Dollarama (TSX: DOL), the dollar store that is all over the place in Canada, came up on my investment radar during a screen. I last looked it many years ago, and obviously I would have done very well had I just bought it, but even back then I recall thinking the stock was over-valued. Shows you how little I know!

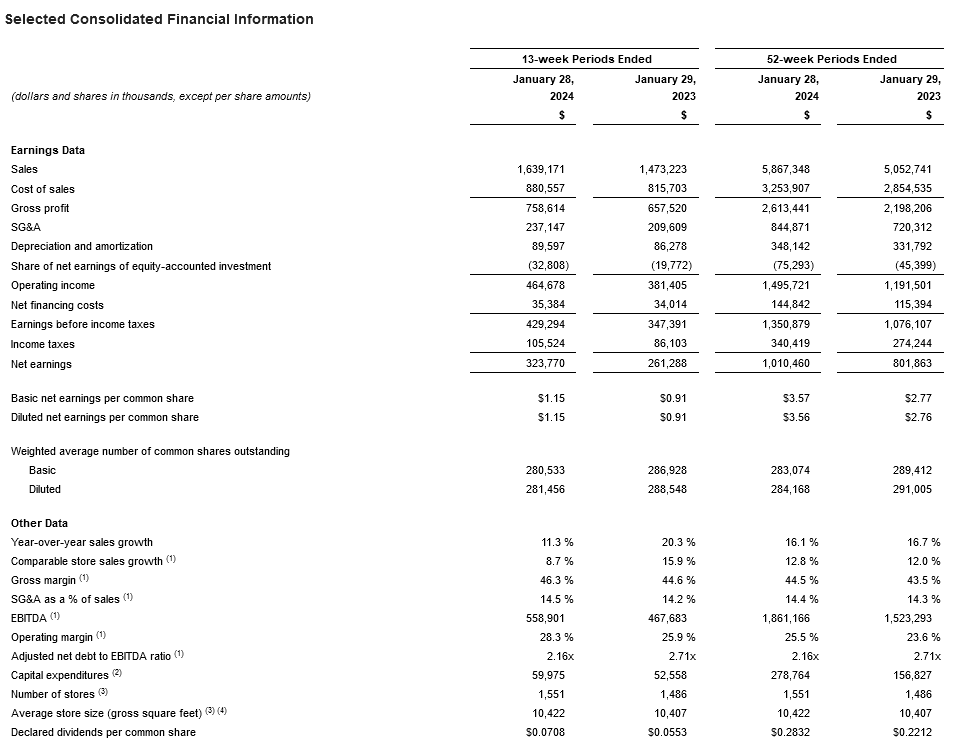

The following is a snapshot from their last fiscal annual result ending January 2024:

Some quick thoughts:

* Dollarama is one of the few retail segments that can effectively compete against Amazon, hence its ability to retain its margins is relatively good;

* They seem to out-compete other dollar store chains as well;

* Somehow they manage to successfully compete against the Loblaws (TSX: L) and Soebys (TSX: EMP.A) discount chains (No frills, Freshco, etc.);

* How many stores can they possibly run in Canada? 1,551 is the current number, what is the saturation point;

* Net operating margins (before taxes and interest expenses) of 25.5% – pretty damn good! Up from 23.6% in the previous year!

* Expansion out to South American in a 50.1% owned subsidiary of the company gives them more runway, but the dynamics of that market remain to be seen.

* Company is goosing up its stock price with buybacks – 7.12 million shares at $92/share

… the valuation currently is a share price of $118.32 over a $3.56/share, relatively “clean” net income, balance sheet not too levered (2x net income) with expansion expecting to increase the bottom line. DOL is trading at 33x trailing earnings, but ultimately the question here is – when do we get to the point where the entire world is flooded with these types of shops and margins come down or expansion simply stops? Dollar General (NYSE: DG) is the big fish in the USA (sales are about 10x that of Dollarama) and their operating margins are 6.3% and well down from 8.8% in the previous year! DG had quite a fall from grace, with their stock falling about 60% from their peak before they started to recover. While the market in Canada is a different (we tend to have less competition), it would not shock me if their stock had a similar change in fortune. The price being paid for shares is very high and assumes a significant amount of growth well into the future. Don’t get me started on the valuation of Costco, a retailer that I love with a stock I would never touch!