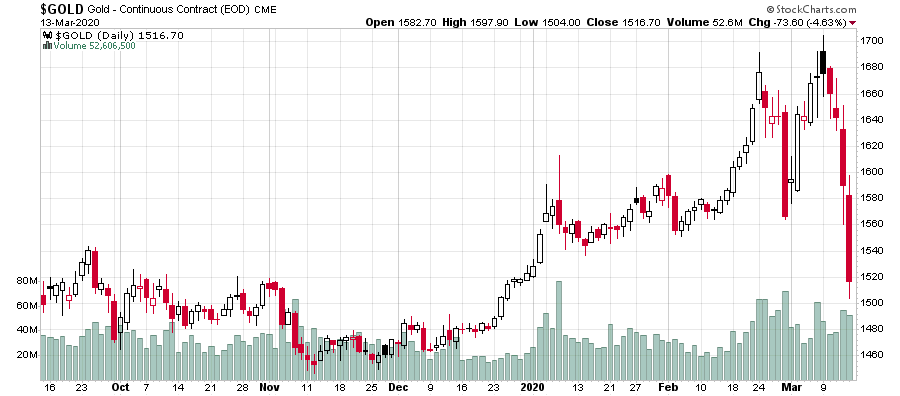

Nothing feels worse than holding an asset that goes down in price when the S&P 500 is up 9% in a day like last Friday:

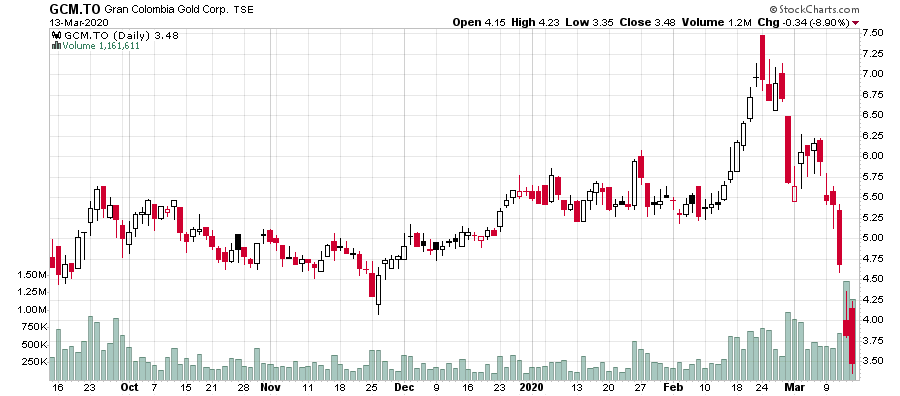

Fortunately I didn’t own anything gold-related (other than TSX: GCM.NT.U, which will be 30% called away at the end of March and the remainder stands a good chance of getting called away in April 2021).

Presumably gold assets (and this includes gold companies, which were equally slaughtered last Friday) were under supply pressure to raise cash to bid up other non-gold assets.

I generally do not like gold miners because historically they have been a huge money pit on capital expenditures on projects that have had collectively dubious return characteristics, but when looking at a company like Gran Colombia (TSX: GCM), they at least do have one viable operation (Segovia) that is making a ton of money at current gold prices. Yet the following:

Although they’ve made some sketchy capital allocation decisions, they did raise CAD$40 million at CAD$5.60/share (plus warrants) which Sprott and company is sitting about 35% underwater on now.

They announced in December 31, 2019 they had US$84 million. Adding the CAD$40 million they raised from the offering (minus 6% offering expenses), gives them US$111 million cash. They spent US$6 million on the January GCM.NT.U payment; US$15 million on the Caldas (Marmato) spin-off IPO/Reverse Takeover; and US$19 million in GCM.NT.U in March 31, for US$21 million. This leaves them US$73 million, plus I will assume US$20 million in Q1-2020 earnings (this will be announced around May 2020, but they did US$21 million at US$1,484/ounce).

US$93 million, offset by US$45 million in notes and US$14 million in (privately held) convertible debentures, gives US$34 million net cash. The market cap of CAD$211 million (60.8 million shares) is undiluted; there are 12 million warrants at CAD$2.21 exercise price; the CAD$20 million debentures are convertible at CAD$4.75; 7.14M warrants at CAD$6.50; and 3.26M warrants at CAD$5.40.

The $2.21 warrants will likely be exercised (not anytime soon; expiry is April 2024); thus US$53 million net cash on a market cap of CAD$253 million on an entity that has, roughly, a cash production capability of about US$80 million/year at a gold price of about US$1,490.

Gold closed at $1,516.70 last Friday.

Needless to say, this looks cheap, as long as the company doesn’t blow their earnings on dead-end mining projects (which would be my apprehension).

In general, monetary policy (zero-interest rate environment) would suggest that global currencies are going to mass devalue in order to stimulate economic prices; in theory, gold should do reasonably well in this environment, but not in the absolute throes of the crisis as people seek liquidity.

The following is a chart of gold during the 2008-2009 economic crisis. People liquidated gold, but after the liquidation was over, it did quite well as monetary policy kicked in:

I’m going to guess that gold will follow a similar trajectory this time around.