The month came and went, and despite all of the theater of Gamestop and the rest of the overall market, there weren’t any portfolio actions of note (some minor tweaking here and there, but it was some minor trimming and minor purchasing of existing positions, less than 1% of the portfolio).

In general, since the November “Biden jump”, many targets of opportunity out there have jumped up in price and presented themselves of being far less compelling than in 2020.

As a consequence of the two takeover offers that occurred in January (FLIR Systems (Nasdaq: FLIR) and Atlantic Power (TSX: ATP)), coupled with an imminent call of Gran Colombia Gold Notes (TSX: GCM.NT.U) and Bombardier’s inevitable debt repurchase offer, my effective cash position is in the teens at present. I’m still being paid to wait with these positions (merger arbitrage and collecting bond coupons is great, but oh-so-less exciting than watching Gamestop get volatility halted 8 times a day) so I’m in no rush to clear them out due to the lack of compelling alternatives.

There was one TSX stock that I performed an intensive research deep dive on, at a valuation that was compelling enough to put in an order to take a small starter position if the market allows for it. Price-wise, it did crash about 50% peak-to-trough during the Covid crunch (March 2020) but its recovery has been tepid, in a manner that I believe is relatively unwarranted. It is most definitely not a household name. It is also unlikely to triple overnight, but it should continue to retain value. Consider this a low risk, medium-reward type opportunity – a base hit single type investment.

Other than this, I’m happy to accumulate cash.

With vaccinations on the way, we will start to focus on the real economy again, the economy that has not been artificially inflated by fiscal spending in the name of COVID-19 mitigation. This is going to present itself as a very ugly picture.

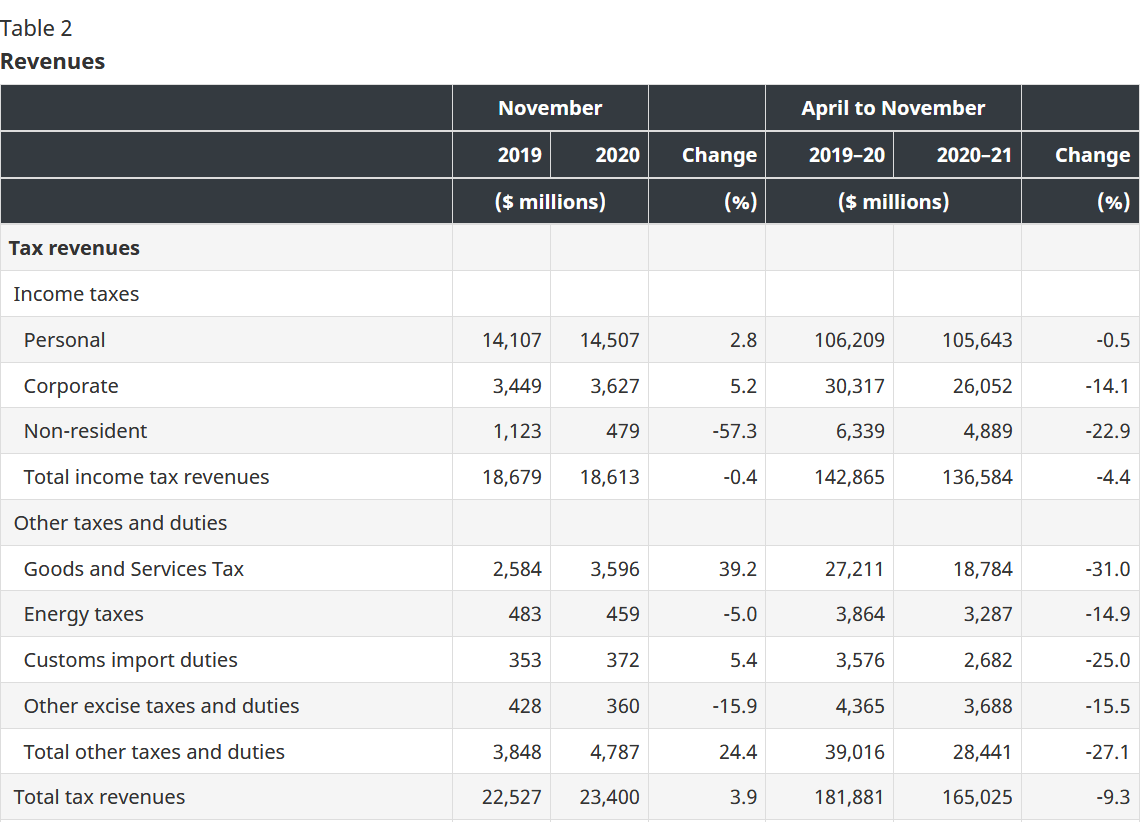

For instance, when we look at the November 2020 snapshot of Canada’s Fiscal Monitor, we see the following:

Note the GST collections: In April to November 2019 (8 months), the government collected $27.2 billion. In April to November 2020, the government collected $18.8 billion, a 31% decrease.

GST collections form the purest indication of end-consumer activity of GST-able products – i.e. non-food, non-export, non-residential rent consumption. This part of the real economy has exhibited a gigantic depression in activity. It is inescapable that this will take a very long time to recover to pre-COVID levels.

For historical context, during the same time periods, here were the GST collections for 2016 to 2020, April to November:

2020: $18.8 billion

2019: $27.2 billion

2018: $27.8 billion

2017: $25.8 billion

2016: $23.5 billion

What’s interesting is that the real economy was already going south before COVID-19 occurred.

Finally, in the belief that lightning can strike twice, the retail crowd that took Gamestop up to the roof is trying the same with the silver commodity. I couldn’t have picked a worse commodity to try to engage in market manipulation with. It all makes me wonder if this is part of some massively elaborate joke. That said, you might wish to be rounding up the cutlery in your grandmother’s kitchen – if silver heads up to $420 an ounce (funding secured), I’ll definitely be selling it.

On a bright side – decrease in GST means that Canadians are sitting on pile of cash ready to be spent, once there’s an opportunity. Of course, this will harm financial and real estate markets, but to me real life economics is always on the first place.