You could mistake the chart above for a technology company’s stock, but indeed it is the spot price of lumber per thousand board feet (about 2.4 cubic meters).

From a peak of $1,700 to $400 today represents a 76% drop.

What happened after Covid is now well known – demand for lumber went through the roof as people decided to focus on home improvement, while supply was curtailed due to labour issues.

As a result, 2020 to 2022 were record years for most lumber producers. We will use an example of Western Forest Products (TSX: WEF):

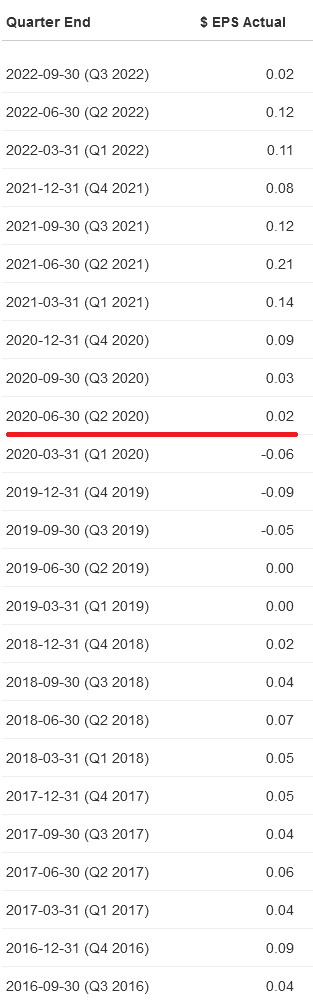

For the 12 months between Q4-2020 to Q3-2021 they made 56 cents per share.

Given that their stock was trading at around $2/share at the end of that period, you were looking at a price-to-earnings of 4, and even less on a price-to-free cash flow basis.

Four times past earnings looks like a very cheap valuation metric. However, had you invested in the stock at the end of Q3-2021 ($2.20/share), today you would be sitting on a loss of nearly 50%.

News is still not very good. Increasing interest rates, a moderation in the supply chain, and also the fact that nobody wants to work on their outdoor deck three years in a row has contributed to prices going back to ambient pre-Covid averages.

A few days ago, Western Forest announced:

Western Forest Products Inc. (TSX: WEF) (“Western” or the “Company”) today announced plans to temporarily reduce its lumber production output for the remainder of 2022 by approximately 20 million board feet to manage inventory levels to current market conditions.

Basically they’re taking most of December off. Hopefully the workers will have a good Christmas, but 2023 will bring more uncertainty. Uncertainty results in decreased prices.

Five analysts have put the 2023 fiscal year at an averaged estimated EPS of $0.22/share. At today’s stock price of $1.13, that would still be at a P/E of 5.

Despite the P/E expansion (going from 4 to 5 is a 25% increase), an investor at the cyclical top has lost a considerable amount of capital.

I also suspect that the 2023 estimate is still high.

It’s really difficult to sell something when you see the P/E at 4, but it was the right choice. My final sale was in May of 2021 at $2.25/share.

Investors in other commodities should be given caution. The tempo of commodity equities varies with the commodity, but universal to them all is the cyclicality. Time it well.

What amazes me is market’s ability to believe in “cycles”, sometimes contrary to any business logic.

WEF is now trading at 0.5 to book, which means there’s an asset impairment not yet recognized.

To make market valuation reasonable (i.e. price to book = 1), WEF need to completely write off inventory (265) and receivables (75), which is not realistic for obvious reasons. WEF does not have any material goodwill or other usual suspects to assets impairment.

As such, to support 50% discount to book value, market assumes that lumber prices should drop from current levels to something like 200-250 and stay there for a long period of time. This is, again, not realistic as lumber remains a key building material. Not to mention, that in worst case scenario, WEF could just cut production and minimize losses until favorable price comes back.

North American lumber production adjusts to new home construction and remodel/repair markets. Imports from/exports to other countries are a factor. Timber production/supply issues (e.g. pine beetle) affect pricing. Global pulp markets affect chip pricing (the other part of the log). Electricity markets affect wood residuals pricing. Gas prices affect production.

Market actors try to anticipate all of this and more. People who make money with lumber stocks either get the timing right on major moves of one or the above variables or they have a view of “mid-cycle” earnings that they use to determine when to add or sell to their positions.

At any given time, markets are always wrong about lumber stocks. Way too many moving parts.

I will note that Canfor yesterday announced mill curtailments for December and January.

@Dmitry, your argument about book value excludes another large vector for impairment, which is the the PP&E component. Given the history of WEF, they’ve gone through periods of time where they eat up cash like no tomorrow and end up significantly negative cash during the low of the cycle (almost always to the point of CCAAing themselves).

One of the most moronic capital allocation decisions they made was the share buyback. They bought back $97 million in 2021 for $2.03 and another $17 million for $1.75 in 2022 before they realized “We’re running out of money!”.

One other comment is that WEF’s portfolio also has concentrated exposure to regulatory issues in BC. Depending on the whims of the day of government, this also increases uncertainty.