The carnage in the small-to-mid cap Canadian oil and gas sector continues.

Today’s interesting news is the recapitalization proposal of Bellatrix Exploration (TSX: BXE).

In this process, I’ll walk through the financial statements and this will give you a snapshot of how I go through these things. Indeed, this is not exhaustive, but a small part of the thought process.

Readers with exceptionally good long-term memory will know that I had an investment in their debt a very long time ago. Indeed, you can read about a minor exit trading error I made on the investment.

I haven’t touched Bellatrix since (9 years ago!), but still keep track of things. You never know when future opportunity may strike.

Bellatrix, just like most smaller Canadian oil and gas companies, has been really struggling.

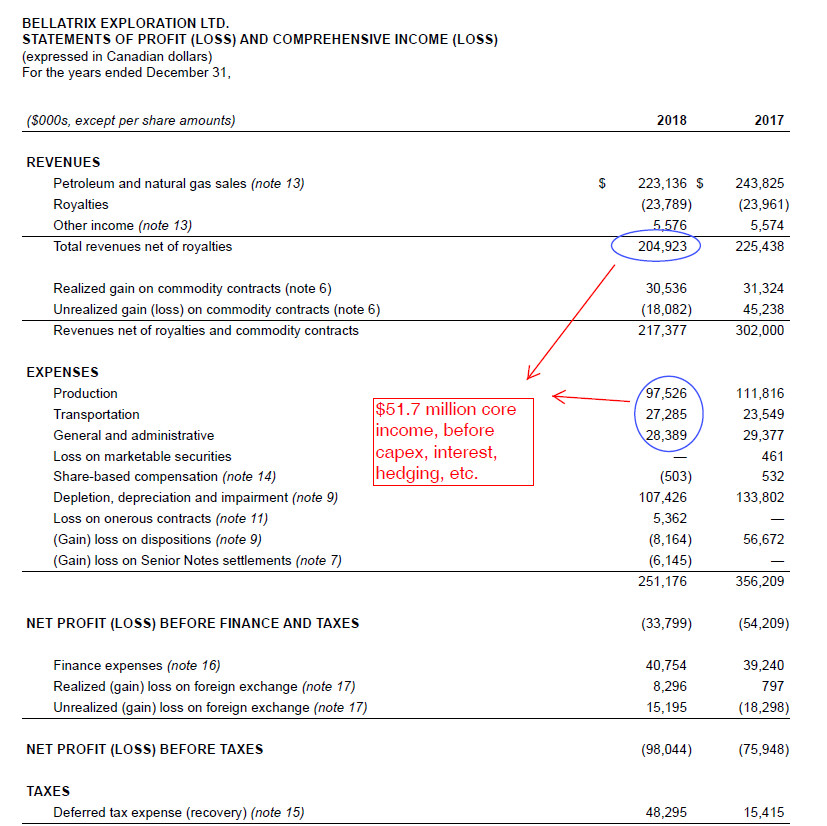

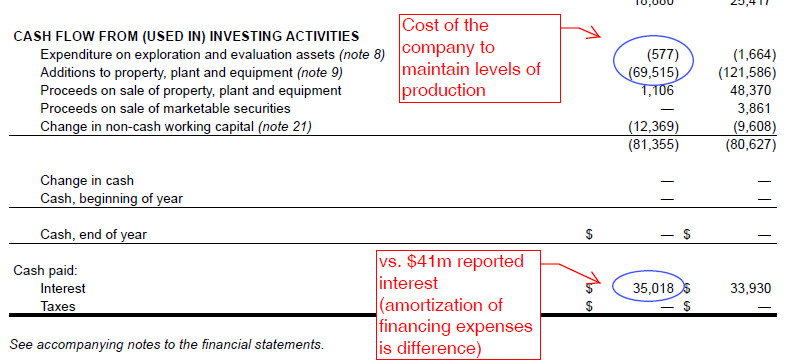

From the cash flow statement:

The key 2018 figures include CAD$52 million in EBITDA (not including impact of hedging), but the “I” is $41 million (cash cost is $35) and the “DA” is about $70 million of capital expenditures. People that are untrained at reading financial statements of oil and gas companies will be swayed by the syren’s voice of operating cash flows without due regard in consideration to how much capital expenditure it actually takes to sustain those barrels of oil (equivalent) per day.

