Pengrowth Energy (TSX: PGF) is an entity I have been following for a very long time. I used to own their debentures, which matured at par a few years ago. Today, their financial situation is much more dire and from their annual report (released today), we glean the following:

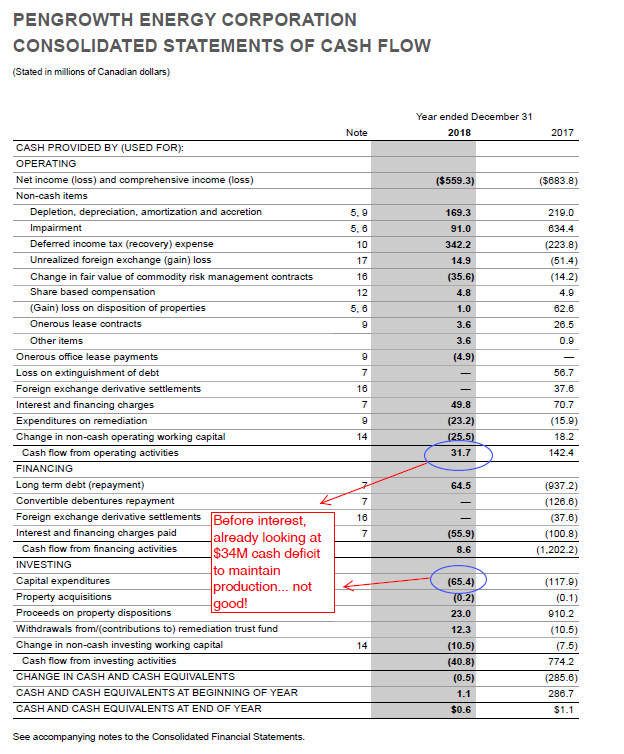

Suffering from low prices and high capital costs, the company is still bleeding money. In addition, when looking at their balance sheet:

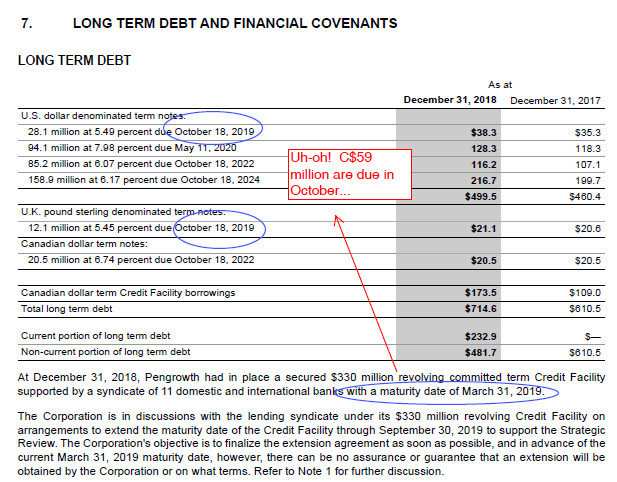

This is not a happy situation. Although management is “positive” they can strike a new credit agreement by the end of this month (when their secured credit facility becomes due), every bank in this syndicate will see CAD$59 million going out the window in October and another CAD$128 million going out eight months later. Considering the banks are the senior secured creditors in this arrangement, I very much doubt they will be willing to extend credit to the point where the October 2019 noteholders will be paid.

There is also the issue of the covenant, where the interest coverage ratio for Q4-2019 has to be better than 4.0, while presently (for the 2018 calendar year) such ratio was 1.6 – barring a huge increase in oil prices in the remainder of this calendar year, PGF stands no chance of meeting this covenant, which applies to both bank debt and notes.

PGF is going to have to negotiate immediately with their secured creditors a 6 month extension (which is currently what they disclosed) but during this six month period will have to negotiate with noteholders and the banks alike to come to a consolidated credit agreement. This is not going to be easy. In other words, we have a credit crunch.

The stock took a nose dive from 73 cents down to 51 cents in today’s trading, but has somehow managed to recover to the 74 cent level despite this news, which I found very fascinating.

The only real wildcard in this entire matter is (billionaire and former large Canadian Oil Sands investor that opposed the merger with Suncor) Seymour Schulich’s huge equity stake in the entity, owning about 29% of the company. Will he bail them out before the banks decide to take the entire firm for themselves?