This is part of a long-continuing series covering Genworth MI (TSX: MIC). I will give the changes that I see salient over the past few months.

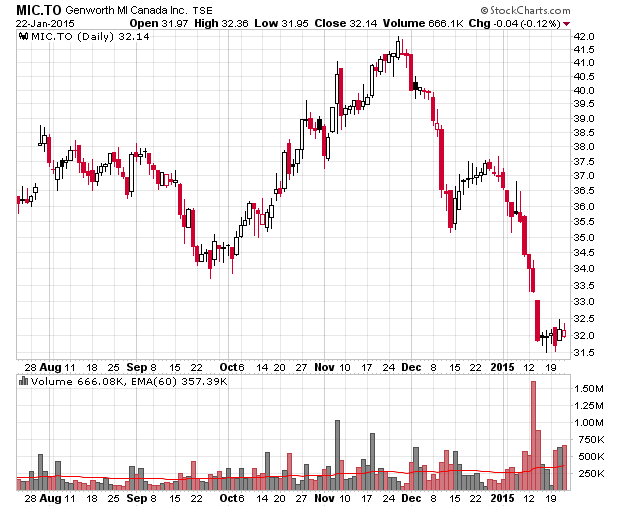

The past two months of price action has seen an approximate 20% decline in common share price:

This is likely due to market perception of increased default rates in mortgages, especially in the Alberta and Saskatchewan markets (the two provinces in Canada with the most negative bias to lower oil prices). At the Q3-2014 report, Alberta has 17% of the insurance in force, while Saskatchewan is 3%. Both provinces have very low delinquency rates (0.09% and 0.12%, respectively).

This will undoubtedly climb up as property will flood the market in the wake of layoffs and capital expense reduction of the oil majors.

The frequency of mortgage defaults is strongly affected by unemployment rates, while the severity of defaults is determined by property valuations. I would expect management would touch upon the impact of Alberta and also the impact of a potential recession in Canada and how it would affect mortgage defaults. As I have mentioned in the past, Genworth’s loss ratios are at all-time lows and this is an abnormal condition.

The other item of note is that management has repurchased $32 million in shares (799,345 shares) between mid-November to early December, at an average of $40.04/share. This was probably the worst example of market timing I have seen in quite some time and was a transaction above book value. In other words, this will be a negative value transaction to shareholders.

Normally management has been a little more cautious with shareholder capital (demonstrated by their willingness to give a sizable special dividend of excess capital in the previous quarter), but this decision is relatively questionable.

Company management had a shift which I deemed relatively minor – the CEO is resigning and becoming the executive chairman of the board; while the COO is now becoming the CEO. This continuity in management would suggest no major strategic changes in the pipeline.

Tangible book value, pro-forma to the buyback, will be around $34.50/share at Q3-2014. This also includes other accumulated comprehensive income and also deferred policy acquisition costs (which is effectively an intangible asset that represents cash paid to acquire business).

At Q3-2014, they did have exposure to $32 million in energy equities and $253 million in energy fixed income investments out of a $5.6 billion portfolio. It will be interesting to see if they got hit during the quarter on energy.

On a positive note, their fixed income portfolio will very likely accrue an increase in fair value as interest rates have continued to drop over the quarter. Indeed, with the Bank of Canada’s interest rate drop, they will be experiencing even higher gains in Q1-2015.

This will pose reinvestment risk, however. Most insurance companies (and pensions) are really struggling to find high quality investments that give out yield. In the low interest rate environment, this will suppress portfolio yields and will result in more expensive policies.

A slowdown in the Canadian real estate market would have an adverse effect on premium generation. That said, with last year’s price increase by CMHC, and little in the way of market competition, I would view the company as generating more premiums than recognizing at present. For the first 3 quarters in 2014, the company took in $461 in premiums and recognized $422 million in revenues. The decline in revenue recognition should reverse in 2015 and beyond.

In balance, considering the risks in the Canadian real estate market, Genworth MI’s position, and current market valuation, I believe Genworth MI at CAD$32/share is slightly undervalued. While it is not at a low enough price for me to add shares, it is something I am comfortable holding at existing price levels. I do not see Canada’s real estate market imploding, although it is certainly going to be rough going for those that have bought million dollar homes in Alberta and finding they have been laid off in the oil patch.

Disclosure: I have been long on MIC.TO since July 2012. I sold a good chunk of my holdings in 2014 but still hold a reasonable amount today.