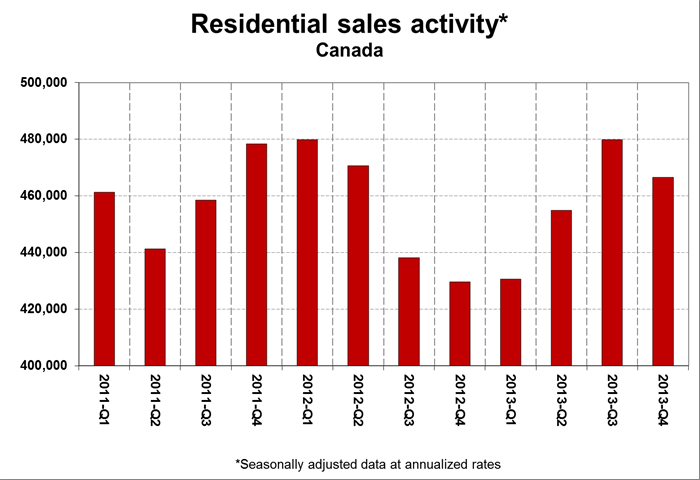

Genworth MI (TSX: MIC) will report its quarterly and year-end results on February 4th. I am not expecting too much deviation from the previous year’s quarter. From the CREA, sales activity nationally are slightly higher than the levels they were in the previous year. The previous year had seasonal-related issues and this year (either Q4-2013 or Q1-2014) will likely have some seasonal-related issues due to the deep freeze that affected the eastern half of North America. These weather related events will only shift demand around periods rather than reducing it.

Due to the latest federal regulatory changes (tightening) in mortgage financing kicking in on July 2012 (but constructively pulling some demand from Q4-2012 onwards into Q3-2012), year-to-year underwriting will likely be flattish from Q4-2012 because this will be the first full year-to-year comparison with the new regulations kicking in.

We can see the predominant trends for the company – premiums earned (the revenues earned from the actuarial performance of the mortgages that are being insured) continues to degrade slightly because of the run-down of past premiums written:

The only other item that I will mention is that claims and delinquent mortgages appear to be at an all-time low in Canada, despite all the talk about high consumer debt-to-income ratios. This will eventually blow up in the faces of those that have accumulated the debt in the first place, but not today. The lack of mortgage delinquencies will continue to mean that Genworth MI will be a cash generation machine.

There are a few negatives coming along the horizon. One is that profitability of this magnitude tends to involve competitors, and I see Canada Guaranty is trying to cash in on this market – however, the barriers to entry with respect to regulatory compliance is not trivial and establishing sales networks and funnels will take quite a bit of time.

Another is that the OSFI is continuing to look at the capital framework on the property and casualty insurance industry in Canada. In 2012, there was a significant change in the government guarantee fund which resulted in surplus funds being released to the company. This risk is offset somewhat due to some guidelines already being released: for those that have the stomach to read this stuff, you can review the draft guidelines here, effective January 1, 2015.

Another negative are the usual concerns over the Canadian housing market that I won’t bother repeating here.

I do not foresee MIC continuing the share buyback at this price level, nor have I seen any insider purchases from SEDI lately. The last slab of shares were repurchased in September at $29.23. They increased the dividend in the last quarter (they have been doing it on a yearly basis) and while I do not see them raising it again, depending on the results of the regulatory review, they do have room to declare a special dividend in the future.

Solvency-wise, the only maturity on the horizon they have is $150 million face value at December 15, 2015. This debt issue has a coupon of 4.59% and in 22 months they can decide whether to refinance or just pay it off. Management is also in a position to pay off about a $3/share special dividend and likely be within their own internal targets for minimum capital.

To summarize, I am not expecting fireworks out of this quarter, but I do expect consistent performance in line with previous quarters. The company is far from the bargain basement price it was a year and a half ago, but I do believe it is continuing to trade within what I would consider my fair value range. In the meantime, they continue to spit out cash.