The year 2000 to 2002 was a fairly good barometer of what I think is to come with respect to these high-flying companies that populate the SaaS, ‘alternate energy’ and SPAC domains (I know SPACs are a financial characterization and do not necessarily reflect the entities that emerge from SPACs, but most of these are complete garbage reminiscent of the dot-com era of 1999-2000). There is also the market for crypto-garbage which many people in their 20’s are enamored with.

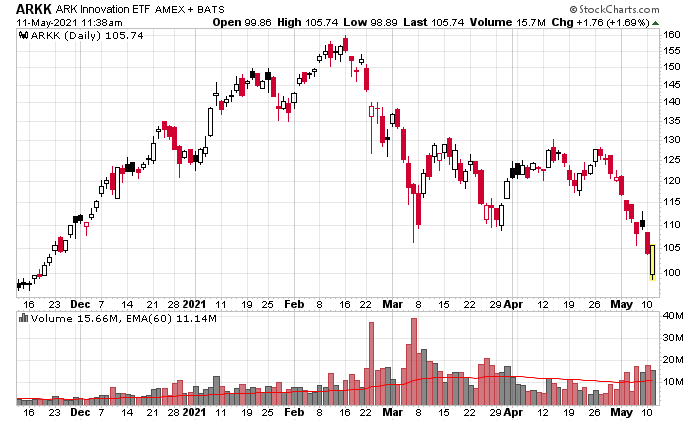

The poster child for all of the equity froth is the ARKK ETF:

There will be ups and downs, but the prevailing trend will be down as valuation eventually has to settle into the equation. Even after a major period of volatility in the spring of 2000, it took a couple years for the Nasdaq to fall roughly 75% from peak to trough before it began to recover again. Think about this – a 75% drop over 30 months.

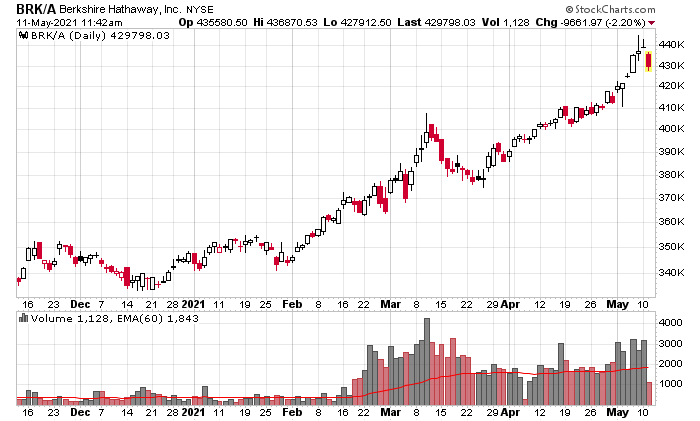

During this same time, companies that generated real cash flows and provided economically valuable goods and services did reasonably well. Berkshire was a great example of this. Warren Buffet prior to 2000 was criticized as being behind the times, just as he is today. Once again, he is going to get his revenge:

I think Warren wants to live to see the day when Berkshire Class A shares trade for US$1,000,000 a piece. He’s accelerating the process by buying back shares. Just imagine the headlines then.

In Canada, it’s actually not that bad in terms of the froth. When dredging up a list of winners over the past year, while there are a few obvious examples of “stinkers” which I will not mention here, there are many companies which are riding the resurgence of commodities and are well positioned to generate huge amounts of cash.

A good example of this is Teck, which exists in the sweet spots of being the leading metallurgical coal producer in Canada (also go look at a chart of Stelco for an idea of how the steel market is being treated currently), coupled with having a very large copper operation that will get even larger with the completion of the QB2 project in Chile – with current commodity pricing they will be minting billions in the upcoming years.

One might be fearful that a drop in the high-flying sectors of the stock market will translate into drops in valuations of “real economy” firms. While this might occur in the short term (as portfolios inevitably will de-leverage to some degree), past experience would suggest that sentiment will flow favorably to companies that can demonstrate profitability and valuations will receive a boost accordingly, especially since the alternate is much less attractive in our very low interest rate environment.

NASDAQ was lucky to bounce back yesterday, but after CPI report (showing exactly what all reasonable people were predicting – helicopter money will inevitably hit consumer prices at some point) its going to be rough summer for robinhoods.

Canadian real estate market will follow suit.

Improving legal access to online sports betting will provide a more natural home for the Robinhood crowd.

Is commodities & commodities producer the best place to hide should inflation takes hold? I speculate tech will get destroyed by PE multiple compression even if they make a boatload of money.

The textbook theory says only the ones actually producing or close to production – the ones that still have the metal or liquid in the ground will have their economic models destroyed by escalating costs.

Teck down 5% yesterday…any thoughts Sacha?

What’s the rhyme here? “As copper and coke flow, Teck will go”?

Thanks.