Rogers Sugar reported their fiscal year-end results yesterday. I wrote about them mostly recently in their last quarter. The erosion of the profitability of their maple division is continuing to hurt the company. The highlight is the following:

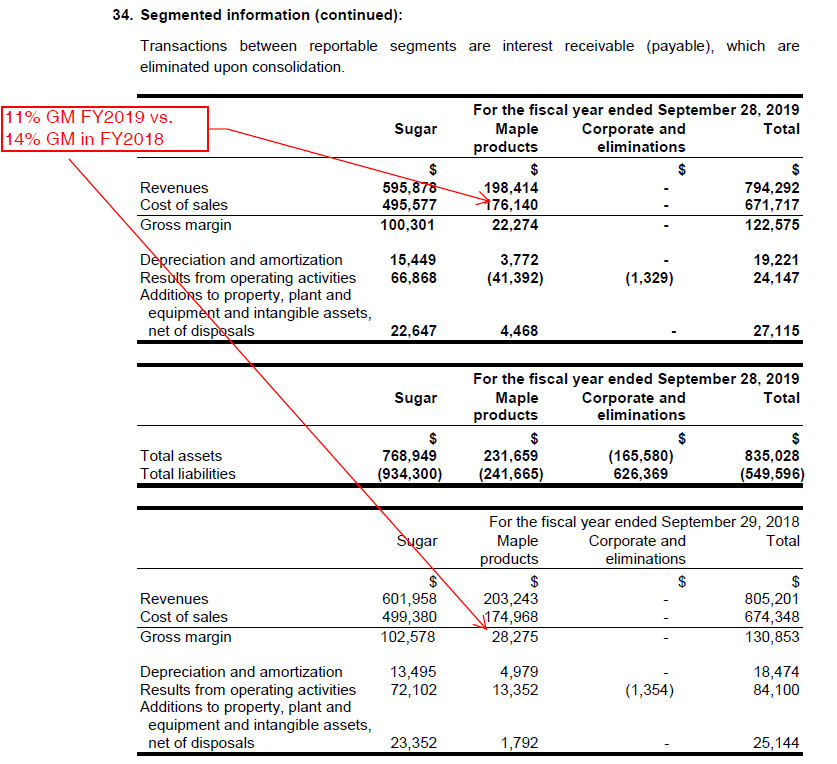

Rogers is able to make a 17% gross profit on sugar refining, and this has been stable (indeed, threat of substitutes is the primary competitive force). However, on the maple division, profitability has continued to decrease due to competition. This is continuing to hurt the company’s financial performance.

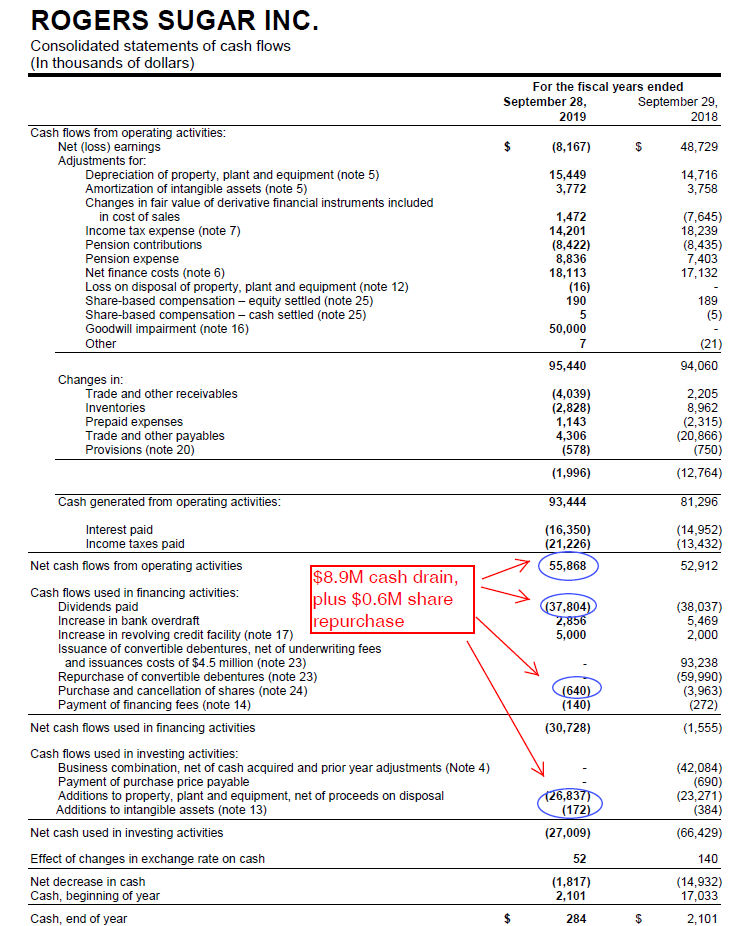

On the cash side, the company continues to distribute more capital in dividends than they are able to sustain with operating cash flows plus capital expenditures:

This is financed with debentures, and a bank line of credit and a revolving facility – which is increasing. The credit pressure will increase if this keeps up. They even spent a little bit buying back stock despite the cash situation, which they probably rationalize in their heads by a 6.9% yield rate (at the $5.22/share they purchased the stock with the 36 cent dividend), but without paying attention to the debt, these sorts of repurchases are going to be much more expensive for shareholders today!

We see the equity markets are starting to get concerned – Rogers is down about 5% today after the annual report. Rogers does have a couple convertible debenture series outstanding which are trading near par presently (with a 5% and 4.75% coupon, maturing in December 2024 and June 2025, respectively) which clearly shows they are not in dire straits by any means, but things are headed in the wrong direction.

The clear conclusion is that the diversification into maple is not turning out very well – the people selling the businesses probably knew more than Rogers did about the future outcome.

At $4.80/share I am still not interested in the equity, although I’m sure yield chasers will love the 7.5% yield.

If you’re patient, what’s your sense of the Maple business working out longer term? Diversification due to fear of substitutes makes a good story at least, and I know on the call they talked about losing and regaining a customer so something is working. However, I’m skeptical of the “we’re going to find new markets” plan.

Could you please explain where this 8.9M cash drain number is coming from?

I don’t really understand that moment.

Thank you!

55,868 cash from operating activities

minus:

26,837 in capital expenditures

172 intangible assets

37,804 in dividends

= 8,945 cash drain

Hidden assumption here is that Rogers needs to spend that much in capital expenditures a year to continue its operating cash flow, but either way as it stands right now they’re not making enough money to cover the current dividend.

Thanks a lot! 🙂

…