I’ll just republish a CNBC article from mainstream media, noting this is the USA and not Canada we are talking about:

“Private sector companies added 497,000 jobs in June, more than double expectations, ADP says”

The sub-headline:

“Leisure and hospitality led with 232,000 new hires, followed by construction with 97,000, and trade, transportation and utilities at 90,000.”

ADP is a private sector payroll processor, so they have fairly good visibility on payroll data.

This much awaited recession is not yet happening, folks! It would be the oddest recession in economic history which still clearly had full employment.

As I wrote in yesterday’s article, “Essentially until we start seeing a gross contraction of employment demand, upward wage pressure should put a floor on inflation.”

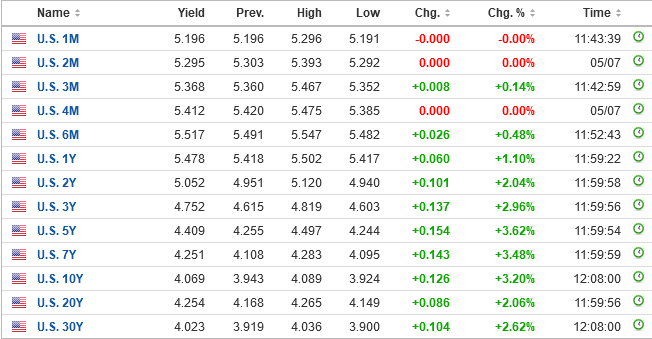

So this “good news” (people working) is resulting in “bad news”, namely looking at the interest rate curve:

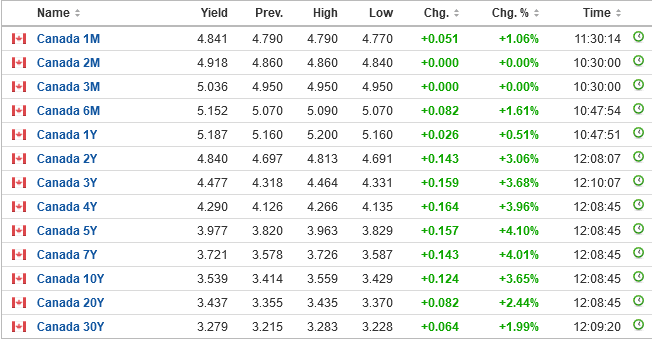

Canada, which is joined at the hip with the US in many things economically, also has a yield boost:

The far end of the yield curve (the 10 year point and beyond) is a core calculation for many asset management models. If that yield goes higher, more money gets allocated to fixed income than equities – for example, why bother buying the S&P 500 at 4% when you can buy its debt at 5%?

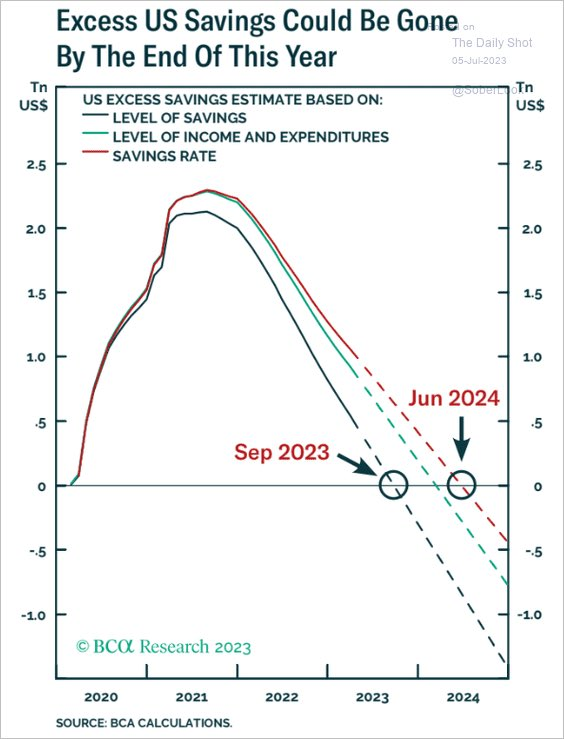

Here is the economic dynamic going on, based on this chart:

I don’t know how accurate this is, but essentially governments gave out a lot of surplus to consumers during Covid and they are still in the process of paring this surplus down. We are getting to the point where many people must pare back luxury expenditures (this would be leisure and hospitality spending, and those sectors have exhibited massive amounts of inflation – take a look at Expedia if you do not believe me) or earn more money (which they can through employment).

Either way, until we start getting reams of unemployment, those interest rates are going to stay higher for longer. I’d venture to say that broad market equity prices probably will peak out this summer. They are having difficulty competing against the returns in the bond market.

The ultimate silver lining, however, is that lower prices mean higher returns. If your companies are generating copious amounts of free cash flows, it doesn’t really matter. If, however, your companies are trading with a market value that is a very rosy projection of elevated future earnings, you may wish to check your risk.

The trick with obtaining these higher returns, however, is that you have the cash on hand to purchase at lower prices. If you’ve already spent the money, you’re out of luck.

The Bank of Canada will raise rates 0.25% to 5.00% on July 12th; the Federal Reserve will raise its funds rate from 5.00-5.25% to 5.25-5.50% on July 26th. There is also an outside chance that QT will be accelerated in an attempt to flatten the yield curve (selling long-term treasuries and buying the 2 to 9 year part of the curve). Buckle up!

Expecting to see the “transitory inflation” narrative back. Of course it was transitory, we just didn’t mention its going to be 3-4 years as opposed to 6-12 months.