In other words, the entity bled about $54 million cash in 2018. Without a change in oil price, the company is going nowhere financially.

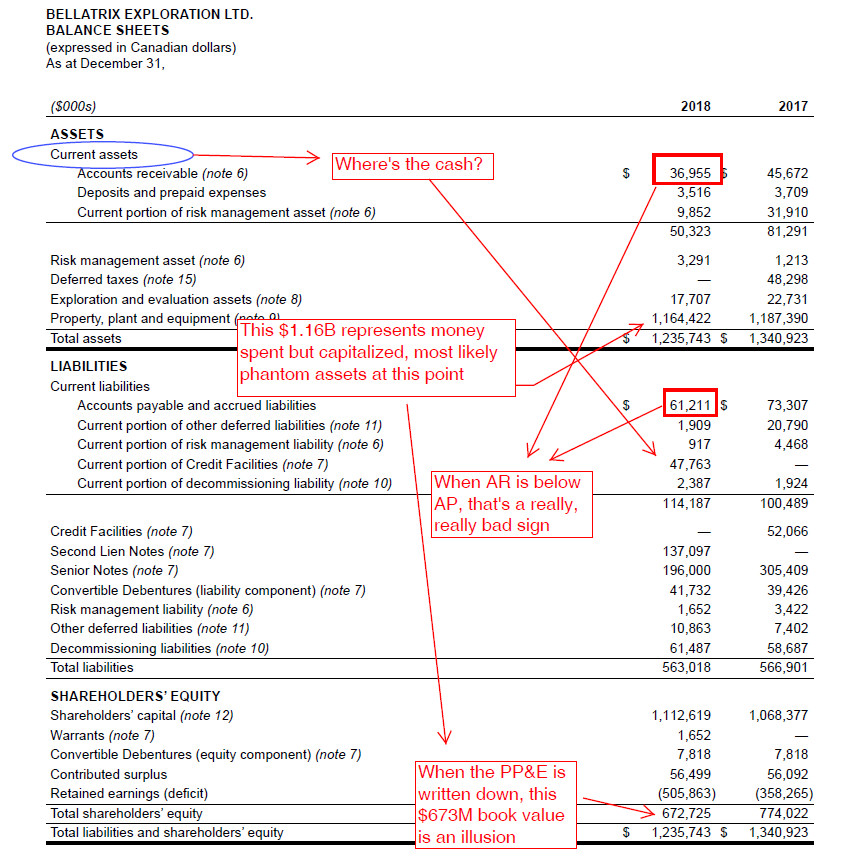

On the balance sheet, we note that the company has no cash on hand (cash is provided by a credit facility) and is capitalized by debt financing. This next picture is a gong-show illustration, so forgive me:

This is a company that is in very bad shape on its balance sheet. People that look strictly at financial metrics will see a $672 million book value (shareholder’s equity) and they will say “Hey! That’s over $8/share in value, and with the stock trading at 50 cents that’s a bargain!” but in economic reality, most of that equity value consists of already spent money that takes place in the form of Property, Plant and Equipment – exploration expenses that are capitalized and not expensed. Whether these assets have any recovery value or not depends on economic assumptions of the price of fossil fuels.

