Chris posted a comment with the following question:

Do you have any thoughts on Canadian Pref shares? I’m watching a few for potential multi-year hold.

I asked for his thoughts first, and he replied:

I’m seeing a few yielding around 7% (taxed as dividend), with resets 3 to 4 years out. I can’t predict where they 5 year bond will be at that time, nor can I pick the bottom on these moves, but 7% for a few years followed by a reset at 5 year bond + 2.9% (based on $25, as you know) seems like a decent place to put some longer term money to work. BAM.PF.A is an example. Prefs are a bit outside my wheelhouse, but it seems that they present an opportunity every now and then. Thanks for any insight.

…

I forgot to mention that Brookfield has been buying back some of their prefs in the open market recently.

Chris – One thought is fairly obvious and you touched upon – those 5 year rate resets are awfully sensitive to the bond yield!

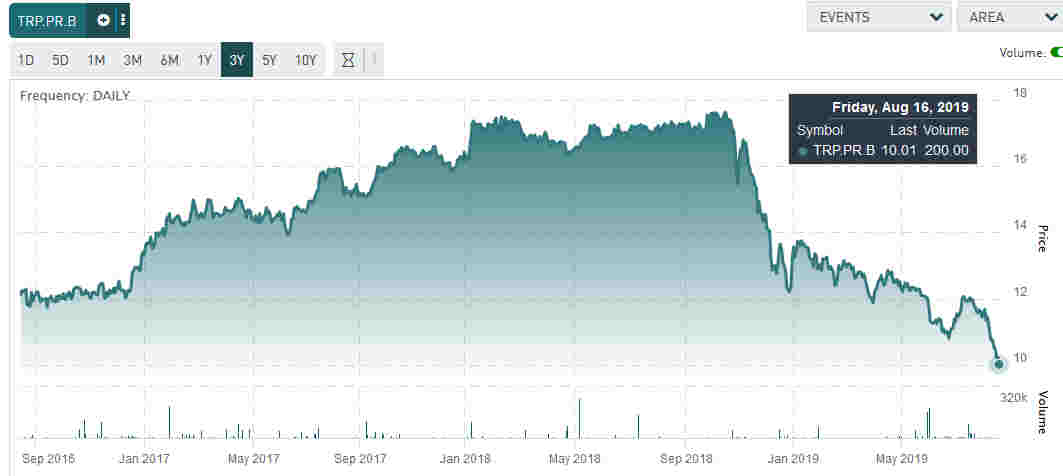

Example (above): TRP.PR.B (current coupon 2.152%, resets at 1.28% above 5yr, the reset is June 2020) – an investor since October 2018 will have lost 45% of their capital to date (when the 5yr yield was roughly 240bps)! That’s very heavy, and a double-whammy because the equity from October 2018 to present has gone up! Normally you’d expect capital gains/losses for preferred shares to be muted to the equity. The company itself hasn’t materially changed in credit profile.

Currently the 5yr government yield is 121bps – at present rates you’ll get a reset at 6.2%, but you can be sure if 5yr yields go down to 60bps (which is conceivable and mirrors the lows a few years back) TRP.PR.B will be trading at around $7.60-ish, all things being equal, or almost another 25% of capital loss!

There also appears to be a law of dividing by small numbers effect going on. Let me illustrate with an example – pretend something yields 3% at present. Going from 3.0% to 2.5% is a 17% difference. Going from 2.5% to 2.0% is an 20% difference. Going from 2.0% to 1.5% is a 25% difference – low-rate reset preferred shares such as TRP.PR.B are getting absolutely killed because of the small denominator.

So if you want to take your 6-7% coupons and run with them, you need to take into consideration that there’s a good chance that you won’t be able to unlock the capital without taking losses, and ultimately you want to eventually see a day where interest rates are higher than when you initially purchased the preferred securities – who knows if/when this will be?

Hence, those 5 year rate resets are much more risky than people probably thought – they have been wildly volatile in the past five years.

You can dampen the risk by buying rate resets that are further out in time (e.g. resetting 3, 4 years from now) but they still trade quite sensitively to the overall 5yr government bond rate. Fixed rate (straight) preferreds are another option (albeit with different rate sensitivity). Most minimum-rate guaranteed preferreds trade very expensive (e.g. PPL.PR.K).

