Right now the largest yielding preferred shares trading on the TSX are of Dundee Corporation (TSX: DC.A), consisting of two series: (TSX: DC.PR.B and DC.PR.D). They are trading under 40% of par and current yields of roughly 14.5%. A long time ago, I had invested in their redeemable preferred shares, but I have not touched them since their maturity extension.

James Hymas had fairly cogent remarks that I would suggest that you read.

I will add that Dundee’s last quarterly report is an absolute disaster. Most of their consolidated operating subsidiaries are losing money. The two posting profits are Dundee Energy and United Hydrocarbon. Dundee Energy is now a shell stripped of its operating assets, and United Hydrocarbon is posting profits on the basis of probabilistic revenues with “contingent consideration” on the outcome of events in the Republic of Chad. (Where is Chad? Google Map link here – I normally consider myself good at geography, but my mind had to struggle with this one…)

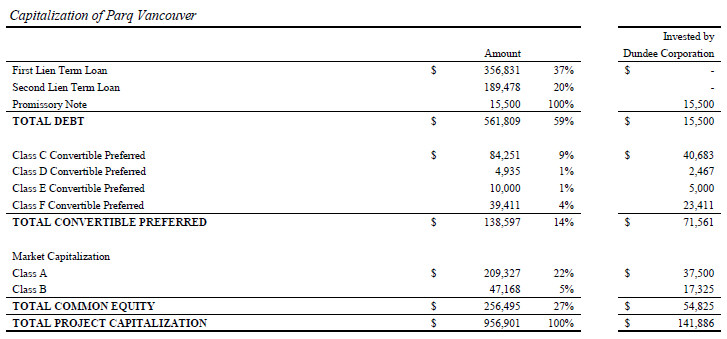

Their flagship real estate project, Parq project in Vancouver (via a limited partnership in Paragon Holdings) is deeply in the red. The operating loss in the first half of 2018 was $13.9 million (and a total accounting loss of $80.8 million as they have amortization and also had to write down their Paragon Holdings value to nil). The financing load is killer – $52 million in interest for the first half. Remember my post about revenues and domestic currencies and loaning money in USD? $26.6 million in foreign exchange losses due to Canadian dollar depreciation. They’ve had to inject emergency capital into the entity and Dundee had to float them a $15.5 million loan at an interest rate of …. 20%!

The Corporation provided an additional $15.5 million in the form of a 20% convertible promissory note during the second quarter of 2018. The convertible promissory note matures on October 1, 2018.

Given that Dundee is behind $546 million dollars of first and second-lien debt in Paragron’s capital structure, Dundee is faced with a horrible choice – give it up, or dump more money into the fireplace.

How the heck can you lose money on Vancouver real estate? Dundee’s apparently figured out the way to do it.

The only silver lining is that their balance sheet still has liquid assets they can transform into cash. Publicly traded investments include $164 million, but $114 million of it is Dundee Precious Metals (TSX: DPM) (down to $107 million today). This would not be easy to liquidate quickly. Their $18 million investment in eCobalt (TSX: ECS) is down nearly half of what it was on the June 30, 2018 valuation date!

The rest of these investments are private and would be even more difficult to liquidate.

The holding company also has no debt – consolidated, there are about $110 million in loans outstanding, but these are in subsidiaries that do not have recourse to Dundee. Half of this debt will go with the disposition of the Energy subsidiary.

Holding company cash is $30.5 million. Adding this to the aforementioned $110 million in publicly traded securities should give Dundee some time to work with. They also have an open credit facility of $80 million. The operations are burning $10 million a quarter, but this should decline in the future as they sell off or get rid of these businesses.

The real fly in the ointment is the upcoming June 2019 redemption of DC.PR.E, which is puttable by holders after that date. This is a $82 million real liability. My guess is that management will float another crappy proposal to extend the maturity. If this fails (indeed, the terms would have to be significantly more generous than the previous offering in light of the fact that the other preferred shares are trading at a 14%+ yield), given the liquidity situation of Dundee, this will probably be redeemed in shares at the minimum price of $2.

This leaves the other preferred shares. Par value of a total of $130 million and giving out a dividend of $7.3 million a year (until the September 2019 rate reset, which will likely lead to higher distributions). Will Dundee be able to pay it? Clearly they can currently, but will the entity figure out a way to eventually make money to be able to pay these dividends in the future?

I think the bargaining power of the DC.PR.E holders is a lot lower than last time around as the stock is now well under $2 and they definitely don’t want 12.5 shares of DC.A at these prices.

Yes, that will likely be the ultimatum bid. Accept another 3 year extension with no change in coupon or we’ll convert to shares and really show you how it’s done!

[…] Divestor weighed in on Dundee Corporation’s preferred shares (disclosure: I own some), and had some thoughts about the tire fire of a company. From now on this […]

Yeah for sure! And if the Goodman’s really believe their NAV, they could probably do a SIB at a $1 afterwards and buy most of the stock back.

I do believe there is no chance they settle the class E prefs in cash next June. Most likely an extension and less likely settled with common. Either way, I think that’s constructive for the class B and D prefs on a relative basis.

@Safety: That’s the other thing, the lack of any insider activity is quite telling. If they believe their book value is actually what it is really, they’d be idiots for not pouncing on their own stock. Maybe 15% perpetual yields on their preferred shares isn’t enough of a hurdle?

I tend to agree on that.

I pressed John on that after the AGM and he said vaguely that he would like to buy the common and the class B/D preferred soon. I’m not sure what’s holding him back except perhaps he is restricted or he was just telling me what I wanted to hear.