Random observations:

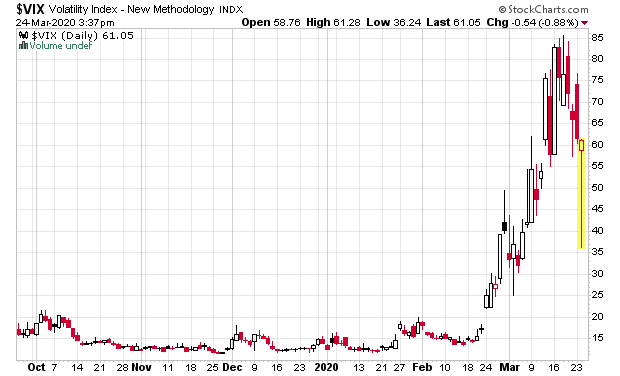

Barring any more catastrophic news (e.g. China launching a military invasion), Vix has likely peaked:

There might be another spike up but I’d suspect that this will subside over the coming months as the fallout is now being quantified and known.

I have done some radical portfolio re-alignment over the past couple weeks. I’ve not been thrilled about my performance, which I’d consider to be mediocre at best. The choice to diversify was correct. An acknowledgement of my own stupidity is in the form of index longs on the S&P 500, which is just trying to get a broad-brushed swash of what is going to be a gigantic capital influx because the “borrow at 1%, long at 10%” trade is going to turn that 10% into 8%, 6%, and 4% before we experience the next leveraged crash.

Speaking of what’s above 10% yield, have you looked at anything relating to the debt markets lately? Print up a list, get a dartboard, and throw darts at it, and you’re likely to do good.

Same thing goes for most of the preferred share market, although you have to wonder about the state of those 5-year resets. Still, even if you assume the 5-year GOC bond yield stabilizes at around 50bps, you can buy some reasonably safe income streams. The only problem is when the market rockets up, you’re not going to be able to benefit as much.

Q1 and Q2 results are going to be horribly impacted, and this is going to make the P/E and PEG metric useless as an investment tool going forward for the next 18 months.

There is still going to be a whole bunch of ups and downs at wild magnitude. Resist the urge to buy on a +8/10% up day like today, and resist the urge to sell when we inevitably get a -5% day and you should do well.

Envision what’s going to still sell a year out. Businesses that were looking shaky before this crisis are likely to go belly-up, and even in a recovery will not recover to the extent that others will.

The math of portfolio management is that if you take a bunch of positions at 5% (or any arbitrary number), some will gravitate up, and some will gravitate down. The ones gravitating up are ones that you happened to pick at a reasonable time (or hopefully the choices themselves were skillful) and thus they will have a larger weighting. Thus future changes in these larger weighted items will have a more disproportionate impact on the overall portfolio, while those that slide down will have less of an impact. It’s exactly how capitalization-weighted investing works with indicies – the strong get stronger, while the weak get less capital. And if you pick something that goes up by a factor of 10, you can still have 9 total wipeouts and break even.

Finally, there is going to be an element of luck and iron steel nerves to pick at the entrails of those that get totally crushed by this – cruise lines, airlines, oil production, and anything very retail-driven. If you pick equity survivors out of those (especially those that are regarded as already written off to go into CCAA/Chapter 11), you will receive huge multiples on your investment – but these come at extreme risk of a permanent loss of capital. Ultra-high risk, ultra-high reward.