Enbridge has sweetened its offer for Spectra Energy Partners (NYSE: SEP) from the initially proposed 1.0123 shares of Enbridge per SEP to 1.1 shares of Enbridge (a 9.8% increase).

Enbridge common shares are down 2% as a result, but SEP is up 3% as a result of the increased consideration. It appears the market baked in about half of the expected appreciation over the prevailing 1.0123 share ratio:

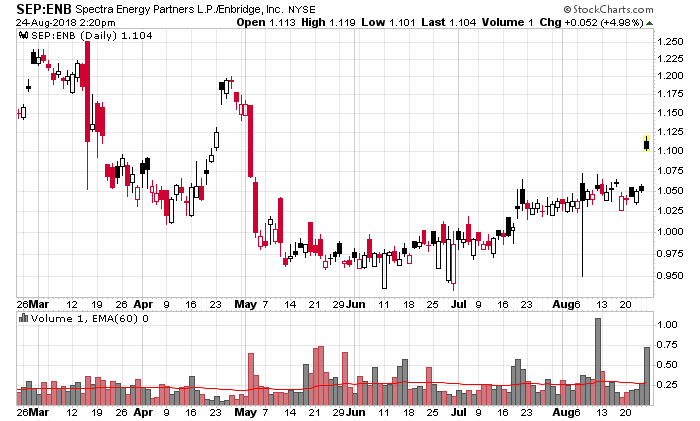

A factor quoted in the press release was the July 18, 2018 FERC Order – and you can also see this implied increase in value on the SEP:ENB chart above.

I will note that this is a fait accompli as the salient sentence in the press release is the following:

As the majority SEP unitholder (83% of total SEP common units outstanding), Enbridge’s approval by consent will constitute the requisite SEP unitholder vote required to approve the transaction.

Unitholders were more or less in it for the ride and short of a minority shareholder oppression lawsuit, it was going to get done at any “reasonable” price.

What is interesting is that Enbridge is concurrently attempting to consolidate its other master limited partnership, Enbridge Enterprise Partners (NYSE: EEP) and related entity (NYSE: EEQ). I have written about EEP in a previous analysis.

An argument by analogy (not air-tight by any means but does have merit) is that if SEP receives a 10% boost in consideration, EEP should be receiving the same, especially considering that EEP, in addition to the July 18, 2018 FERC ruling order, has under its belt a major positive ruling with the Line 3 expansion in Minnesota – one that was received after the initial proposal of 0.3083 shares of ENB per EEP unit. The other factor is that EEP unitholder approval is not guaranteed – EEP requires 2/3rds unitholder approval and Enbridge controls about a third of the vote.

A lot of Canadians are also invested in Enbridge Income Fund (TSX: ENF) which is also affected by this. However, Enbridge has an 82% interest in ENF so they will have to take whatever they are offered, within reason. ENF also does not have the benefit of having the July 18, 2018 partial reversal of the FERC ruling as it is mostly about Canadian operations (where the FERC doesn’t apply). I do not believe ENF holders that are waiting for a boost in the exchange ratio will end up with a happy outcome. Right now ENF:ENB is trading at 0.732 while the proposed exchange ratio was 0.7029.

My general expectation is that EEP unitholders will be offered 0.35 shares of Enbridge, or about a 14% boost-up from the existing offer. As Enbridge is likely to shade down in price as a result of the increased consideration for merging, I would expect the EEP price upon transaction announcement to settle around the $12.10 range. This is a relatively thin value play. I had a not inconsiderable amount of call options on EEP after the initial FERC announcement, but I added slightly to my position today – the downside risk is quite limited.

[…] I’ve been writing about Enbridge (NYSE: ENB) and their process of re-acquiring their daughter entities, including EEP, EEQ and ENF. They already formalized the arrangement with Spectra Energy Partners (NYSE: SEP), which I wrote about earlier. […]