Apparently some institutional shareholders are feeling the political pressure of the company’s ridiculously high executive compensation schemes. They’re voting against the “say on pay” resolution on the upcoming AGM.

Major Bombardier Inc. shareholder and supporter Caisse de dépôt et placement du Québec is voting against the company’s executive pay practices at its coming shareholder meeting.

It’s one of a number of major North American pension plans that intend to rebuff Bombardier’s compensation program. Some, including the Caisse, have grown sufficiently discontented to oppose reappointing directors to the company’s board.

Bombardier, like most major Canadian companies, submits its compensation program to shareholders for a non-binding “say-on-pay” vote at its annual meeting. Canada Pension Plan Investment Board (CPPIB), British Columbia Investment Management Corp. (BCI), as well as two major pensions from California and one from Florida, also say they are voting “no” Thursday.

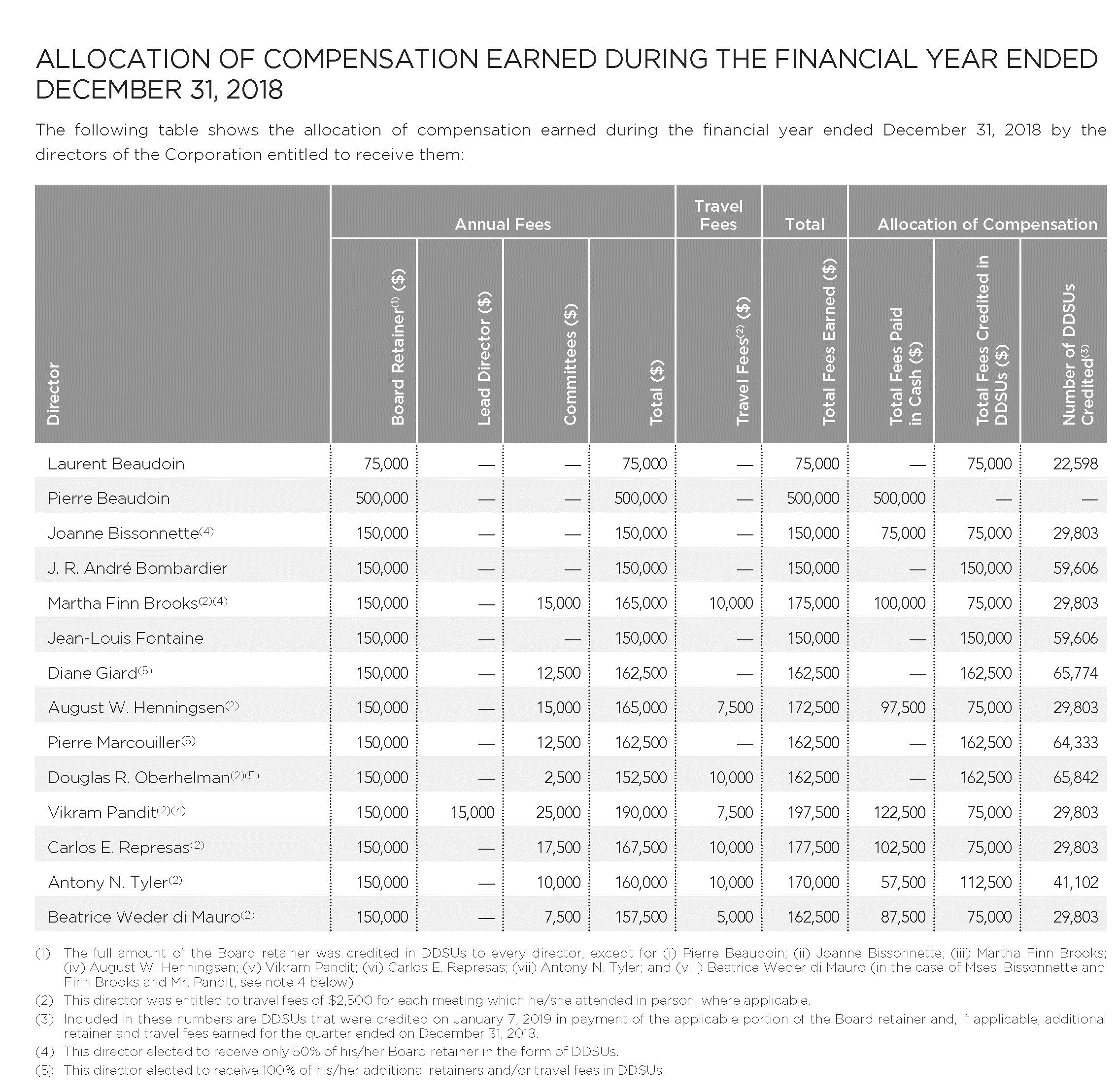

At issue this year is Bombardier paying former chief executive Alain Bellemare a severance package of US$12.35-million when he was terminated in March, as well as promised future special payments and potential severance packages to other top executives when a deal to sell the company’s train division closes in 2021.

This is purely political posturing to the public to justify holding Class B shares (2.1 billion outstanding) in the company. Bombardier’s Class A shares (309 million outstanding) have 10 votes each, which give its holders effective control of the company. Bombardier’s Class A shares are currently trading at about a 30% premium over the Class B shares, so the market does ascribe some value to the voting component.

