In highly anticipated news, First Republic (NYSE: FRC) went bye-bye over the weekend.

As long as the yield curve remains inverted and quantitative easing continues, financial institutions are going to receive continued pressure and the “too big to fail” institutions will be the ones to vacuum up the money.

Think of it this way – behind each bank asset (a customer loan) is a bank liability (a customer deposit). If the asset to liability situation goes out of regulatory proportions (e.g. you took your customer loans and invested in them in high-duration government debt and suddenly your customer wants their deposits back and you can’t pay it), you get FDIC’ed. However, when the FDIC process occurs, it is not as if all of that capital goes away – it has to go somewhere. It doesn’t end up as paper banknotes inside the safe or underneath the couch, but rather it goes to another financial institution. The assets and liabilities go somewhere else within the financial net – they do not vanish!

In this case, it appears destined that the assets in this digital financial world (where assets get transferred with mouse clicks) will bubble up to the systemically important banks.

I’ve been trying to pick away at the entrails of the lesser banks within the USA, but I don’t have a clue how to project who will survive and who will not. So I’ve given up.

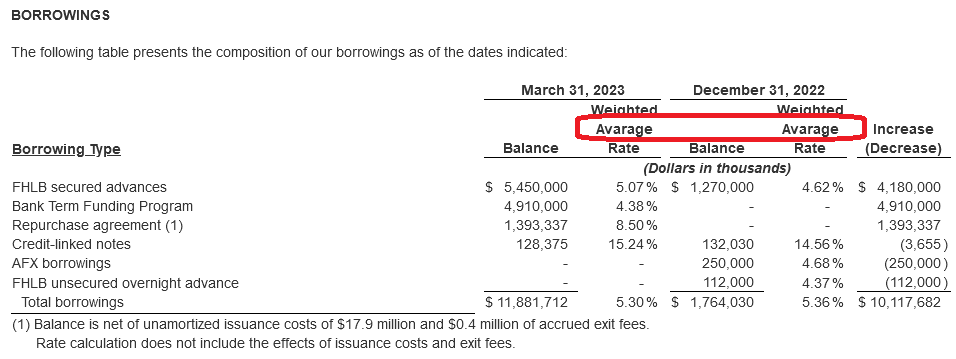

I will leave this post with one amusing note. Financial releases go through plenty of review cycles within management, but if they can’t spell the word “average” correctly, it is trouble:

My professor of banking used to say: “Banking business is simple. Make sure your duration is matched, everything else is manageable”.

Its amazing how many useless people sit in ALCO’s of these failed banks…

Oh, that typo is hilarious. Which bank is that from?!

None other than PACW.

OMG, that typo is a leading indicator 🙂