A story of some collateral damage of the Coronavirus: A public example of a margin call – Royal Bank taking one of its clients to the cleaners.

The juicy details are here: 1257000-1257010-https-ecf-nysd-uscourts-gov-doc1-127126628149

3. Specifically, on March 23, 2020, Defendants issued margin calls to Plaintiffs on

the purported basis that the “Market Values” of Plaintiffs’ commercial mortgage-backed

securities (“CMBS”) that are financed through the parties’ Master Repurchase Agreements

(“MRAs”) have drastically declined in value as a result of the current market crisis. According

to Defendants, their calculations of these “Market Values” reveal a purported “Margin Deficit”

that permits them to require Plaintiffs to post large sums of additional cash or securities to meet

margin requirements. Defendants’ margin calls, however, are based on their entirely subjective

and self-serving calculation of “Market Value,” and do not come close to reflecting the

fundamental value of the securities or following the contractually-mandated means of assessing

those values. Indeed, because the “Market” is temporarily frozen, there currently is no objective

means of calculating “Market Value.” Moreover, the MRAs provide that “Market Value” shall

be based on a “price … obtained from a generally recognized source agreed to by the parties or

the most recent closing bid quotation from such a source.” MRA ¶ 2(j). It is entirely unclear

what “source” Defendants have been using to calculate “Market Value” in this illiquid market,

but it is crystal clear that Plaintiffs have not agreed to use it.…

5. Yesterday (Sacha’s note: this was filed March 25, 2020), Plaintiffs learned that Defendants intend to conduct an auction that

includes nearly $11 million of Plaintiffs’ CMBS—at 11:00 a.m., EDT, this morning.…

33. Notwithstanding the various government actions designed to return liquidity to

the markets and stave off mass foreclosures, on March 23, 2020, Defendants made multiple

margin calls on Plaintiffs in the total amount of $10,794,000.

Ouch. When playing with debt and leverage, playing with fire. Effectively, this mREIT got cleaned because they believed their definition of “Market Value” was what they believed they will get the assets for, while RBC’s definition appears to be “whatever you can auction the thing for”. Also I truly wonder what’s going to happen with all of this private equity and infrastructure investments going on that don’t have any active market – you can be sure that the level 3 value on balance sheets for the funds and such that own these assets are likely going to get downgraded pretty soon!

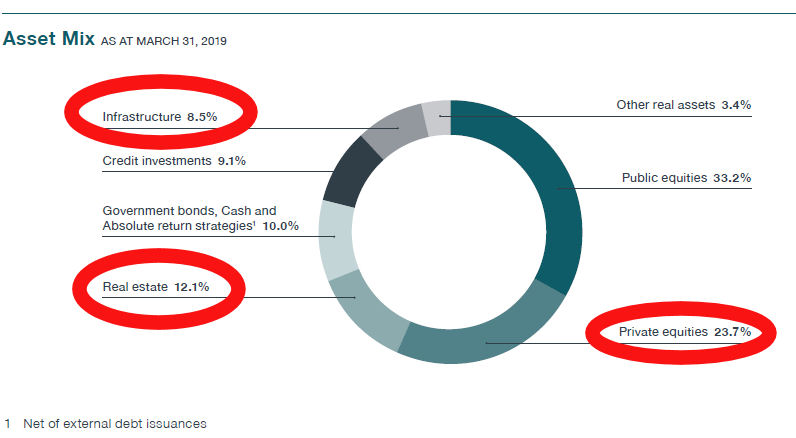

And for a final note, take a look at your Canada Pension Plan and ask yourself whether you can trust the stated value on 44% of the portfolio or so (I’m being generous and considering the “Other Real Assets” to be things like gold bars in a vault somewhere)…

When you have $400 billion in assets under management, you’re probably allowed to use your own definition of “Market Value” and not RBC’s.

Accounting-wise, I think the largest scandal-in-waiting is the proper valuation of private and infrastructure assets, or basically anything that doesn’t have an actively trading market. It would not shock me at all to discover there are plenty of assets out there being held on books of funds that are overstated by a significant magnitude.

This is a great post and a concern I’ve had for years. Several funds have had issues (https://www.advisor.ca/news/industry-news/canada-life-temporarily-suspends-real-estate-funds/).

I hold BAM.A. Any concerns on their accounting of long-lived assets?

BAM.A trades on its opaqueness. Flatt must be a genius, so he needs it to be this complex? It’s sort of like John Malone and his massively convoluted corporate structures – I never figured them out, and I’m happy to let others make or lose fortunes with them.

Or put another way, put a gun to my head and ask me to invest 100% in BAM.A or Berkshire, and it’s an easy Berkshire, which despite the size of the entity, is still reasonably simple to get an idea of what you’re investing in despite its half trillion capitalization.