There is little remedy for the subordinate shareholders other than to sell if they wish to voice their opinion. This happens in any dual-class share structure company, where typically the founders get the supervoting majority to stack the board. You have cases like Berkshire (NYSE: BRK.A) and Fairfax (TSX: FFH) where you are being a silent partner to Warren Buffett/Prem Watsa, but you also have cases like Dundee (TSX: DC.A), which have made disastrous capital allocation decisions in the past decade (will they get their act together for the next one? Insiders are at least buying now). There are also firms like Biglari Holdings (NYSE: BH), where the controlling shareholder basically has open contempt for its subordinate shareholders – don’t like me? Go ahead and sell! Zuckerberg at Facebook (Nasdaq: FB) also has expressed the same sentiment – my way or the highway.

In all of these cases, investors, especially institutional ones, should know what they have gotten into. This doesn’t mean they can’t complain, but when it comes to exercising power to compel the board of directors to tell management to change their practices, the influence is very weak since controlling shareholders will always be able to replace potentially dissenting directors with those that favour their interests. In the case of Bombardier, who wants to give up $150-$190k for being a human rubber stamp?

(By the way, this board is far too large).

The only way to get any sort of leverage on an entrenched board is to own enough of the debt in a distressed situation, and then you will be able to get enough attention of management by the time the maturity comes to extract better terms. But these situations are rare, and they more often end up with management engaging in asset stripping and other extraction activities to the detriment of both shareholders and debtholders alike before they finally lose control.

took a chance on the BBD pref shares based upon an earlier note you published (thank you). Since BBD seems to be a sacred cow in Canada figure the pref dividends are safe. Am now looking at Aimia pref shares – with take over of company by Mittleman brothers and complete change in direction of company thinking the pref shares here too could represent a good risk/reward . Interested in thoughts of others who follow this site. Happy Investing! (as Lou Schizas used to say )

Aimia is entirely about the future, given the effective takeover by Mittleman. The market is sufficiently scarred by past actions at Aimia that the prefs represent good risk/reward if Mittleman can avoid destroying shareholder equity. Decisive early action by the “new” company are positive IMO, including the willingness to use cash to buy securities in March and then sell them on the Robin Hood rally.

I expect common and preferred share buybacks via NCIBs and possibly SIBs to drive book value higher. Eventually, the market will demand less of a spread to the GOC 5 year for the prefs and prices will rise. In the meantime, yields are pretty good!

@Larry & @stusclues – I also picked up some BBD preferred recently around $8 and also picked up some Aimia preferred shares. I have previously owned Aimia preferred shares prior to them suspending the dividends – i was able to get out with a profit and a bit of deferred dividends after the Air Canada buyout of Aeroplan was announced. I feel they are sufficiently cheap with a good yield. The ‘A’ shares are locked in at the current rate for about 5 years.

The previous Aimia management was brutal but Mittleman seems to be making good decisions. I don’t think the risk is high here and I agree with stusclues that people are likely scarred by the mismanagement of the previous company leaders. Mittleman has sufficient skin in the game that they are not going to make overtly greedy or stupid moves.

thank you both for quick replies! I picked up some Aimia C shares and may add more with the A series to hedge the reset risk.

Larry – I don’t understand your comment about hedging the reset risk. The C’s reset in 2024 and the As in 2025. Are you that fine tuned in your modeling? It seems pretty clear to me that the As are much cheaper (more upside) at current market prices.

Liquidity on the issues are terrible, but at the last trading prices of $13.31 for AIM.PR.A and $16.7 for AIM.PR.C, AIM.PR.A, on both the basis of current yield and projected reset yield, is much cheaper.

thanks again and this is why I find this site very useful as I find it very hard to get much info on Cdn prefs. Noticed tonight that Air Canada court challenge against Aimia has been dismissed so another +ve step for Aimia.

Amazing what can be done with those super-voting A shares (“Look, they love us!”)… in all fairness, one has to wonder where the other 1.8 billion votes on the B-shares went:

The non-binding advisory resolution on the Corporation’s approach to executive compensation was approved by a majority of the votes cast by shareholders on a vote by electronic ballot. 94.52% of the proxies received and ballots cast on this matter, representing a total number of 3,108,057,165 votes, were voted FOR the approval and 5.48%, representing a total number of 180,028,121 votes, were voted AGAINST.

Did you read this article Sacha?

https://seekingalpha.com/article/4374077-whether-is-value-in-bombardier-preferred-shares?utm_medium=email&utm_source=seeking_alpha&mail_subject=this-is-one-of-the-greatest-secular-growth-trends&utm_campaign=nl-investing-ideas&utm_content=link-17

A shockingly well-written article on SA. This author’s analysis is good. I got rid of the last of my Cs in 2018, and I fully expect BBD to convert them to equity as part of reforming their capital structure. I also expect my March 2022 debt to mature or get called after the Alstom deal – now I’m just clipping coupons until that happens. If I could defer the capital gain on that until 2022, all the better.

As I recall that Canadian author made some badly timed calls in the past concerning dividend’s of some companies that would not be cut, only to have them cut a couple days later….he then disappeared for a while, and now writes a lot less.

I’m not a big fan of this piece. He is too cynical with respect to the Bombardier family and lacks thoughtfulness about the leaner-business-jet-focused Bombardier that will emerge post-Alstom. He also makes the common error of assuming that the Cs are dramatically overpriced in the market by failing to make the connection that conversion to commons, along with other balance sheet initiatives, will incrementally de-risk the commons, helping increase the price.