Of course if you anticipate 5yr government rates will increase, the inverse of the above scenario applies (i.e. potential for significant capital gains).

With the US Fed anticipated to drop short term rates, there’s a good chance Canada will be following to some extent and this will continue to depress the entire yield curve. I’m not offering an opinion on future rates, but the trend clearly has been negative (i.e. bias towards lowering rates) since the beginning of the year.

Another comment I will make is that I’ve generally noticed equity presents a much more attractive risk/reward than the preferred shares in a lot of issuers. If you’re just buying for income, why not just buy equities that give out nearly the same yield with a lot more potential for upside (including dividend increases)?

Also, I have not seen another asset class that is so ripe for tax-loss selling. If you were sitting on a 45% loss on TRP.PR.B but really wanted the exposure, I’d sell it and buy something very related instead (e.g. TRP.PR.C) and this avoids the 30-day wash sale rule.

So to conclude, there appears to be quite an element of risk unless if you’re planning on holding these securities strictly for income for a considerable period of time.

“So to conclude, there appears to be quite an element of risk unless if you’re planning on holding these securities strictly for income for a considerable period of time.”

This, of course, is the rub. It was also the essence of Chris’ question (i.e. he is planning a multi-year hold).

While your analysis is very good (as usual), it is primarily germane to those running money for others, especially those who are paid in relation to net (mark-to-market) asset value (i.e. virtually the entire investment management world), or to those with a need to spend from capital rather than income. For the lucky minority (Chris?) who can arrange their affairs to spend from investment income (i.e. they meet the IFRS test of “willingness and ability to hold” for the long term), these preferred share yields might be gift.

So, as usual, the answer “depends” on the goals of the investor. Warren Buffet’s parable of the noisy neighbor ought to be googled at this point.

There is no question that rate reset preferreds have been very volatile, but what if that volatility had more to do with the kind of people who invest in them and almost nothing to do with the economic characteristics of the preferreds themselves? I contend that if investors in these preferreds were rational they would trade with very little volatility because the spreads over 5-year bond yields should not change much over time. Instead the spreads widen dramatically whenever bond yields drop. Also, when the prefs trade at large discounts they carry the potential for big capital gains without risk of being called by the issuer. So in my view, the volatility is an absolute gift.

Thanks for the post and replies. I agree completely that individual rate-reset prefs are likely a poor investment choice for the short term as that would be too speculative. It’s my understanding that the pref market is mostly made up of retail investors , is extremely illiquid and therefore prone to substantial inefficiency. With the media currently fixated on yield curve inversion and negative interest rates, retail investors seem to want nothing to do with these shares. This appears to be a case where selling begets selling.

In my case, I plan to use funds that I do not need to access for a very long time, in a taxable account. So, I can provide liquidity to desperate sellers, and sell when the appetite for these shares returns, whether that’s one, five, or fifteen years from now. I’m also willing to add if we see further declines. As Sacha alluded to, you do not want to be one of those forced to sell at an inopportune time, with little liquidity, or it could get ugly.

Thanks again for the analysis and replies.

Sacha, I should mention that I agree with your point about buying the equity rather than the prefs, in most cases. Without such a sharp selloff in the rate-rest prefs, that is exactly what I would do. Only time will tell which performs better over the next few years, but the spread has widened so much that it piqued my interest, just as a sharp selloff in equities would push me in their direction.

Thanks for this post. I wonder what would happen if the Canada 5-year govt bond yield falls below 0%. Taking the example of TRP.PR.B that resets at 1.28% above 5-year, does it mean that the dividend rate will reset to less than 1.28%? Say if 5-yr canada is -0.50%, the pref rate becomes 0.78%?!

I suppose if 5-yr canada is lower than -1.28%, TRP won’t start drawing cash from my brokerage account every 3 months?! 🙂

@gokou3, pls see following links from prefblog on negative rates & p/s implications. James Hymas provides a wealth of information

http://prefblog.com/?p=39215

http://prefblog.com/?p=30401

http://prefblog.com/?p=27583#comment-193132

This is a great thread.

It will be interesting to see what the terms of future prefs will be, if these rate resets scare away investors. As Sacha mentioned KML. prefs have a floor of 5.2 and 5.25%. I wonder if we will see more of these, or even floating resets, which seem to be more popular in the US.

