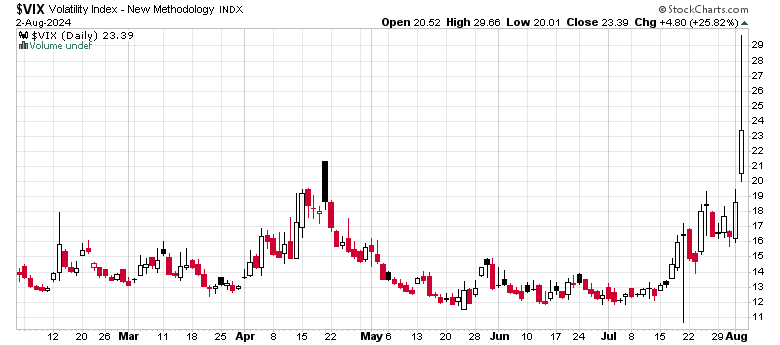

The last two days have been quite stirring. In particular, on Friday’s trading, the volatility index spiked up to 29, which is the highest it has been since the Silicon Valley Bank debacle:

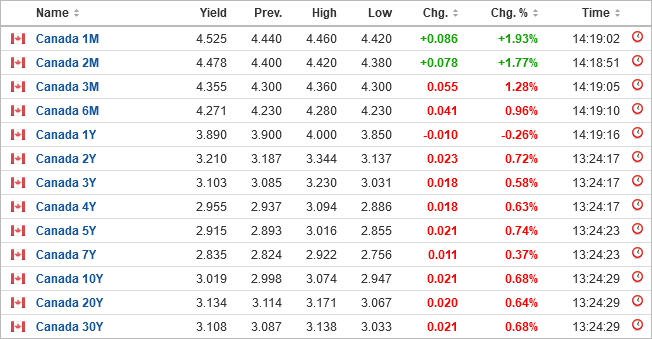

Notably, the yield curve also dived down, with the GoC 5-year going south of 3% for the first time in awhile:

There are a few lead theories that I’m thinking. In no particular order:

The “day of reckoning” of tightening interest rates is finally hitting the markets in some sort of liquidity crunch. Somebody big needed liquidity and decided to hit all the bids.

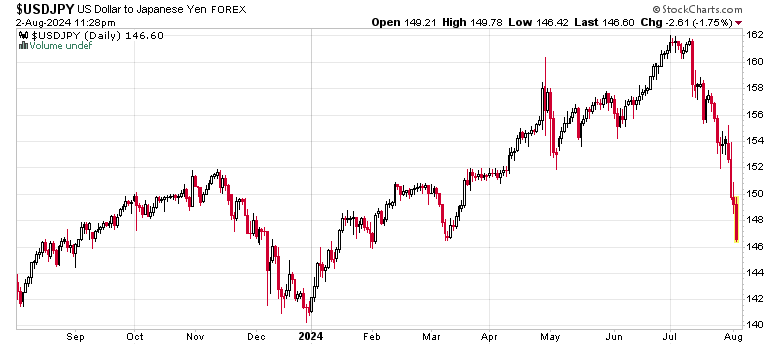

Was there somebody big that was caught short the Japanese Yen and spontaneously triggered a liquidation?

The commodity complex has also gotten hammered. For example, CNQ and CVE reported quite decent quarterly results, but their stocks have been taken down 10% since then (and WTI has dropped from US$77 to US$73 in short order).

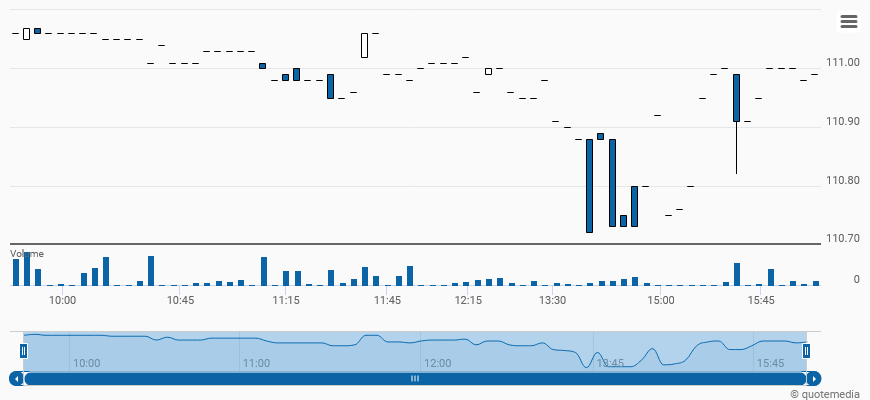

Finally something that might be concerning is the liquidity of cash ETFs – in particular, I note that HSUV.u (the US dollar corporate class fund) in intraday trading actually was trading 0.3% below NAV in very illiquid trading (note: NAV is 111.01):

Somebody holding this fund was demanding US dollars in the middle of the trading day and simply was not getting it. This is the hallmark of liquidity issues during a market volatility event.

My gut says there is more to come, so don’t buy too early. However, I’m well positioned for something catastrophic occurring.

I thought this was great from ADG: Grant’s | Almost Daily Grant’s (grantspub.com)

“It’s the rate of change [of interest rate differentials] that matters,” James Malcolm, head of FX strategy at UBS, told Reuters. “And so, if the BoJ are stepping up the pace of rate hikes relative to market pricing, and if the Fed is also becoming in play [for rate cuts] here, then the pressure on the carry trade increases.”

As an influx of income-seeking foreign capital has provided a persistent tailwind for stateside stocks, the unwinding of that dynamic reciprocally presents un-bullish implications. “The now evident vulnerability of U.S. equity prices to a rise in the yen exchange rate warns of the consequences for U.S. asset prices and developed-world asset prices in general from monetary policy changes in the East,” Russell Napier wrote in Tuesday’s latest edition of The Solid Ground.

Contending that a narrowing interest rate differential – rather than the wholesale repatriation of capital by income seeking Japanese investors – has driven the recent FX snap back, Napier likewise concludes that the sharp share price downdraft “is the shape of things to come and an indicator to investors of how interrelated U.S. equity valuations are with the global financial system.”

——-

Let’s add some overlevered pods playing momentum in the chip stocks and this could get rough for passive indices.