The on-again, off-again rumours regarding a billion-dollar injection with the Canadian government is purely negotiation strategies on both parts. The government wants to invest, but they also want to do it in a manner that allows them to save face. Conversely, the controlling shareholders of Bombardier want the money (it will indirectly end up in their pockets), but they also do not want to lose control over the gravy machine.

There will be a happy equilibrium where the taxpayers of Canada will transfer wealth to the owners of Bombardier, but the structure of the arrangement is up for debate. My suspicion is that some sort of arrangement will be made as long as they keep a certain number of jobs in Quebec, the Class A share owners will not be compelled to convert into Class B shares.

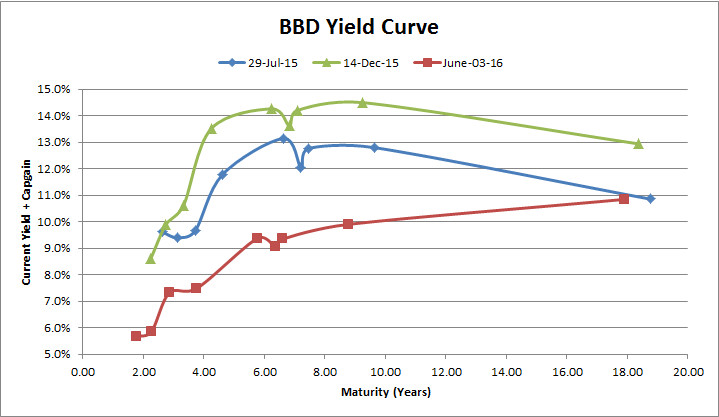

The credit market has been much more kinder to Bombardier, to the point where they can raise capital at a very reasonable rate:

The Class B equity has been hovering at $2/share, with the control premium (Class A shares) being around 10% of late.

Floating rate preferred shares (TSX: BBD.PR.B) has been hovering around 8.4% yield, while fixed-rate with conversion risk (TSX: BBD.PR.C) has been hovering around 9.9% of late.

As I alluded to earlier, investors must make a distinction between revenues and profit, and Bombardier is focussed on revenues at the moment. They will continue to service their debt and preferred shareholders, but I do not believe equity holders will be receiving dividends anytime soon. There is also a significant overhang with the two Quebec deals, with a significant number of warrants outstanding at US$1.66 level – although these warrants are held by institutional owners (Quebec), this will be a valuation overhang which will serve to depress the maximum upside of the common shares. If it ever gets to the point where these warrants are exercised, it would buffer the serviceability of debt and preferred share dividends.

I am of the general belief that if Bombardier plods along and returns to a profitability at a level that is somewhat less than what they have touted in their 2020 vision, and that their C-series jet clearly has a “runway” of perpetual orders keeping the assembly lines busy, that BBD.PR.C would trade around the 8% level (or roughly $19.50/share). The credit markets are indeed pointing toward this direction.

Now the corporation just has to make money.

I am still long their preferred shares, but under the belief that a good quantity of upside has been realized by investors in relation to previous trading prices. I went long on preferred shares less than a year ago when there was a lot more gloom and doom, and having been called a “brave soul” by national media for doing so.