Some thoughts on reading the above (and concur with @Marc, this is an excellent conversation):

1. A “long time” is indeed that. Circumstances that get one in, however, may change before the envisioned ‘long time’ happens.

2. The last time the preferred shares dumped like this (late 2015/early 2016), they were trading at double-digit yields in a lot of instances (e.g. I do own some CF.PR.x that were bought at double-digit yields). I posted about Bombardier preferred shares (although that was also a combination of credit risk which got the yields so ridiculously high as well). I will observe that most of these higher quality prefs that have been dumped are still sitting around 6-7%, a far cry from what happened last time (if memory serves they were upper single digits).

3. I believe a lot of the initial purchasing is from Canadian institutional sources (they are typically the ones to subscribe to new offerings). I’m not sure how much of the volume is generated by retail vs. institutional, but at the minimum I’d think ETFs such as ZPR and CPD would contribute.

4. TRP.PR.B I believe is the lowest reset margin preferred share to illustrate an extreme, but indeed, it would be rather interesting to see what would happen if it reset with GOC at -1.3%… pay me to take those shares away from you! But indeed, if government bond rates were negative, that coupon gets really, really tiny – at GOC of -50bps (reset yield at 78bps), the pref price would be $3.25 to yield 6%. How much capital loss are you willing to take for the income?

Indeed, the income isn’t even that secure – your next reset may result in an income drop. Hence the wild price variations on these preferred shares, especially in relation to how the equity trades.

As an example: If you were forced to hold onto a stock or its preferred share for 10 years, would you buy BCE equity (yield: 5.1%, typically the div rate rises 5% annually) or something like BCE.PR.A which will give you a 6.1% yield until the next reset…

It’s clear the strong variable with the rate reset preferred shares are projected interest rates.

What should Prem Watsa do?

Fairfax long term debt is transacting to yield 3% +/-, while the reset yields on its various fixed rate prefs vary from 6.6% (C) to 7.0% (I). Interest on debt is deductable for Fairfax, dividends on prefs are after tax. Retiring preferred shares extinguishes their claim on income of the Corporation, freeing up cash for other purposes. At current prices, all of Fairfax preferred shares can be repurchased far below par (~50% for E for example at $12.45 as I write).

Why wouldn’t Prem borrow long to do a SIB on all or most of the preferred series to eliminate their claims on after tax income (thus increasing cash flow available for other purposes) and drive up book value of common shares? His oft stated primary goals for FFH are to do exactly both of these things.

If Prem, why not others? Say BAM (see SIB announced yesterday).

If the market spreads (indicating irrational panic in my view) of preferred shares to GOC yields don’t begin to narrow soon, I suggest we are going to see a lack of new issuance and major NCIB and SIB programs across the board. This ought to (eventually) help blunt the fall in prices and narrow spreads.

Does buying up the prefers below par result in a taxable gain for the corporation? If so, you setup yourself for a rather large tax payment that has to be pay upfront while the net cost reduction will be realized over a much longer period.

Atlantic Power is certainly buying back preferred shares. In fact that is a part of the appeal in owning their preferreds (assuming someone is going to force these preferreds to eventually get taken out a par).

I think the corporate buyback angle is the clincher… You can make all kinds of arguments that people won’t buy these preferreds because of volatility or some other fear, rational or not. But it’s hard to argue with the math of corporations buying back their own prefs at huge discounts. Dundee announced an intention to make a NCIB just last week, so add them to Brookfield and Atlantic Power.

Great responses.

It seems clear that perception of future rates (and not as distant as perhaps investors should look) really drives these reset prefs. If you compare 2015 & 2016 5 year Canada bond yields with HPR or ZPR, there’s sure a lot of spread movement, so there are many forces at work. Although 5 year yields can certainly move lower, I think there’s a lot of pessimism built into the reset prefs at the prices, as though much lower yields are a given. Add in the lack of liquidity and we’ve had a sharp correction.

I also like the buybacks, not just because they create real buying, but it’s good to see skilled capital allocators agree that these are trading too low.

I picked up 10 symbols from 8 issuers today, most resetting in 2-5 years at 224bps to 398bps above the 5 year. I’ll purchase a bit more if we see further declines. I’m prepared for a bit of a ride, but expect to be satisfied in a few years.

