Company should be able to generate about $100 million in cash through operations in Q4, the thermal coal part of their market segment is steady, and coking coal markets look to be in-line.

CapEx will be elevated due to Leer South construction and thus share buybacks will be slowed down (to roughly $40-50 million/quarter, my estimate, compared to the $75 million they’ve been doing), but at that rate they still retire ~5% of the stock outstanding quarterly since each share they’re buying back at US$60 will result in roughly a 20-25% ROI given the estimated future cash returns they will earn.

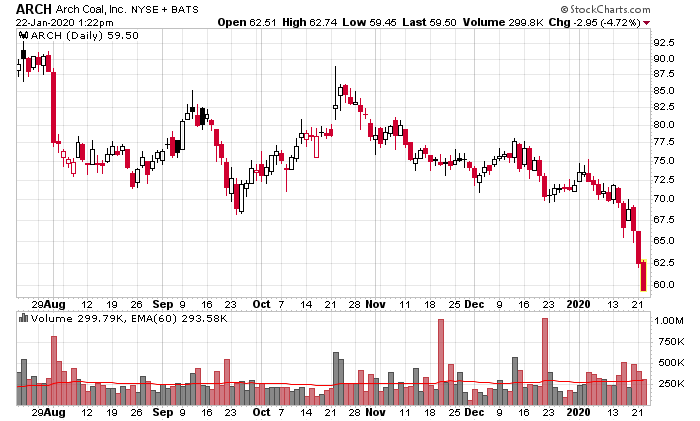

The panic is generated through two sources: ESG-forced policy investors forced to dump stock in coal companies; and fears that low natural gas pricing will displace coal power generation. The first is a social construct that simply serve to fuel incumbency protection. The second is more relevant, but power generation is a very slow-moving industry where long lead times and up-front capital costs means that existing coal plants will continue to be economically productive for years to come. This does not factor in coking coal, which is half of the company’s revenues, and has nothing to do with the war on thermal coal currently being waged.

In the meantime, the underlying company continues to generate cash. The company itself is in a net cash position.

As long as the cash is being generated, one of two outcomes will occur. If the stock price is at panic levels like it is currently, share repurchases will be massively accretive to EPS and will elevate the stock price when the supply dump is finished. The other option is the company can stockpile cash and issue a special dividend – with a lower share count, this leads to a significant cash outlay per share.

I have no idea how long this supply dump will be, but it isn’t often when you see companies trading at 3x historical PEs being mass dumped – of course, companies are valued on the basis of future earnings, but there’s quite a large margin of error to work with given that ARCH is far, far, far away from being insolvent!

Time to load up more.

There is a third option: the cash goes into the ground. Never underestimate the willingness of mining men to dig away whatever gains they make.

Anyway, I pretty much agree with this post, but your capital’s in the hands of price takers who haven’t necessarily covered themselves in glory with their allocation decisions (even the buybacks–driven, likely, by former debtholders who wanted an exit, and who maybe aren’t inclined to dig–were mostly done at prices much higher than today’s, so it’s still an open question whether this was the smartest use of $). That said, it’s so, so cheap, and I think the closing off of debt (and equity?) markets will in the midterm end up being the biggest boon the coal industry’s solvency has ever seen.

I guess I should clarify “As long as the cash is being generated” as being free cash… you are right about miners (especially gold ones!) loving their never-ending projects until the next bust.

“I think the closing off of debt (and equity?) markets will in the midterm end up being the biggest boon the coal industry’s solvency has ever seen.”

Bingo – incumbency protection. Leer South ($360-$390M estimate) appears to make sense (although one can argue buying back half the shares at these prices even more so and just keep operating Leer), and getting the thermal assets together with BTU for cost savings makes a lot of sense for the inevitable run-off of that business. Thermal will take a lot longer to die off than most expect.

“The first is a social construct that simply serve to fuel incumbency protection”

Can you elaborate on this a bit? Are you referring to the idea that certain actors have made massive bets on coal going away (renewables, gas, etc.) and now that those bets are in-play it is time to pull the rug on coal? Or to those political forces who draw their power from pushing for action on climate change?

Even more abstract. The theory is that by withdrawing access to capital to the deemed “bad actors” that are not ESG-compliant, they can be goaded into becoming ESG-compliant, or face the consequences of more expensive cost of capital. This is in addition to the perceived moral hazard of investing in such entities being removed (does not consider the moral hazard of investing in other entities with sub-par returns but I’ll leave that for later).

In the case of fossil fuel companies, clearly they will never be “E” compliant (using today’s definition which is all fossil fuels are bad), so they will always be deemed bad actors. Hence, the cost of capital will be higher for entrants, which increases incumbency protection.

The net result is somewhat paradoxical in that the bad actors in capital-constricted industries will have better returns if they can generate the required amounts of internal capital.

It breaks the back of those that require external capital (e.g. companies that have debt to rollover) but since that already happened with most of the coal industry in 2016, the survivors are all self-funded and likely in a profitable equilibrium state. The leaded gasoline additive market is a good analogy, but perhaps even better is tobacco post 1990s settlement. The missing variable is the global component of coal, but coke is not going away, and south/southeast Asia will be sucking up a gigantic amount of thermal for the foreseeable future.

None of this ESG stuff does anything to benefit or hinder the environment. It’s a disconnect from economics and social psychology that is actually becoming actionable.

Thanks for the idea. Wonder if you have an idea of the annual run-off / depletion rate of the existing thermal coal mines? Seems to me that as long as the annual decline % of global coal usage < existing mine depletion rate, these coal companies will not need to worry about their products being obsolete?

Stated alternatively, assuming current coal prices hold and the company never again invest in a new mine, can we expect the existing assets to be NPV positive using a high equity cost of capital?

Thanks again.

Page 25 on ARCH’s last 10-Q should give some hints as to the present day situation. The politics concerning export capacity is much more relevant on the thermal side, the west coast states are all solidly opposing any increase in facilitation of coal to the Pacific, which is being litigated in court in terms of whether states have jurisdiction to block (remind anybody of Trans-Mountain and British Columbia?).

First 9 months of 2019, the Powder River Basin produced $85M EBITDA, with $19M in capex, on an asset base of $236 million…

Red flag that the CEO at the time of bankruptcy is still leading the company?

He came in April 2012 and the company already had the $5 billion debt noose around its neck and I don’t think it mattered who was there, the company was bound for Chapter 11.

I was looking at theirs buybacks, here how many shares they repurchaed in 2019 :

Q1 2019 : 872,317 shares at $89.70 for $78,246,834

Q2 2019 : 697,255 shares at $90.92 for $63,394,424

Q3 2019 : 1,169,597 shares at $78.11 for $91,357,221

Q4 2019 : 133,379 shares at $78.72 for $10,499,594

Furthermore, they didn’t buy a single share in december 2019 even tho they still had $233 million left in their authorization.

So like you predicted buybacks really slowed…

Management said they’re going to cut buybacks in 2020 in favour of capital construction of Leer South, which given the numbers involved I think is a reasonable decision (far more than my initial estimate which had more cash coming in). Their new unstated policy appears to be to keep their net cash roughly neutral. (It’s about $288 million cash and $311 million debt right now).

If met coal starts to rise in prices again there will be a lot more FCF and the gravy train will continue. If not, once Leer South gets going, there should be more coming in 2022 regardless and at that point probably only maintenance capital.

BTU scrapped their dividend and buyback program to focus on debt reduction, and their balance sheet situation is a bit worse, in addition to their met coal operations being more troublesome.

I don’t normally like commodity companies, but there’s compelling value.