Two observations – Berkshire announced that it will repurchase its own shares at no more than a 10% premium to book value. The stock went up about 8% in trading during the session to roughly this level. Book value is $163 billion, while the company has 1.649 million class “A” equivalent outstanding for a book value of about $98,850 per share. Add 10% and this gives a value of roughly $108,700 per share, not too far from the closing price.

I find this interesting simply because Warren Buffett is now a net seller of his own company and he is quite good at using his mouth to talk up or down the market when it suits his purposes – there tends to be a media aura that he is relatively altruistic. I am not convinced that Berkshire makes a compelling value as its analysis is not that easy – essentially an insurance operation with a series of fully-consolidated subsidiaries and a hodge-podge smattering of equity in various well-known companies (including Burlington Northern). When at the scale of Berkshire, the rules of engagement are considerably different since it takes forever to build and exit positions – not as easy as plugging in a market order to buy 100 shares of Microsoft.

The last time Buffett talked about buying back his own shares was when it was trading at $40,000 at the peak of the tech bubble. He graciously offered anybody that was willing to sell at that price can call him up and sell it to him at the prevailing bid on the NYSE at the time. Nobody took him up on that offer.

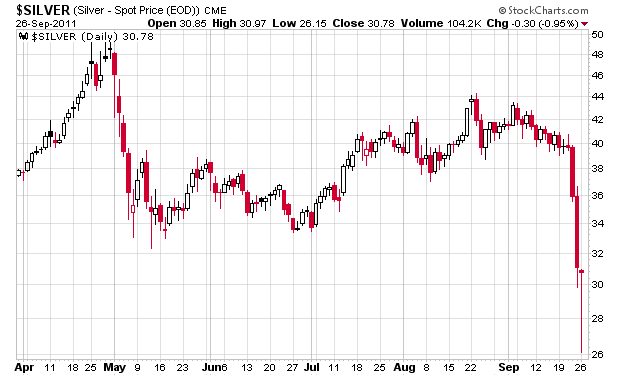

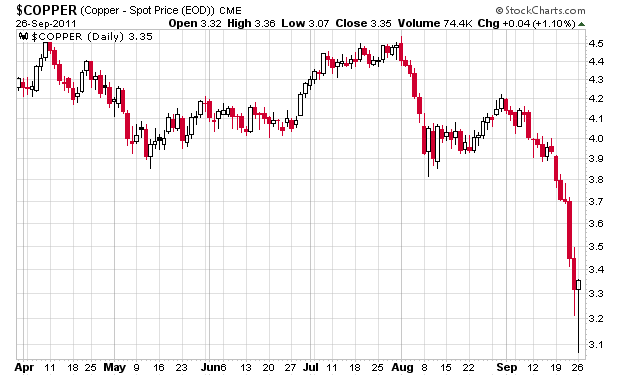

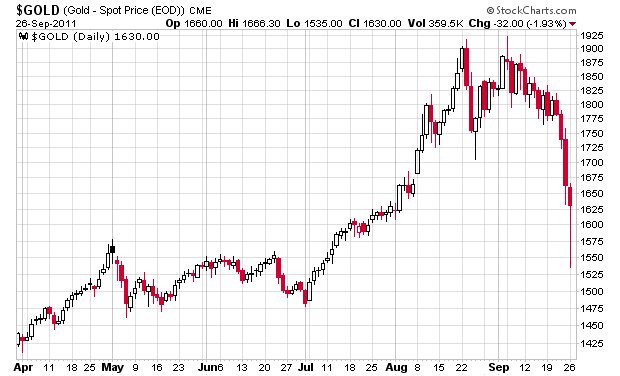

The other observation is commodity prices appear to have developed a “spike” on the charts. Observe the following:

Although I am hardly a technical trader, my best guess at this time is that the three commodities will head up for the rest of the week or so before declining again and “retesting” the bottom of that spike and likely trending down. There was clearly some sort of liquidation that has been occurring and the market is not that deep.