As stusclues mentioned, this is definitely a situation where suitability matters.

@Will: “Does buying up the prefers below par result in a taxable gain for the corporation?” – the question is rather does buying up the preferreds result in a deemed dividend? If it is done by open market purchases, then no. If it is done by a SIB, then potentially yes. But the burden would be borne by the sellers, not the purchasers.

@stusclues: As for what capital allocators should be doing, clearly if they can raise tax-deductible debt at 3-4% (pre-tax) and use them to redeem preferred shares at 6.5% after-tax, that’s presumably be a good use of money, providing that when it comes time to pay off the debt, you can roll it over on acceptable terms!

I’ll note BAM announced an NCIB and not SIB. Their daily purchase amounts are in most series limited to 1,000 shares so it isn’t a gigantic amount but every bit helps!

@Philbert: ATP can buy back some more AZP.PR.B but the other series were capped at 10% and this was done earlier this year. Even if they get bought out there is no obligation for the purchaser to take out the preferreds at par, but you could bet the spreads would tighten 100bps or so if purchased by a credible entity.

@Rod: Dundee is a trigger word for me. And they announced something much weaker than you stated, “we are taking steps to consider the implementation of a normal course issuer bid and possibly a substantial issuer bid for our Preference Shares, series 2 and series 3” – such a strong stand by management!

Yes, the Dundee news release was very weaselly. But I listened to the conference call and they stated they will go ahead with the NCIB. There was no hedging in the language on the call.

I have both the series 2 and 3. They’ve gained a lot in the last year, but I’m going to hold for a while at least. There are a lot of other prefs that are just as cheap now, so I may swap them for something else. I also own BPO.PR.N–a Brookfield Office Properties Pref (5yr+3%), which trades under $14. BPO is interesting because it is a wholly owned corporation of Brookfield Property Partners. It holds all their major office properties. Presumably it pays dividends out to BPY so they would have a hard time turning off the divs on the prefs if they have to cancel the dividends to BPY as well.

Thanks Sacha. I worded it poorly but I was actually referring to Atlantic Power eventually taking out their own preferreds at par. It would seem like once they get their financial house in order there might be some value in doing so. They can whittle away at them as they trade at a discount and then when you and I are the last shareholders redeem rest at par :).

@Philbert: I doubt they would do it unless if their prefs were already trading very close to par, and if that was the case you’d be sure their equity would be higher than US$2.35/share. Their recent purchase of the equity stake of the two plants from Altagas give out 20%+ on EBITDA (at least until the PPA expires in 2027) and if they can keep doing that, they’ll be investing in that instead of buying back anything.

@Rod: Reading the transcript on Dundee, it looks like they can’t do a SIB because they probably don’t know what their paid-up capital (tax basis value) is! So it’ll probably be an NCIB.

Thought I’d weigh in here as someone who recently bought a couple of preferreds (BAM.PR.S and TA.PR.J, in case anyone is interested).

My thought process was essentially two-fold:

1. I’m buying preferreds that I feel offer great yields when accounting for the credit worthiness of the issuer.

2. If rates go down I’m protected by the fact my 7.5% average yield on the two securities I bought should be more valuable, not less valuable. In other words, I don’t believe the yield on a preferred share should be the same if the five-year GoC bond is 1.5% or 0.5%.

I figure this is a classic heads I win tails I don’t lose much scenario. Sacha is right that these prefs will continue selling off if rates keep going down, but I can afford to patiently hold until we normalize again.

@Nelson: “2. If rates go down I’m protected by the fact my 7.5% average yield on the two securities I bought should be more valuable, not less valuable. In other words, I don’t believe the yield on a preferred share should be the same if the five-year GoC bond is 1.5% or 0.5%.”

Are you sure about this assumption? Yes, you have a temporary “yield shield” for the length of the pref before the next reset, but the market does bake in the current 5yr rate in some manner no matter if the pref is months away from the next rate reset or 4.5 years away.

FWIW, this week and last, I sold several of the prefs that I purchased in August. Nice 15-20% bounce, but far less compelling to hold now as 1.7% looks like the top for the 5 year for some time. I’m still holding a few, and purchased a couple that should hold up better if rates continue their pullback.