Diamond Offshore (NYSE: DO) today went to Chapter 11 heaven. Offshore drilling is even more expensive than drilling for oil by digging into your backyard, and paying somebody US$40/barrel for your crude oil isn’t a very economical business model.

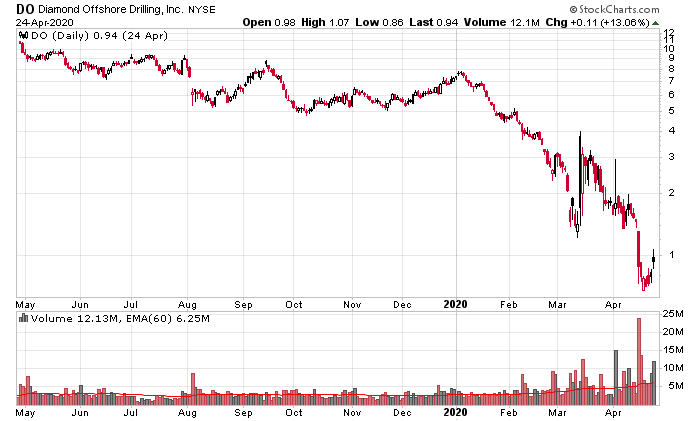

The demise in Diamond Offshore was generally projected by the stock market:

There was also a very explicit hint on April 16th, where they stated they were withholding interest payments on one of their senior notes – never a good sign!

Diamond Offshore Drilling, Inc. (the “Company”) elected not to make the semiannual interest payment due in respect of its 5.70% Senior Notes due 2039 (the “Notes”). Under the terms of the indenture governing the Notes, the interest payment was due on April 15, 2020, and the Company has a 30-day grace period to make the payment. Non-payment of the interest on the due date is not an event of default under the indenture governing the Notes but would become an event of default if the payment is not made within the 30-day grace period. During the grace period, the Company is not permitted to borrow additional amounts under the Credit Agreement (as defined below).

On December 31, 2019, the balance sheet had $2 billion in debt, entirely in four Senior notes and $5 billion in drilling assets. Subsequent to the 2019 year end, they drew some capital on a revolving credit facility before going to Chapter 11, but otherwise most of the debt is pari-passu, which means they will probably get a slab of equity in the restructured entity.

The senior debt has been very volatile in trading today, hovering around the 10 cent level. If I had deep enough pockets (it is nearly impossible and highly risky for retail players to get involved in outcomes of Chapter 11 proceedings) I’d consider buying a slab of the senior notes. They’ll probably wipe out 3/4 of the debt, give out a bunch of equity in compensation, extend the rest of the maturities out for five years, and then pray that there is a recovery in oil where everybody can be made whole.

Other related companies I keep an eye on: Transocean (NYSE: RIG), and Seadrill (NYSE: SDRL). Seadrill went through a recapitalization a couple years ago, and Transocean looks to be on the brink (although they are not in as bad a shape as Diamond was, they can probably find enough spare change in the couch to survive until around 2022).