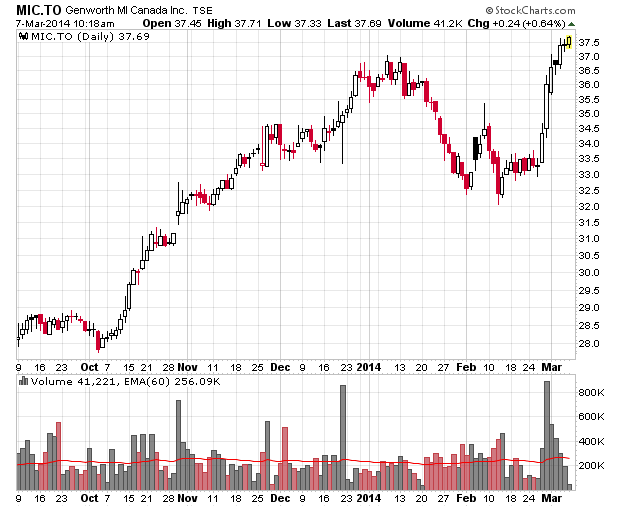

The largest component in my portfolio continues to be Genworth MI (TSX: MIC).

The stock is trading at an all-time high today.

I acquired shares in July and August 2012 and have been patiently waiting. I took quite a large initial stake to begin with and I have done well by this decision, but the appreciation is getting to a point where the portfolio fraction is getting too concentrated. Unfortunately, I very much doubt mortgage insurance will be the next big hype in the financial marketplace unlike Twitter, Facebook and 3D printing! (Or if Marijuana is your thing, check out shares of Advanced Cannabis!)

A couple canary in the coal mine analogies include Equitable (TSX: EQB) and Home Capital (TSX: HCG) which interestingly enough, have not exhibited the deprecation that most mortgage REITs in the USA have. Just because this has not happened doesn’t mean it will not happen in the future – right now the economic climate in Canada is relatively stable, but this remains dependent on the commodity industries remaining solvent. I do note that the Canadian dollar has depreciated somewhat over the year, which would be supportive to Canadian real estate valuations. Also looking at the charts of EQB and HCG, it does not look like the canaries are in ill-health at all.

That said, my valuation metrics show that MIC is in the upper end of my fair value range and I have slowly start trimming my position in 2014. They’re almost at 20% above tangible book and I expect they will be booking about $3.60-3.80 EPS in 2014. I would estimate there is some upside left, but it isn’t a huge amount compared to what we have seen over the past 18 months, and it would be momentum-driven rather than any valuation-centric investors.

The recent CMHC announcement to increase mortgage premiums resulted in a nice one-time spike in the stock, but the market might not anticipate that this will have a dampening effect on demand for mortgage insurance itself. Time will tell. The other headwinds of concern is that loss ratios are at historical lows, and one wonders how much more potential unknown good news there is out there for the company.

Momentum and some potential for a catalyst-type event (especially with their huge cash hoard they have been sitting on) have kept me from hitting the sell button too quickly – historically my sales have had much worse timing than my entries. My exit will be slow and gradual and only if the common shares continue to appreciate – otherwise I am fairly satisfied at present to just clip dividend coupons and keep the capital in something other than cash, which has been increasingly difficult to deploy these days.

My only fear is simply one of greed – I can conceivably see momentum trading taking MIC far above what rational analysis would suggest is a fair value. Trimming the position, instead of eliminating it outright, is the rational way of addressing this – if they do shoot to the moon like they are a social media stock, I will have some participation.

Sell half at the very least. We both won this round.

I sold my whole MIC stake back in 2013 at around the 34-35mark and stuck the proceeds in some REITs and index ETF’s. I believe they have returned about what MIC has gone up since I sold but with much less exposure to one issue.

Let’s not get greedy. 100% return in two years is just fine. If you’re getting nervous about the outsized position, it’s your conscious telling you it’s time to lighten up.

Just my two cents – remember I bought mine at $17, about 5 cents away from the 52 week low. Calling the bottom or the top is sheer luck.

Hi Cannikin, I did sell some shares today and will likely continue doing so as the stock appreciates. How much depends on how high the price goes.

My guess is that other than the CMHC announcement (which is undoubtedly a plus), income ETFs are picking up a portion the demand for shares. This is the 8th day in a row it is up on higher than normal volume.