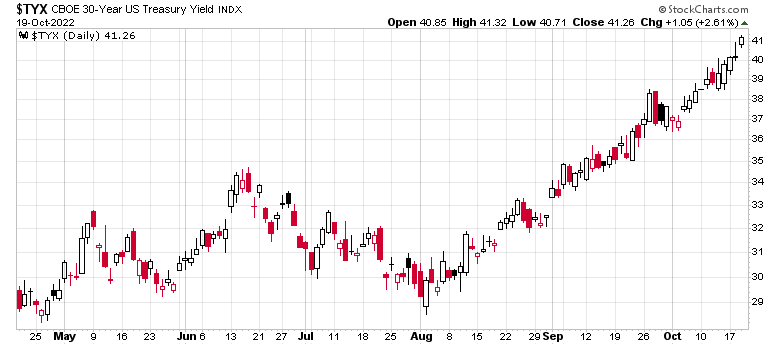

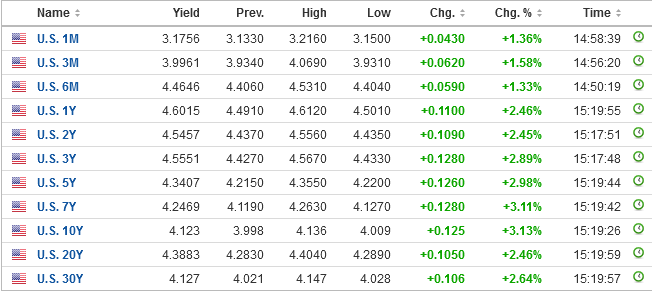

Yields are now higher on 30-year government bonds than they have been since 2011.

There was a time where you could put money away into government debt and earn a satisfactory return on investment, especially if you are into the annuity-type investments. For example, if you bottom-ticked the 30-Year US treasury bond in September 1981, your yield to maturity would have been north of 15%. Ignoring the coupon differential (as those bonds surely at the time would have been trading at a discount), pouring a million dollars into fixed income would yield off $150k/year for the next 30, virtually guaranteeing a high cash stream.

At the same time, your dreams of going into margin to buy such a financial product would have been unattractive because short term rates would have spiked up to 21% at the time. Speculating on buying 30-year government debt was exceptionally difficult at the time – high inflation, a massive recession, and just doom and gloom everywhere. Of course, such times tend to be perfect for buying assets which are being liquidated wholesale.

Timing the market is always subject to psychological urges and always looks easier in retrospect. One year earlier, in September 1980, the same bond yielded around 11%. At that time, CPI inflation from 1979 to 1980 averaged 13.5% and such a long-term investment would seemingly have been locking in a real negative rate of return. Had you invested in the 11% yielding long bond at the time, over the course of the following year you would still be sitting on significant capital losses (about 25%) a year later and looked quite stupid.

I don’t think we’re going to get to that magnitude of interest rates, but there is going to be a parallel between how CPI persists, and the continuing downward slope of the yield curve. It doesn’t appear to be the right time to pounce. It’s just not painful enough.

Don’t get me started on whoever got trapped into buying these things a year ago when yields were less than 2% – they’ve lost over a third of their capital at present. A large cohort would be pension funds that have gotten annihilated on fixed income, coupled with insurance companies that keep the bulk of their capital into the same financial instruments. Look to see massive losses on the comprehensive statements of income from these entities when they announce their upcoming quarters.

Speaking of insurance… While bonds effect would hit comprehensive incomes (which is rarely considered a KPI and is not part of eps calculation), insurance reserves drop (due to higher discount rates) would hit net income (and eps accordingly). There will be some lag, as reserves usually are reasessed at year end, but otherwise impact could be quite positive.