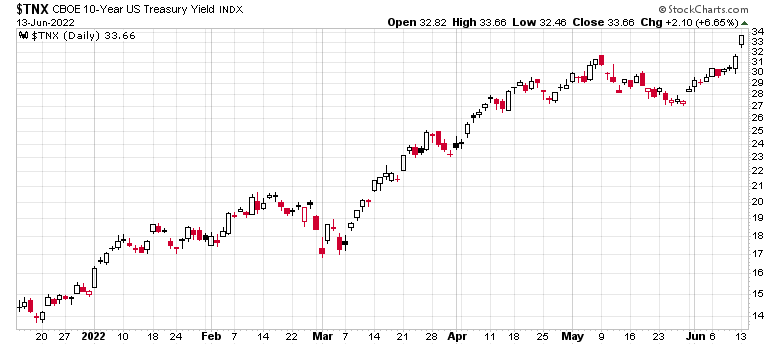

Both Canadian and American interest rate expectations have spiked considerably over the past two trading days.

On Wednesday it appears quite likely at this point that the Federal Reserve will raise its rate 75bps from a 0.75-1.00% band to 1.5-1.75% band. There is also an outside shot of a full 1% increase.

More relevantly, however, longer-term rate expectations have continued to creep higher:

Quantitative tightening hasn’t even gone on for two weeks and we are seeing the markets vomit.

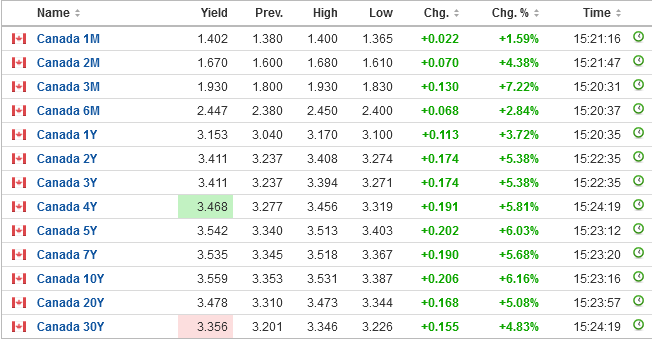

It is not much better in Canada either, with long-term rates elevating to levels not seen since before the economic crisis.

With the 5-year bond going up another 20bps today, mortgage rates will surely climb and this is going to kill credit availability. Specifically in Vancouver/Toronto, condominium holders are going to face two ugly decisions – either they continue to incur a deeply negative carrying cost (in relation to the amount of net rental income they can earn) or they will have to take increasingly larger haircut to prices in order to be able to obtain liquidity. There is definitely going to be a short period of time where people will try to get February pricing, but it will effectively be a no-bid market at those prices.

July 13th for the Bank of Canada is increasingly looking like a 75bps raise at this point (to a 2.25% target rate).

These interest rates are still on the low end historically in the pre-2008 history. The reversal of QE and the subsequent financial reverberations are going to crush leveraged finance in all forms, and markets will be seeking US cash as the safe haven (notably not Bitcoin, which is down about 20% as I write this).

The survivors are going to be companies that generate copious amounts of free cash flow with respect to their valuations. De-leveraging is the name of the game. Those with cash – you’ll be getting your opportunities in the next few months.