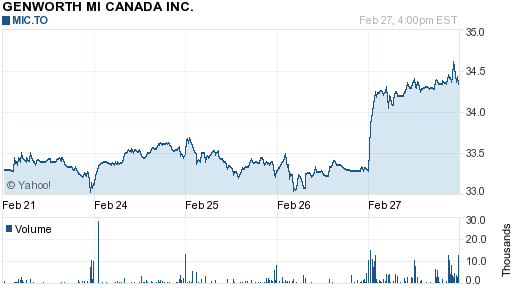

The earnings release was about what I was expecting. There was a slight increase in the expense profile but this was due to some stock-related compensation expenses (cash flow statement has it at $11.2 million for the year) but this is due to the stock itself increasing in value.

For the year, net premiums written were $511 million, while revenues recognized were $572 million. These two will have to converge eventually. This has been the trend for the past few years now – revenues recognized was $621 million back in 2010. Premiums earned in 2014 should be around the $550 million level.

The $5.4 billion portfolio continues to remain dull (a good thing) with a 3.6% yield, 3.7 year duration.

The loss ratio continues to remain exceptionally low, at 22%. Management continues to focus on Quebec and the Toronto condominium market, which is correct.

The bottom-line operating EPS is $3.60/share. Looking at tangible book value, I get a value of $32.34/share with a diluted share count of 94.9 million shares.

Balance sheet-wise, the company continues to remain over-capitalized with 222% of its required regulatory minimum capital, and well above its 190% internal target. There are regulatory changes which I have outlined earlier that the company is awaiting for before deciding what to do with its excess capital. They bought back shares when the stock was trading lower, but now they are holding onto their cash instead of buying back shares (a smart decision).

The only item of any distinction in the financials is the following paragraph:

On December 20, 2013, the Company, through its indirect subsidiary PMI Canada, entered into a retrocession agreement with Merrill Lynch Reinsurance under which the Company assumed reinsurance risk for up to $30,000 Australian dollars if the losses on claims paid by Genworth Financial Mortgage Insurance Pty Limited, an Australian company (“Genworth Australia”) exceed $700,000 Australian dollars within any one year. The term of the agreement is 3 years. Genworth Australia has the right to terminate the reinsurance agreement after the first year of coverage.

Under the excess of loss reinsurance agreement, the Company is required to collateralize its reinsurance obligations by posting cash collateral equal to the maximum exposure under the agreement in favour of Merrill Lynch Reinsurance. As at December 31, 2013, the Company has posted $30,000 Australian dollars, equivalent to $28,482 Canadian dollars, under the agreement. The collateral is recorded as collateral receivable under reinsurance agreement on the Company’s condensed consolidated interim statement of financial position.

Re-measurement adjustments arising on translation of collateral receivable under the reinsurance agreement and any reinsurance receivable balances from Australian dollars to Canadian dollars are recognized in net investment gains.

This is functionally a bet by management that the Australian real estate market is not going to crater. While I am not thrilled that the company appears to be engaging in gambling outside of the Canadian sphere, I do note that the history of paid claims in Australia appears to be considerably below this:

2013 – AUD$185 million

2012 – AUD$287 million

2011 – AUD$112 million

2010 – AUD$171 million

2009 – AUD$173 million

2008 – AUD$146 million

It would appear that it would take a disaster for Australia’s paid claims to be above the AUD$700 million threshold, but if this was the case, then why did Genworth Australia make this agreement with a sub of Genworth Canada?

Reading between the lines on the conference call, it sounds like management is tinkering around with the idea of deploying their excess capital in reinsurance of mortgage insurers. This doesn’t sound like a bad idea, until it blows up, like it almost did for the parent Genworth (NYSE: GNW) entity.

In absence of any better investment alternatives and also in absence of any looming Canadian real estate crisis, Genworth MI is still in my portfolio as a large fraction. It is or more less a proxy for a bond fund at this point and I am comfortable with the relevant risks regarding the Canadian real estate market. I also believe the equity is in the middle of what I consider to be its fair value range. If they execute as they have in 2013, the stock should go up another 10% or so on the basis of increased book value alone.

The critical sensitivity continues to be the state of the Canadian economy. Our country is export-oriented, especially in the commodity sector. As long as this remains active, we are unlikely to see spikes in unemployment that would cause mortgage defaults. Interest rates are also projected to be low and this will not create an additional shock in the market.