Kinder Morgan (NYSE: KMI) is in a chicken-and-egg situation. It needs financing to implement capital projects, but the cost of its financing has been steadily increasing due to its financing requirements.

Energy pipeline equities are a staple income producer for a lot of funds out there, but if they have their dividends threatened, the supply dump is going to be gigantic.

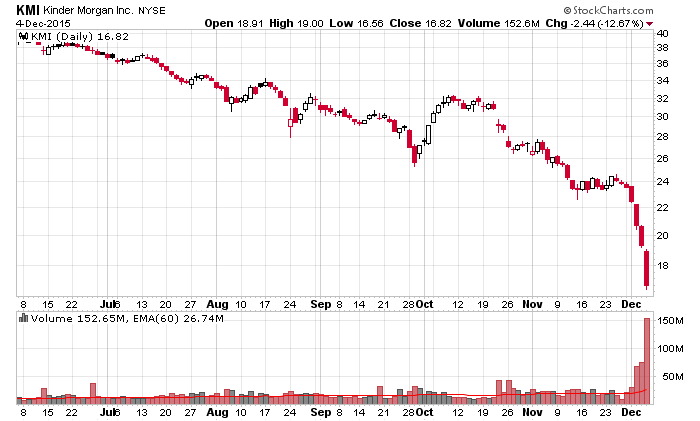

I sense this is a falling knife situation where it will be very difficult to predict the bottom. You can make an excuse for US$16.84/share being the bottom, or you can also make an excuse for US$9/share. It just depends on how many funds are hitting that sell button, irrespective of price.

Cash-wise, it is very evident they will have to cut their huge dividend. They are giving out US$4.5 billion a year and it is completely obvious they cannot sustain it given their capital spending profile (offset with their not inconsiderable positive operating cash flows). Refinancing their debt ($3 billion of it current as of September 30, 2015) is going to be progressively expensive as bond yields rise and their equity price drops. They do have a credit facility with $3.4 billion availability, but their buffer is thin!

I am sure Kinder Morgan will recover this financial earthquake, but how low will their common stock go before they recover?

Finally, let this be a lesson those that invest in highly leveraged industries (e.g. power generation, pipelines, etc.) – you never know when the market will arbitrarily pull the rug on your refinancing program.

Kinder Morgan’s clever financial engineering finally caught up with it. It really feels like one of those typically income trusts, in that it over-distributes (dividend coverage ratio is quite bad last yr), consistently misses on revenue / earnings, too much debt on the balance sheet and too slow to realize the underlying business environment is deteriorating (their CO2 business is more sensitive to oil prices).

A dividend cut would hurt the stock on the short-term but ensure the long term viability of the business. Let’s just hope it doesn’t end up being similar to those sad ending income trust.

The overall entity makes money and not an inconsiderable amount of it, so their equity value should be non-zero, but this will be after a lot of pain to get their debt ratio in order (i.e. cutting their dividend to zero).

The question is whether for the knife catchers this is at US$15.50/share or US$5.50, or US$0.50! If I was to make a wild guess, around $8/share, but just like most good panics, the very bottom prices are not usually seen for more than an intraday purge of the last exhausted market participants that have thrown up their arms and hit the sell button at any price.

Slash their dividend by 75% – a very prudent thing to do and I guess Richard Kinder has a lot of skin in his own baby. It is tumbling after hours. See where the dust settles. Certainly worthy of moving in if it does go to $8.

I myself work for a pipeline company (not Kinder Morgan) and to be honest, a bit skeptical of the balance sheet and all the financial engineering.

The 9.75% mandatory convertible prefers (with par value of $50 and a conversion ratio to common capped between 1.544 to 1.8412) initially fell in tandem with the common but now reacts positively to the news.

Financially they’d be better off slashing it entirely but I’m guessing they’re still aiming to keep the income funds invested in their equity so they can do another public offering.

The preferred shares I wouldn’t touch at all – they are not truly “preferred” in the traditional sense – the mandatory conversion coupled with the common share decrease should make them priced as 1.8412 common shares plus the coupon premiums and unless if you are into razor-edge arbitrage then only the common should be in any sort of play at all.

Oh, and they said they’d not do another equity offering, but “for the foreseeable future” for these guys is about 24 hours…

Moody saves the day and stopped the plunge. When did the rating agency acts this fast?