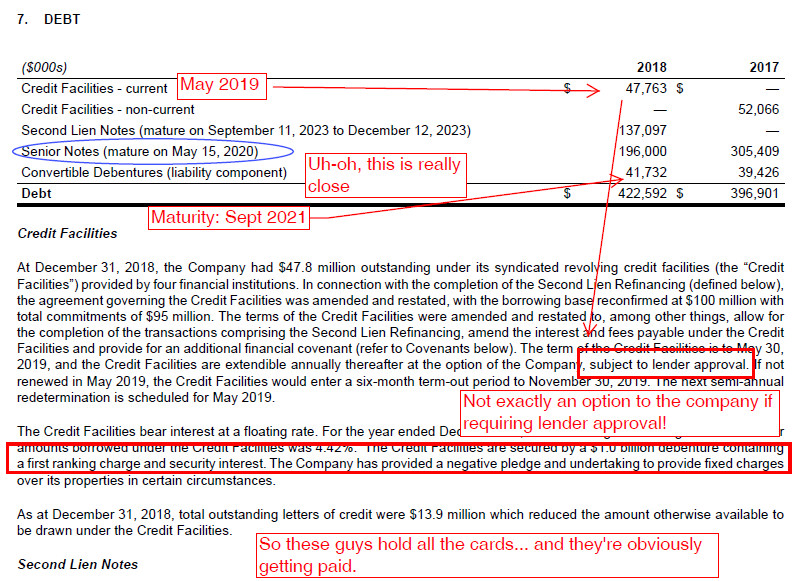

The company also has germane issues with its solvency – so we have to dig into the credit facility and debt financing:

We discover the company can borrow up to CAD$95 million and that this facility is first in line, and is up for redetermination at the end of May. This is not a good sign.

The next in line to maturity are the senior notes (which are third ranking, US$145.8 million par outstanding) and this matures in May 15, 2020 (not that far away). The first and second in line creditors will not allow a third-line creditor to jump them in maturity, so this has the makings of a classic credit crunch, which has to be solved. One scenario is that the credit facility provider will choose to extend the timeline another six months to facilitate a recapitalization, but in no way would they ever allow the senior notes to be repaid without huge assurances they would be paid first. Note the second-line noteholders do not have the ability to directly compel BXE to not pay the Senior Notes, but there are covenant issues regarding the loaning of money that is adverse to the interests of the second-line noteholders.

There are other issues regarding covenants which I will ignore for the purposes of this analysis (this adds a layer of complexity which in itself is interesting but I don’t wish to get into this post).

Now we get to the meat of the recapitalization proposal:

* an exchange of all of the Company’s outstanding 8.5% senior unsecured notes due 2020 (the “Senior Unsecured Notes”) for, in the aggregate and taking into account early consent consideration, a combination of US$50 million of new second lien notes due September 2023 (the “New Second Lien Notes”), US$50 million of new third lien notes due December 2023 (the “New Third Lien Notes”) and approximately 51% of the common shares of Bellatrix outstanding immediately following the implementation of the Recapitalization Transaction; and

* an exchange of all of the Company’s outstanding 6.75% convertible debentures due 2021 (the “Convertible Debentures”) for, in the aggregate and taking into account early consent consideration, approximately 32.5% of the common shares of Bellatrix outstanding immediately following the implementation of the Recapitalization Transaction.

…

* it is a condition to completion of the Recapitalization Transaction that the Company’s existing senior bank credit facility (the “Credit Facility”) (which currently matures on November 30, 2019) be extended for a one-year term on terms substantially similar to those currently in place;

The summary is that the company is asking their US$145.8 million senior noteholders to take a US$45.8 million haircut in exchange for 51% of the equity in Bellatrix, and also to become pari-passu (equal standing) to the second-ranking noteholders for US$50 million and effectively extend their own notes for another 3.5 years. The convertible debentures (CAD$50 million par, who are last in line on the pecking order) will receive 32.5% of the equity in Bellatrix.

Existing shareholders will keep 16.5% of the company, in exchange for offloading CAD$50 million plus US$45.8 million in debt, but the company will also receive a term extension on the primary part of its debt until 2023 (when everything becomes due).

The company obtained consent of 90% of the senior note holders (so passage becomes inevitable), but the question then becomes – what if the convertible debenture holders do not agree to this? They received consent from somebody owning 50% of the debentures, but with regards to the other 50%, they cannot be “force consented” unless if a sufficient number of them vote in a class to recapitalize (I am not sure what the threshold amount is).

The debenture holders, if they do not agree, can be told by the company that they will go into CCAA to force the matter (where they will receive nothing in return, instead of the 32.5% equity they are being offered today).

Hence it is interesting that the convertibles are trading up about 10 cents on the dollar today to 60 cents – valuing the remaining equity (plus the encumberance of the second-lien debt and credit facility) at CAD$92 million.

By no means does this recapitalization put Bellatrix on a good financial standing – certainly offloading CAD$111 million in debt will be good for the company, but the underlying operations still need an assist on the price of oil. If this recapitalization does go through, there are still considerable headwinds to be faced.