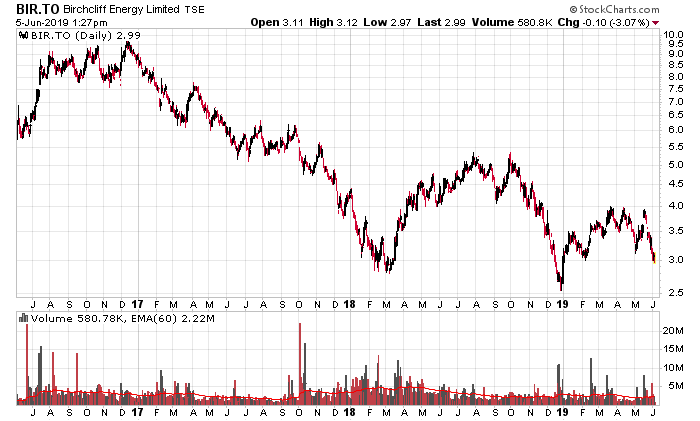

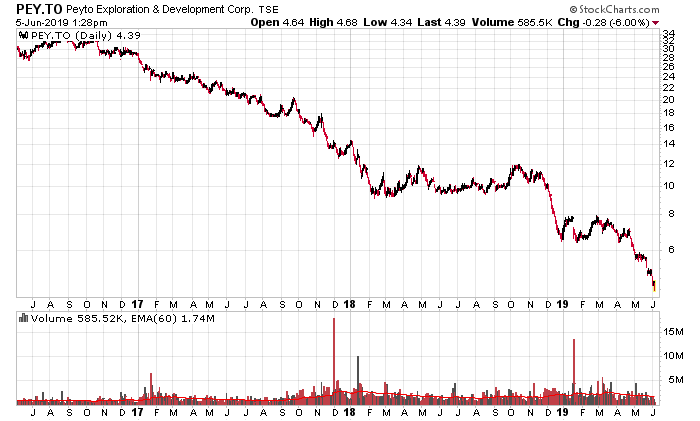

Birchcliff Energy (TSX: BIR) and Peyto (TSX: PEY) are two producers that have been able to be consistently profitable (or nearly so) despite horrible economics – in the case of Birchcliff, they have been able to do some degree of vertical integration, and in Peyto’s case, they operate organizationally very lean.

Investors that bought at the relative peaks of 2016 are sitting on losses of 70% and 85%, respectively.

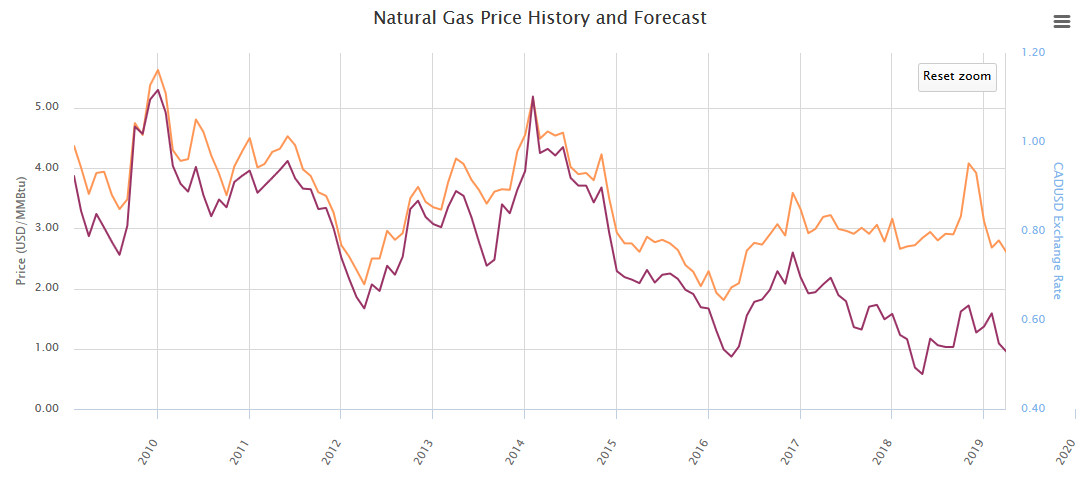

These are the charts of despair that I like looking at, but when looking at natural gas economics, it is simply a story of a huge supply glut. The primary driver is AECO pricing:

(Charts courtesy of GLJ Petroleum Consultants)

AECO at USD$1 vs. Henry Hub at USD$2.75 is a gigantic difference. There’s no point to mining natural gas at USD$1/MMBtu rates – only companies that can get rid of the supply at “proper” rates will have any chance in that pricing environment.

Even worse yet is that you can sell the same commodity to Japan in LNG form for about US$11/MMBtu at present. Although construction on LNG Canada is progressing, it remains to be seen whether regulatory roadblocks will put a halt to the project in some shape or form.