… I’m not talking about Ovintiv either (TSX: ECA), which is pretty much an admission that any dot-com name for a company has already been taken up, so companies now have to resort to pharmaceutical-style naming conventions for their firms.

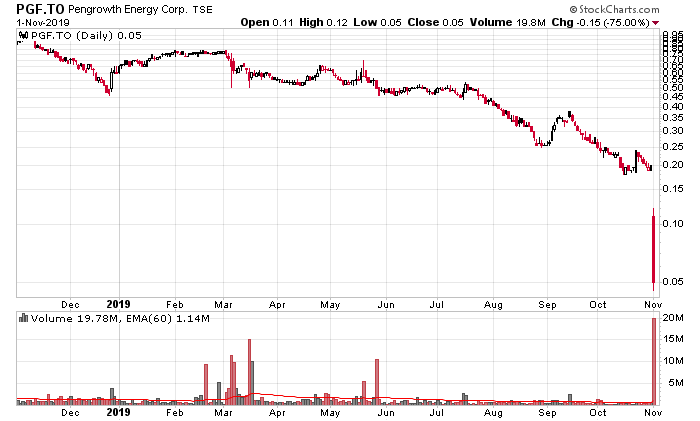

Pengrowth (TSX: PGF), which I have written about extensively in the past on this site, announced on Friday they were going to accept a takeover bid of CAD$0.05/share plus the payout of debt. The amount of debt outstanding was approximately $700 million and the total purchase price is $740 million.

The effect on their stock price was fairly dramatic:

It reminds me of the expression I tell people around me when they mention that something is cheap at 20 cents per share – “When it goes to zero, your loss is always the same – 100 percent”. In this case, investors took a 75% haircut on the last Friday of trading after the announcement.

This is the next (former) mid-tier oil and gas player to effectively go belly-up, the previous one being Bellatrix Exploration. At the rate things are going, only Suncor will be the last one standing in Canada.

The buyout of Pengrowth is going to be interesting for a couple reasons.

One is that the press release does not make mention in any way of any shareholder consent agreement from Seymour Schulich, who owns 28% of the company. Perhaps he is planning on taking a huge capital loss. One does not do big merger deals without getting consents from major shareholders with deep pockets, so the absence of this is very mysterious. To reverse the merger will cost some other suitor $45 million dollars – in light of the existing deal, this is a huge windfall that would be paid out if somebody were interested in the assets.

However, I deeply suspect in the shopping around process they couldn’t find anybody that was willing to finance the company at an acceptable price. The management information circular that will come out should yield some further clues on the process they undertook.

The other is how the deal is structured – Cona Resources used to be public, but it was majority owned by the Waterous Energy Fund, which is relatively secretive in its dealings (it is private). Waterous took its minority share of Cona private in May 2018 and we can infer from its SEDAR filings that were available that this entity is still not making money. Cona was bought out at about 45% of book value ($2.55/share on 101 million shares) coupled with $332 million in debt.

That said, Pengrowth, stripped of its leverage situation, actually makes money. Not a lot (especially in the current Canadian context), but while I am not surprised that shareholders are taking a massive bath on the company, I am surprised that this is the best agreement they could find. I am guessing the existing debt holders were completely unwilling to consider a debt-for-equity swap.

If Canadian oil and gas does come back from the dead, however, Pengrowth’s thermal oil assets are top notch and Waterous will be making a mint on this one. They effectively are going to wait this one out until the climate gets better. Parking $740 million of capital to do this seems like a reasonable gamble. I can see why they made it.

My last position in Pengrowth was in their unsecured convertible debentures, which matured at par in early 2017. I’ve been tracking it ever since and have taken no positions in their stock.