Continuing on from my April 19, 2024 post about the board room and proxy drama occurring at Slate Office REIT, we have the following developments:

April 20, 2024 – an incumbent trustee decides to not run again, and in replacement Armoyan’s nominee is put forward (Scott Dorsey).

Following receipt of the Notice, Lori-Ann Beausoleil advised the Board that she is declining to stand for re-election to the Board and tendered her resignation as a trustee of the REIT effective May 2, 2024 and, thus, will not be standing for re-election at the Meeting. Following unsuccessful attempts by the REIT to come to a cooperative outcome with Mr. Armoyan, and in light of the resignation of one of the Board’s nominees for election at the Meeting, on the recommendation of the Governance Committee, the Board resolved to nominate Scott Dorsey in place of Ms. Beausoleil and to add Mr. Dorsey to the REIT’s slate of management nominees to be considered for election as trustees at the Meeting. Mr. Dorsey is also one of the individuals put forward by Armco.

April 24, 2024 – another incumbent trustee, Jean-Charles Angers, decides to not run again (obviously knowing that the writing is on the wall and he would not win a seat).

May 2, 2024 – Slate reports their quarterly result, a rather tepid quarter. FFO and AFFO is roughly $4 million. Loan-to-value still hovering around 68% and interest expenses creeping higher. They are basically continuing their slow fire-sale of properties to try to deleverage.

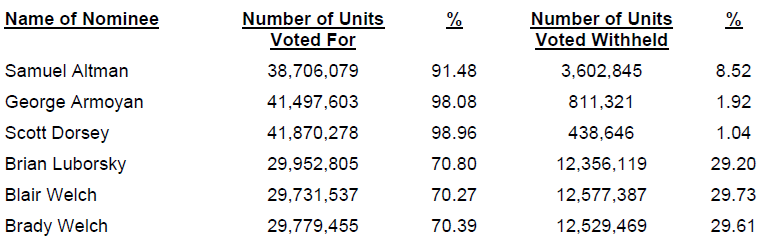

May 3, 2024 – AGM day! Voting results:

Brian Luborsky and Scott Dorsey and Sam Altman were endorsed by Armoyan.

And finally, after the vote…

May 8, 2024 –

Slate Office REIT (TSX: SOT.UN) (the “REIT”), an owner and operator of high-quality workplace real estate, announced today that Scott Dorsey has informed the REIT that, for personal reasons, he is unable to serve as a trustee on the REIT’s board of trustees.

What??? Who strong-armed him into leaving Slate with a five-trustee board?

Practically speaking, it appears the George Armoyan takeover of Slate Office REIT is nearly complete. The question at this point is what he can salvage from the entrails of this debt-laden entity before it will have to go through some inevitable recapitalization.

On the conference call, Armstrong suggested that 30% below IFRS was good number for the recent dispositions (after saying 30-40% moments earlier). If SOT’s entire property book was disposed 40% below IFRS, shareholder equity would be very close to zero (at 30% below, it would be about $100M). The game that seems to be afoot is to destroy just enough IFRS value in the property book to reset SOT’s financial metrics to make it investable again. I wouldn’t make a big bet against the Armoyan’s ability to pull it off.

It’s interesting how the debentures that are trading well below par are real-estate related:

HOT.db.u

IVQ.db.u/v

MPCT.db.a

MR.db.b was looking questionable half a year ago, notably they cut the yield to zero

NWH.db.h/i

and finally, Slate is in the basement. If there is any recovery scenario, these debts would be golden… the problem is I just can’t see it happening. Their management hasn’t had a lot of credibility about their remarks in their presentations. Perhaps Armoyan swoops in to the rescue with a bailout package but how much would he want to plough into this thing? Or is there some sort of tax angle?

“If there is any recovery scenario, these debts would be golden… the problem is I just can’t see it happening. “

Ever? Someday we will have a normal yield curve. Is it not a matter of time and whether (or not) each entity can manage their way until then and how much more damage there might be to unit holder equity? For those entities that do manage the gap, these debts may indeed be golden.

The first tranche of debentures matures on February 2026 (and this isn’t even a large one) so they do have some time to work with. But in the meantime they’ll also have to renew a bunch of mortgages at higher interest rates……

Now Scott left, and stock dropped to $0.38 today as of June 17.

Is george still in control in board?

George and Welch brothers have 30% shares in total, why do they allow the stock price drop to this low?

Can they let slate office keep losing money by selling office cheap to their friends/family members or themselves and benefit from it?

How much chance is the company go bankrupt?

Thanks